- Noncentral t-distribution

-

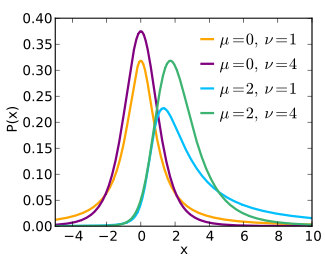

Noncentral Student's t Probability density function

parameters:  degrees of freedom

degrees of freedom

noncentrality parameter

noncentrality parametersupport:

pdf: see text cdf: see text mean: see text mode: see text variance: see text skewness: see text ex.kurtosis: see text In probability and statistics, the noncentral t-distribution (also known as the singly noncentral t-distribution) generalizes Student's t-distribution using a noncentrality parameter. Like the central t-distribution, the noncentral t-distribution is primarily used in statistical inference, although it may also be used in robust modeling for data. In particular, the noncentral t-distribution arises in power analysis.

Contents

Characterization

If Z is a normally distributed random variable with unit variance and zero mean, and V is a Chi-squared distributed random variable with

degrees of freedom that is statistically independent of Z, then

degrees of freedom that is statistically independent of Z, thenis a noncentral t-distributed random variable with

degrees of freedom and noncentrality parameter  . Note that the noncentrality parameter may be negative.

. Note that the noncentrality parameter may be negative.Cumulative distribution function

The cumulative distribution function of noncentral t-distribution with

degrees of freedom and noