- European Central Bank

-

European Central Bank

European Central BankBulgarian: Европейска централна банка Czech: Evropská centrální banka Danish: Den Europæiske Centralbank Dutch: Europese Centrale Bank Estonian: Euroopa Keskpank Finnish: Euroopan keskuspankki French: Banque centrale européenne German: Europäische Zentralbank Greek: Ευρωπαϊκή Κεντρική Τράπεζα Hungarian: Európai Központi Βank Irish: Banc Ceannais Eorpach Italian: Banca Centrale Europea Latvian: Eiropas Centrālā banka Lithuanian: Europos centrinis bankas Maltese: Bank Ċentrali Ewropew Polish: Europejski Bank Centralny Portuguese: Banco Central Europeu Romanian: Banca Centrală Europeană Slovak: Európska centrálna banka Slovene: Evropska centralna banka Spanish: Banco Central Europeo Swedish: Europeiska centralbanken

Logo of the European Central Bank European Central Bank headquarters Headquarters Frankfurt am Main, Hesse, Germany Coordinates 50°06′34″N 8°40′26″E / 50.1095°N 8.6740°E Established 1 June 1998 President Mario Draghi Central bank of - Austria

- Belgium

- Cyprus

- Estonia

- France

- Finland

- Germany

- Greece

- Ireland

- Italy

- Luxembourg

- Malta

- Netherlands

- Portugal

- Slovakia

- Slovenia

- Spain

Currency Euro ISO 4217 Code EUR Reserves 526 billion euro in total- 43 billion euro directly

- 338 billion euro (Eurosystem incl. gold)

- 145 billion euro (forex reserves)

Base borrowing rate 1.25% Base deposit rate 0.50% Website www.ecb.int Preceded by 17 national banks- National Bank of Austria

- National Bank of Belgium

- Central Bank of Cyprus

- Bank of Estonia

- Bank of Finland

- Banque de France

- Deutsche Bundesbank

- Bank of Greece

- Central Bank of Ireland

- Banca d'Italia

- Central Bank of Luxembourg

- Central Bank of Malta

- De Nederlandsche Bank

- Banco de Portugal

- Bank of Slovenia

- National Bank of Slovakia

- Bank of Spain

The European Central Bank is the institution of the European Union (EU) that administers the monetary policy of the 17 EU Eurozone member states. It is thus one of the world's most important central banks. The bank was established by the Treaty of Amsterdam in 1998, and is headquartered in Frankfurt, Germany. The current President of the ECB is Mario Draghi, former governor of the Bank of Italy.

The primary objective of the European Central Bank is to maintain price stability within the Eurozone, which is the same as keeping inflation low. The Governing Council defined price stability as inflation of around 2%. (Harmonised Index of Consumer Prices) Unlike, for example, the United States Federal Reserve Bank, the ECB has only one primary objective with other objectives subordinate to it.

The key tasks of the ECB are to define and implement the monetary policy for the Eurozone, to conduct foreign exchange operations, to take care of the foreign reserves of the European System of Central Banks and promote smooth operation of the financial market infrastructure under the Target payments system and being currently developed technical platform for settlement of securities in Europe (TARGET2 Securities). Furthermore, it has the exclusive right to authorise the issuance of euro banknotes. Member states can issue euro coins but the amount must be authorised by the ECB beforehand (upon the introduction of the euro, the ECB also had exclusive right to issue coins).

On 9 May 2010, the 27 member states of the European Union agreed to incorporate the European Financial Stability Facility. The EFSF’s mandate is to safeguard financial stability in Europe by providing financial assistance to Eurozone Member States.

The bank must also co-operate within the EU and internationally with third bodies and entities. Finally it contributes to maintaining a stable financial system and monitoring the banking sector. The latter can be seen, for example, in the bank's intervention during the 2007 credit crisis when it loaned billions of euros to banks to stabilise the financial system.

Although the ECB is governed by European law directly and thus not by corporate law applying to private law companies, its set-up resembles that of a corporation in the sense that the ECB has shareholders and stock capital. Its capital is five billion euro which is held by the national central banks of the member states as shareholders. The initial capital allocation key was determined in 1998 on the basis of the states' population and GDP, but the key is adjustable. Shares in the ECB are not transferable and cannot be used as collateral.

Throughout 2011 various member states of the European Union showed themselves to be increasingly unable to meet financial commitments. At its heart, the crisis of the European currency unit or ECU is similar to almost any other financial crisis, including the crisis of 2008. Key concepts to understanding the crisis include collateral, assets, and liabilities.

The bank is based in Frankfurt, the largest financial centre in the Eurozone (although not the largest in the European Union). Its location in the city is fixed by the Amsterdam Treaty along with other major institutions. In the city, the bank currently occupies Frankfurt's Eurotower until its purpose-built headquarters are built.

The owners and shareholders of the European Central Bank are the 27 member states of the EU.

Contents

History

Further information: History of the euroThe European Central Bank is the de facto successor of the European Monetary Institute (EMI).[1] The EMI was established at the start of the second stage of the EU's Economic and Monetary Union (EMU) to handle the transitional issues of states adopting the euro and prepare for the creation of the ECB and European System of Central Banks (ESCB).[1] The EMI itself took over from the earlier European Monetary Co-operation Fund (EMCF).[2]

The ECB formally replaced the EMI on 1 June 1998 by virtue of the Treaty on European Union (TEU, Treaty of Maastricht), however it did not exercise its full powers until the introduction of the euro on 1 January 1999, signalling the third stage of EMU.[1] The bank was the final institution needed for EMU, as outlined by the EMU reports of Pierre Werner and President Jacques Delors. It was established on 1 June 1998.[3]

The first President of the Bank was Wim Duisenberg, the former president of the Dutch central bank and the European Monetary Institute.[3] While Duisenberg had been the head of the EMI (taking over from Alexandre Lamfalussy of Belgium) just before the ECB came into existence,[3] the French government wanted Jean-Claude Trichet, former head of the French central bank, to be the ECB's first president.[3] The French argued that since the ECB was to be located in Germany, its President should be French. This was opposed by the German, Dutch and Belgian governments who saw Duisenberg as a guarantor of a strong euro.[4] Tensions were abated by a gentleman's agreement in which Duisenberg would stand down before the end of his mandate, to be replaced by Trichet, which occurred in November 2003.[5]

There had also been tension over the ECB's Executive Board, with the United Kingdom demanding a seat even though it had not joined the Single Currency.[4] Under pressure from France, three seats were assigned to the largest members, France, Germany, and Italy; Spain also demanded and obtained a seat. Despite such a system of appointment the board asserted its independence early on in resisting calls for interest rates and future candidates to it.[4]

When the ECB was created, it covered a Eurozone of eleven members. Since then, Greece joined in January 2001, Slovenia in January 2007, Cyprus and Malta in January 2008, Slovakia in January 2009, and Estonia in January 2011, enlarging the bank's scope and the membership of its Governing Council.[2]

On 1 December 2009, the Treaty of Lisbon entered into force, ECB according to the article 13 of TEU, gained official status of an EU institution.

In April 2011, the ECB raised interest rates for the first time since 2008 from 1% to 1.25%,[6] with a further increase to 1.50% in July 2011.[7]

Future

When German appointee to the Governing Council and Executive board, Jürgen Stark, resigned in protest of the ECB's bond buying programme, Financial Times Deutschland called it "the end of the ECB as we know it" referring to its perceived "hawkish" stance on inflation and its historical Bundesbank influence.[8]

Powers and objectives

The primary objective of the European Central Bank is to maintain price stability within the Eurozone, which is the same as keeping inflation low. The Governing Council defined price stability as inflation of around 2%. (Harmonised Index of Consumer Prices) [9] Unlike for example the United States Federal Reserve Bank, the ECB has only one primary objective with other objectives subordinate to it.

Authorities

The key tasks of the ECB are to define and implement the monetary policy for the Eurozone, to conduct foreign exchange operations, to take care of the foreign reserves of the European System of Central Banks and promote smooth operation of the financial market infrastructure under the Target payments system[10] and being currently developed technical platform for settlement of securities in Europe (TARGET2 Securities). Furthermore, it has the exclusive right to authorise the issuance of euro banknotes. Member states can issue euro coins but the amount must be authorised by the ECB beforehand (upon the introduction of the euro, the ECB also had exclusive right to issue coins).[10]

In U.S. style central banking, liquidity is furnished to the economy primarily through the purchase of Treasury bonds by the Federal Reserve Bank. The Eurosystem uses a different method. There are about 1500 eligible banks which may bid for short term repo contracts of two weeks to three months duration.[11] The banks in effect borrow cash and must pay it back; the short durations allow interest rates to be adjusted continually. When the repo notes come due the participating banks bid again. An increase in the quantity of notes offered at auction allows an increase in liquidity in the economy. A decrease has the contrary effect. The contracts are carried on the asset side of the European Central Bank's balance sheet and the resulting deposits in member banks are carried as a liability. In lay terms, the liability of the central bank is money, and an increase in deposits in member banks, carried as a liability by the central bank, means that more money has been put into the economy.[12]

Mandates

To qualify for participation in the auctions, banks must be able to offer proof of appropriate collateral in the form of loans to other entities. These can be the public debt of member states, but a fairly wide range of private banking securities are also accepted.[13] The fairly stringent membership requirements for the European Union, especially with regard to sovereign debt as a percentage of each member state's gross domestic product, are designed to insure that assets offered to the bank as collateral are, at least in theory, all equally good, and all equally protected from the risk of inflation.[13] The economic and financial crisis that began in 2008 has revealed some relative weaknesses in the sovereign debt of such member countries as Portugal, Ireland, Greece and Spain.[14] These securities are not limited to the countries of issue, but held in many cases by banks in other member states.[13] To the extent that the banks authorized to borrow from the ECB have compromised collateral, their ability to borrow from the ECB—and thus the liquidity of the economic system—is impaired.[13] This threat has drawn the ECB into rescue operations.[13] But weak sovereign debt is not the only source of weakness in the ECB's operations, as the collapse of the market in U.S. dollar denominated collateralized debt obligations has also led to large scale interventions in cooperation with the Federal Reserve.[13]

Rescue operations involving sovereign debt have included temporarily moving bad or weak assets off the balance sheets of the weak member banks into the balance sheets of the European Central Bank.[15] Such action is viewed as monetization and can be seen as an inflationary threat, whereby the strong member countries of the ECB shoulder the burden of monetary expansion (and potential inflation) in order to save the weak member countries.[15] Most central banks prefer to move weak assets off their balance sheets with some kind of agreement as to how the debt will continue to be serviced.[15] This preference has typically led the ECB to argue that the weaker member countries must:

- Allocate considerable national income to servicing debts.[15]

- scale back a wide range of national expenditures (such as education, infrastructure, and welfare transfer payments) in order to make their payments.[15]

European Financial Stability Facility

On 9 May 2010, the 27 member states of the European Union agreed to incorporate the European Financial Stability Facility.[16] The EFSF’s mandate is to safeguard financial stability in Europe by providing financial assistance to Eurozone Member States.[16]

The European Financial Stability Facility is authorised to use the following instruments linked to appropriate conditionality:

- To provide loans to countries in financial difficulties, like in the event of Greece.[16]

- To intervene in the primary and secondary debt markets. Intervention in the secondary debt market will be only on the basis of an ECB analysis recognising the existence of exceptional financial market circumstances and risks to financial stability.[16]

- Act on the basis of a precautionary programme.[16]

- Finance recapitalisations of financial institutions through loans to governments[16]

The EFSF is backed by guarantee commitments from the Eurozone Member States for a total of €780 billion and has a lending capacity of €440 billion.[16] It has been assigned the best possible credit rating (AAA by Standard & Poor’s and Fitch Ratings, Aaa by Moody’s)[16]

Powers and objectives during the European banking crisis

The European Central Bank had stepped up the buying of member nations debt.[17] In response to the crisis of 2010, some proposals have surfaced for a collective European bond issue that would allow the central bank to purchase a European version of U.S. Treasury Bills.[18][19] To make European sovereign debt assets more similar to a U.S. Treasury, a collective guarantee of the member states' solvency would be necessary.[20] But the German government has resisted this proposal, and other analyses indicate that "the sickness of the Euro" is due to the linkage between sovereign debt and failing national banking systems. If the European central bank were to deal directly with failing banking systems sovereign debt would not look as leveraged relative to national income in the financially weaker member states.[19]

On 17 December 2010, the ECB announced that it was going to double its capitalization.[21] (The ECB's most recent balance sheet before the announcement listed capital and reserves at €2.03 trillion.)[22] The sixteen central banks of the member states would transfer assets to the ledger of the ECB. In banking, assets (loans) are used to offset liabilities (deposits and currency).[22] If some of the sovereign debt held as an asset by the ECB becomes non-performing, the asset is "bad" and the deposits, in this case, currency, are not appropriately backed.[22] This inequality means that liabilities exceed assets and therefore the bank is in trouble.[22] One response is to use the bank's capital to offset the losses.[22] The use of capital to offset a loss transfers the loss to the bank's shareholders: the member banks.[22] The increased capitalization of the ECB against potential sovereign debt default means that the sixteen member banks are also exposed to potential losses.[22] In 2011, the European member states may need to raise as much as US$2 trillion in debt.[21] Some of this will be new debt and some will be previous debt that is "rolled over" as older loans reach maturity. In either case, the ability to raise this money depends on the confidence of investors in the European financial system.[22] The ability of the European Union to guarantee its members' sovereign debt obligations have direct implications for the core assets of the banking system that support the Euro.[21]

The bank must also co-operate within the EU and internationally with third bodies and entities. Finally it contributes to maintaining a stable financial system and monitoring the banking sector.[23] The latter can be seen, for example, in the bank's intervention during the 2007 credit crisis when it loaned billions of euros to banks to stabilise the financial system.[24] In December 2007, the ECB decided in conjunction with the Federal Reserve under a program called Term auction facility to improve dollar liquidity in the eurozone and to stabilise the money market.[25]

Independence

Furthermore, not only must the bank not seek influence, but EU institutions and national governments are bound by the treaties to respect the ECB's independence. For example, the minimum term of office for a national central bank governor is five years and members of the executive board have a non-renewable eight-year term.[26] To offer some accountability, the ECB is bound to publish reports on its activities and has to address its annual report to the European Parliament, the European Commission, the Council of the European Union and the European Council.[27] The European Parliament also gets to question and then issue its opinion on candidates to the executive board.[28]

The bank's independence has notably come under intense criticism since the election of Nicolas Sarkozy as French President. Sarkozy has sought to make the ECB more susceptible to political influence, to extend its mandate to focus on growth and job creation (at cost of inflation), and has frequently criticized the bank's policies on interest rates.[29] As result of pressure from France and Greece, independence of ECB has been limited.[29] The same has happened with Stability and Growth Pact that sets fiscal limits in the euro zone — these limits have been notoriously violated but no member country has been fined.[29]

Organization

Although the ECB is governed by European law directly and thus not by corporate law applying to private law companies, its set-up resembles that of a corporation in the sense that the ECB has shareholders and stock capital. Its capital is five billion euros[30] which is held by the national central banks of the member states as shareholders. The initial capital allocation key was determined in 1998 on the basis of the states' population and GDP,[31] but the key is adjustable.[32] Shares in the ECB are not transferable and cannot be used as collateral.[33]

All National Central Banks (NCBs) that own a share of the ECB capital stock as of 1 January 2011 are listed below. Non-Euro area NCBs are required to pay up only a very small percentage of their subscribed capital, which accounts for the different magnitudes of Euro area and Non-Euro area total paid-up capital.[34]

NCB Capital Key (%) Paid-up Capital (€) Nationale Bank van België / Banque Nationale de Belgique 2.4256 180,157,051.35 Deutsche Bundesbank 18.9373 1,406,533,694.10 Eesti Pank 0.1790 13,294,901.14 Central Bank of Ireland 1.1107 82,495,232.91 Τράπεζα της Ελλάδος (Bank of Greece) 1.9649 145,939,392.39 Banco de España 8.3040 616,764,575.51 Banque de France 14.2212 1,056,253,899.48 Banca d'Italia 12.4966 928,162,354.81 Kεντρική Τράπεζα Κύπρου / Kıbrıs Merkez Bankası

(Central Bank of Cyprus)0.1369 10,167,999.81 Banque centrale du Luxembourg 0.1747 12,975,526.42 Bank Ċentrali ta' Malta 0.0632 4,694,065.65 De Nederlandsche Bank 3.9882 296,216,339.12 Österreichische Nationalbank 1.9417 144,216,254.37 Banco de Portugal 1.7504 130,007,792.98 Banka Slovenije 0.3288 24,421,025.10 Národná banka Slovenska 0.6934 51,501,030.43 Suomen Pankki - Finlands Bank 1.2539 93,131,153.81 Total 69.9705 5,196,932,289.36 Non-Euro area: Българска народна банка (Bulgarian National Bank) 0.8686 3,505,013.50 Česká národní banka 1.4472 5,839,806.06 Danmarks Nationalbank 1.4835 5,986,285.44 Latvijas Banka 0.2837 1,144,798.91 Lietuvos bankas 0.4256 1,717,400.12 Magyar Nemzeti Bank 1.3856 5,591,234.99 Narodowy Bank Polski 4.8954 19,754,136.66 Banca Naţională a României 2.4645 9,944,860.44 Sveriges Riksbank 2.2582 9,112,389.47 Bank of England 14.5172 58,580,453.65 Total 30.0295 121,176,379.25 European Union

This article is part of the series:

Politics and government of

the European UnionPolicies and issuesThe Executive Board is responsible for the implementation of monetary policy defined by the Governing Council and the day-to-day running of the bank.[35] In this it can issue decisions to national central banks and may also exercise powers delegated to it by the Governing Council.[35] It is composed of the President of the Bank (currently Mario Draghi), a vice president (currently Vitor Constâncio) and four other members.[35] They are all appointed by common accord of the Eurozone member states for non-renewable terms of eight years.[35]

The General Council is a body dealing with transitional issues of euro adoption, for example fixing the exchange rates of currencies being replaced by the euro (continuing the tasks of the former EMI).[35] It will continue to exist until all EU member states adopt the euro, at which point it will be dissolved.[35] It is composed of the President and Vice President together with the governors of all of the EU's national central banks.[36][37]

European sovereign debt crisis

Main article: European sovereign debt crisisFrom late 2009, fears of a sovereign debt crisis developed among fiscally conservative investors concerning some European states, with the situation becoming particularly tense in early 2010.[38][39] This included euro zone members Greece,[40] Ireland and Portugal and also some EU countries outside the area.[41] Iceland, the country which experienced the largest crisis in 2008 when its entire international banking system collapsed has emerged less affected by the sovereign debt crisis as the government was unable to bail the banks out. In the EU, especially in countries where sovereign debts have increased sharply due to bank bailouts, a crisis of confidence has emerged with the widening of bond yield spreads and risk insurance on credit default swaps between these countries and other EU members, most importantly Germany.[42][43] To be included in the eurozone, the countries had to fulfill certain convergence criteria, but the meaningfulness of such criteria were diminished by the fact they have not been applied to different countries with the same strictness.[44]

Causes

The principal monetary policy tool of the European central bank is collateralized borrowing or repo agreements.[45] These tools are also used by the United States Federal Reserve Bank, but the Fed does more direct purchasing of financial assets than its European counterpart.[46] The collateral used by the ECB is typically high quality public and private sector debt.[45] The criteria for determining "high quality" for public debt have been preconditions for membership in the European Union: total debt must not be too large in relation to Gross Domestic Product, for example, and deficits in any given year must not become too large.[47] Though these criteria are fairly simple, a number of accounting techniques may hide the underlying reality of fiscal solvency—or the lack of same.[47]

In central banking, the privileged status of the central bank is that it can make as much money as it deems needed.[48] In the United States Federal Reserve Bank, the Federal Reserve buys assets: typically, bonds issued by the Federal government.[48] There is no limit on the bonds that it can buy and and one of the tools at its disposal in a financial crisis is take such extraordinary measures as the purchase of large amounts of assets such as commercial paper.[48] The purpose of such operations is to ensure that adequate liquidity is available for functioning of the financial system.[48]

Response to the crisis

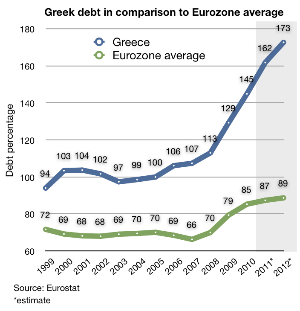

The first round of austerity in 2010 failed to stop Greece's rising debt, which is expected to go up by 10% in 2011.[49]

The first round of austerity in 2010 failed to stop Greece's rising debt, which is expected to go up by 10% in 2011.[49]

There are a variety of possible responses to the problem of bad debts in a banking system. One is to induce debtors to make a greater effort to make good on their debt.[45] With public debt this usually means getting governments to maintain debt payments while cutting back on other forms of expenditure.[45] Such policies often involve cutting back on popular social programs.[50] Stringent policies with regard to social expenditures and employment in the state sector have led to riots and political protests in Greece.[51] Another response is to shift losses from the central bank to private investors who are asked to "share the pain" of partial defaults that take the form of rescheduling debt payments.[45] However, if the debt rescheduling causes losses on loans held by European banks, it weakens the private banking system, which then puts pressure on the central bank to come to the aid of those banks. Private sector bond holders are an integral part of the public and private banking system. Another possible response is for wealthy member countries to guarantee or purchase the debt of countries that have defaulted or are likely to default.[45] This alternative requires that the tax revenues and credit of the wealthy member countries be used to refinance the previous borrowing of the weaker member countries, and is politically controversial.[52] Reluctance in Germany to take on the burden of financing or guaranteeing the debts of weaker countries has led to public reports that some elites in Germany would prefer to see Greece, Portugal, and even Italy leave the Euro zone "temporarily."[53] However, Greek Euro zone exit was rejected by German Chancellor Angela Merkel.[54]

Bond purchase

The ECB could, and through the late summer of 2011 did, purchase bonds issued by the weaker states even though it assumes, in doing so, the risk of a deteriorating balance sheet. ECB buying focused primarily on Spanish and Italian debt.[55] Certain techniques can minimize the impact. Purchases of Italian bonds by the central bank, for example, were intended to dampen international speculation and strengthen portfolios in the private sector and also the central bank.[56] The assumption is that speculative activity will decrease over time and the value of the assets increase. Such a move is similar to what the U.S. federal reserve did in buying subprime mortgages in the crisis of 2008, except in the European crisis, the purchases are of member state debt. The risk of such a move is that it could diminish the value of the currency.[47] On the other hand, certain financial techniques can reduce the impact of such purchases on the currency.[47] One is sterilization, wherein highly valued assets are sold at the same time that the weaker assets are purchased, which keeps the money supply neutral.[47] Another technique is simply to accept the bad assets as long-term collateral (as opposed to short-term repo swaps) to be held until their market value stabilizes. This would imply, as a quid pro quo, adjustments in taxation and expenditure in the economies of the weaker states to improve the perceived value of the assets.[47]

Location

Main article: European Central Bank Headquarters Model of the ECB's new headquarters, which is due to be completed in 2014.

Model of the ECB's new headquarters, which is due to be completed in 2014.The bank is based in Frankfurt, the largest financial centre in the Eurozone. Its location in the city is fixed by the Amsterdam Treaty along with other major institutions.[57] In the city, the bank currently occupies Frankfurt's Eurotower until its purpose-built headquarters are built.[58]

In 1999 an international architectural competition was launched by the bank to design a new building.[59] It was won by a Vienna-based architectural office named Coop Himmelbau.[59] The building will be approximately 180 metres (591 ft) tall (the present building is 148 m/486 ft high.) and will be accompanied with other secondary buildings on a landscaped site on the site of the former wholesale market in the eastern part of Frankfurt am Main. The main construction began in October 2008, with completion scheduled during 2014.[59][60] It is expected that the building will become an architectural symbol for Europe and is designed to cope with double the number of staff who operate in the Eurotower.[61]

See also

- European Banking Authority

- European Systemic Risk Board

- Open market operations

References

- ^ a b c "ECB: Economic and Monetary Union". ECB. http://www.ecb.int/ecb/history/emu/html/index.en.html. Retrieved 15 October 2007.

- ^ a b "European Central Bank". European NAvigator. http://www.ena.lu?lang=2&doc=8034. Retrieved 15 October 2007.

- ^ a b c d "ECB: Economic and Monetary Union". Ecb.int. http://www.ecb.int/ecb/history/emu/html/index.en.html. Retrieved 2011-06-26.

- ^ a b c "The third stage of Economic and Monetary Union". European NAvigator. http://www.ena.lu?lang=2&doc=14950. Retrieved 16 October 2007.

- ^ "The powerful European Central Bank [ E C B in the heart of Frankfurt/Main - Germany - The Europower in Mainhattan - Enjoy the glances of euro and europe....03/2010....travel round the world....:)"]. UggBoy♥UggGirl [ PHOTO // WORLD // TRAVEL ]. Flickr. 6 March 2010. http://www.flickr.com/photos/uggboy/4417740330/. Retrieved 14 October 2011.

- ^ "ECB Raises Interest Rates - MarketWatch". marketwatch.com. 2011 [last update]. http://www.marketwatch.com/story/ecb-raises-interest-rates-2011-04-07. Retrieved 14 July 2011.

- ^ "ECB: Key interest rates". 2011 [last update]. http://www.ecb.int/stats/monetary/rates/html/index.en.html. Retrieved 29 August 2011.

- ^ Financial Times Deutschland

- ^ "Powers and responsibilities of the European Central Bank". European Central Bank. http://www.ecb.int/ecb/orga/tasks/html/index.en.html. Retrieved 10 March 2009.

- ^ a b Fairlamb, David; Rossant, John (12 February 2003). "The powers of the European Central Bank". BBC News. http://news.bbc.co.uk/1/hi/business/business_basics/86006.stm. Retrieved 16 October 2007.

- ^ In practice, 400-500 banks participate regularly.

Samuel Cheun; Isabel von Köppen-Mertes and Benedict Weller (December 2009), The collateral frameworks of the Eurosystem, the Federal Reserve System and the Bank of England and the financial market turmoil, ECB, http://www.ecb.int/pub/pdf/scpops/ecbocp107.pdf, retrieved 2011-08-24 - ^ The process is similar, though on a grand scale, to an individual who every month charges $10,000 on his or her credit card, pays it off every month, but also withdraws (and pays off) an additional $10,000 each succeeding month for transaction purposes. Such a person is operating "net borrowed" on a continual basis, and even though the borrowing from the credit card is short term, the effect is a stable increase in the money supply. If the person borrows less, less money circulates in the economy. If he or she borrows more, the money supply increases. An individual's ability to borrow from his or her credit card company is determined by the credit card company: it reflects the company's overall judgment of its ability to lend to all borrowers, and also its appraisal of the financial condition of that one particular borrower. The ability of member banks to borrow from the central bank is fundamentally similar.

- ^ a b c d e f Bertaut, Carol C. (2002). "The European Central Bank and the Eurosystem". New England Economic Review (2nd Quarter): 25–28. http://www.bos.frb.org/economic/neer/neer2002/neer202e.pdf.

- ^ Minder, Raphel (24 November 2010). "Fears Mount Over Spain and Risks to the Euro". New York Times. http://www.nytimes.com/2010/11/25/business/global/25spainecon.html. Retrieved 24 November 2010.

- ^ a b c d e Buite, Willem (07-09-2010). "Greece and the fiscal crisis in the EMU". NBER. http://www.nber.org/~wbuiter/Greece.pdf. Retrieved October 30, 2011.

- ^ a b c d e f g h "About EFSF". EFSF. efsf.europa.eu. 9 May 2010. http://www.efsf.europa.eu/about/index.htm. Retrieved 19 October 2011.

- ^ "Euro zone bonds rally after ECB debt buying". Irish Times. December 2, 2010. http://www.irishtimes.com/newspaper/finance/2010/1202/1224284573209.html.

- ^ Walker, Marcus (17 December 2010). "Closer Fiscal Union: A Collective Guarantee". Wall Street Journal. http://online.wsj.com/article/SB10001424052748703395204576023784088914652.html.

- ^ a b Nixon, Simon (7 December 2010). "A Way Around European Bonds". Wall Street Journal. http://online.wsj.com/article/SB10001424052748704156304576003760628199904.html.

- ^ The European dilemma may be imagined as follows. In the United States, if tax collections from California are weak, the total federal debt is financed through tax collections in other states, through federal taxes. California may default on its state debt, but the federal government bypasses California in directly taxing California citizens to finance the federal debt. There is only one legal authority taxing, paying for, and backing the federal debt. Federal expenditures are determined by the federal government. Therefore California cannot leverage more money out of the federal system other than by means of the normal constitutional procedures in the House and Senate. If the federal government transfers additional money to California it is because of federal policy, not because California's state debt is threatening the backing of the U.S. dollar. Consider this hypothetical: If the U.S. federal reserve carried state debts on its balance sheets the system would be more similar to the ECB. If California stated to default on its debt a hole would appear on the Fed's balance sheets where it carried California bonds. To make good this loss, the Fed would have to raise capital from the more solvent states, giving rise to the political issue that California's "lack of responsibility" was forcing other states to jump in and save California's public debt. This, one might worry, could turn into a license to California to ignore fiscal restraints and in effect transfer money from the "more responsible states" to the "least responsible states." Even though California's state finances are faltering in 2010, this is not an issue for the Federal Reserve, because of the federal system of taxation and unified backing of the federal debt. In Europe, the ECB could push for greater political and fiscal integration, which would make the member states more explicitly responsible for backing each others debts and potentially lead to greater political integration. Speculative attacks on the sovereign debt that backs the euro have in effect revealed the weaknesses in the European Union's political and fiscal structure.

- ^ a b c Walker, Marcus; Forelle, Charles (17 December 2010). "Bailout Deal Fails to Quell EU rifts". Wall Street Journal. http://online.wsj.com/article/SB10001424052748703395204576023732485094802.html.

- ^ a b c d e f g h "Aggregated balance sheet of euro area monetary financial institutions, excluding the Eurosystem". ECB.int. http://www.ecb.int/stats/money/aggregates/bsheets/html/outstanding_amounts_L60.X.Z5.0000.en.html.

- ^ "The European Central Bank (ECB)". Europa (web portal). http://europa.eu/scadplus/leg/en/lvb/o10001.htm. Retrieved 16 October 2007.

- ^ Lander, Mark (14 August 2007). "Credit Squeeze Puts Europe's Bank in Spotlight". New York Times. http://www.nytimes.com/2007/08/14/business/worldbusiness/14euro.html?_r=1&n=Top/Reference/Times%20Topics/Organizations/E/European%20Central%20Bank&oref=slogin. Retrieved 16 October 2007.

- ^ "ECB press release on dollar liquidity". ECB. http://www.ecb.int/press/pr/date/2008/html/pr080110_2.en.html.

- ^ "Independence". European Central Bank. http://www.ecb.int/ecb/orga/independence/html/index.en.html. Retrieved 15 October 2007.

- ^ "Accountability". European Central Bank. http://www.ecb.int/ecb/orga/accountability/html/index.en.html. Retrieved 15 October 2007.

- ^ "Executive Board" (PDF). Banque de France. 2005. http://www.banque-france.fr/gb/eurosys/telechar/europe/Directoire_GB.pdf. Retrieved 15 October 2007.

- ^ a b c Philipp Bagus (2010) (PDF). Tragedy of the Euro. ISBN 9781610161183. http://mises.org/books/bagus_tragedy_of_euro.pdf. Retrieved 2011-10-28.

- ^ Article 28.1 of the ESCB Statute

- ^ Article 29 of the ESCB Statute

- ^ Article 28.5 of the ESCB Statute

- ^ Article 28.4 of the ESCB Statute

- ^ "Capital Subscription". European Central Bank. http://www.ecb.int/ecb/orga/capital/html/index.en.html. Retrieved 11 June 2011.

- ^ a b c d e f "ECB: Governing Council". ECB. ecb.int. 1 January 2002. http://www.ecb.int/ecb/orga/decisions/govc/html/index.en.html. Retrieved 28 October 2011.

- ^ "Composition of the European Central Bank". European Navigator. http://www.ena.lu?lang=2&doc=8035. Retrieved 15 October 2007.

- ^ "The General Council". ecb.europa.int. http://www.ecb.europa.int/ecb/orga/decisions/genc/html/index.en.html. Retrieved 15 October 2007.

- ^ George Matlock (16 February 2010). "Peripheral euro zone government bond spreads widen". Reuters. http://www.reuters.com/article/idUSLDE61F0W720100216. Retrieved 28 April 2010.

- ^ "Acropolis now". The Economist. 29 April 2010. http://www.economist.com/node/16009099. Retrieved 22 June 2011.

- ^ Brian Blackstone, Tom Lauricella, and Neil Shah (5 February 2010). "Global Markets Shudder: Doubts About U.S. Economy and a Debt Crunch in Europe Jolt Hopes for a Recovery". The Wall Street Journal. http://online.wsj.com/article/SB10001424052748704041504575045743430262982.html. Retrieved 10 May 2010.

- ^ Bruce Walker (9 April 2010). "Greek Debt Crisis Worsens". The New American. http://www.thenewamerican.com/index.php/world-mainmenu-26/europe-mainmenu-35/3274-greek-debt-crisis-worsens. Retrieved 28 April 2010.

- ^ "Greek/German bond yield spread more than 1,000 bps". Financialmirror.com. 28 April 2010. http://www.financialmirror.com/News/Cyprus_and_World_News/20151. Retrieved 5 May 2010.[dead link]

- ^ "Gilt yields rise amid UK debt concerns". Financial Times. 18 February 2010. http://www.ft.com/cms/s/0/7d25573c-1ccc-11df-8d8e-00144feab49a.html. Retrieved 15 April 2011.

- ^ "The politics of the Maastricht convergence criteria | vox - Research-based policy analysis and commentary from leading economists". Voxeu.org. 2009-04-15. http://www.voxeu.org/index.php?q=node/3454. Retrieved 2011-10-01.

- ^ a b c d e f "All about the European debt crisis: In SIMPLE terms". rediff business. rediff.com. 19 August 2011. http://www.rediff.com/business/slide-show/slide-show-1-all-about-european-debt-crisis-in-simple-terms/20110819.htm. Retrieved 28 October 2011.

- ^ "Open Market Operation - Fedpoints - Federal Reserve Bank of New York". Federal Reserve Bank of New York. www.newyorkfed.org. August 2011. http://www.newyorkfed.org/aboutthefed/fedpoint/fed32.html. Retrieved 29 October 2011.

- ^ a b c d e f "WORKING PAPER 2011 / 1 A COMPREHENSIVE APPROACH TO THE EURO-AREA DEBT CRISIS" (PDF). Zsolt Darvas. Corvinus University of Budapest. February 2011. http://unipub.lib.uni-corvinus.hu/304/1/wp_2011_1_darvas.pdf. Retrieved 28 October 2011.

- ^ a b c d Ben S. Bernanke (December 1, 2008). "Federal Reserve Policies in the Financial Crisis" (Speech). Greater Austin Chamber of Commerce, Austin, Texas: Board of Governors of the Federal Reserve System. http://www.federalreserve.gov/newsevents/speech/bernanke20081201a.htm. Retrieved October 23, 2011. "To ensure that adequate liquidity is available, consistent with the central bank's traditional role as the liquidity provider of last resort, the Federal Reserve has taken a number of extraordinary steps."

- ^ "Προβλέψεις της Ευρ. Επιτροπής". To Vima. http://www.tovima.gr/finance/article/?aid=400463. Retrieved 3 July 2011.

- ^ Cohen, Sabrina (14 August 2011). "Italian Unions Criticize Austerity Plan". Wall Street Journal. http://online.wsj.com/article/SB10001424053111903392904576508253558418390.html.

- ^ CNN Wire Staff (28 June 2011). "Greek austerity protests turn ugly as strike begins". http://articles.cnn.com/2011-06-28/world/greece.strike_1_police-and-protesters-stone-throwing-demonstrators-force-protesters?_s=PM:WORLD.

- ^ Castle, Stephen (15 July 2011). "Euro Zone Seeks Deal on Greece". New York Times. http://www.nytimes.com/2011/07/16/business/global/eu-leaders-to-meet-thursday-to-try-to-break-deadlock-on-greece.html.

- ^ Ewing, Jack; Alderman, Liz (10 August 2011). "Some in Germany Want Greece to Temporarily Exit the Euro Zone". New York Times. http://www.nytimes.com/2011/08/11/business/global/greece-feels-push-toward-euro-exit.html.

- ^ Walker, Marcus; Bisserbe, Noemie (14 September 2011). "Merkel Lessens Fears Over Greece: German Leader Rejects Suggestions Athens Be Allowed to Default or Leave Currency Bloc, Reassuring Nervous Markets". Wall Street Journal. http://online.wsj.com/article/SB10001424053111904265504576568693911614726.html?mod=WSJ_hp_LEFTWhatsNewsCollection.

- ^ McManus, John; O'Brien, Dan (5 August 2011). "Market rout as Berlin rejects call for more EU action". Irish Times.

- ^ Walker, Marcus; Paletta, Damian; Blacksone, Brian (13 August 2011). "Global Crisis of Confidence World Policy Makers' Inability to Agree on Fixes Led Markets on Wild Ride". Wall Street Journal.

- ^ "Consolidated versions of the treaty on European Union and of the treaty establishing the European Community" (PDF). Eur-lex. http://eur-lex.europa.eu/LexUriServ/site/en/oj/2006/ce321/ce32120061229en00010331.pdf. Retrieved 12 June 2007.

- ^ Dougherty, Carter. "In ECB future, a new home to reflect all of Europe". International Herald Tribune. http://www.iht.com/articles/2004/11/16/ecb_ed3_.php. Retrieved 2 August 2007.

- ^ a b c "Winning design by Coop Himmelb(l)au for the ECB's new headquarters in Frankfurt/Main". European Central Bank. Archived from the original on 2007-09-24. http://web.archive.org/web/20070924213221/http://www.ecb.int/ecb/premises/html/image29.en.html. Retrieved 2 August 2007.

- ^ "Launch of a public tender for a general contractor to construct the new ECB premises". European Central Bank. http://www.ecb.int/press/pr/date/2007/html/pr070710_3.en.html. Retrieved 2 August 2007.

- ^ Dougherty, Carter. "In ECB future, a new home to reflect all of Europe". International Herald Tribune. http://www.iht.com/articles/2004/11/16/ecb_ed3_.php. Retrieved 2 August 2007.

External links

- European Central Bank, official website.

- Central Bank Rates, Europe Interest Rates data and chart

- New ECB Premises, official website.

- The European Central Bank, European NAvigator.

- European Central Bank: history, role and functions, ECB website.

- Infocheese: ECB

- forex-history.net, historical currency charts based on the data published daily by the ECB.

Categories:- 1998 establishments

- Central banks

- European System of Central Banks

- Eurozone fiscal matters

- Frankfurt

- Institutions of the European Union

- Visitor attractions in Frankfurt

Wikimedia Foundation. 2010.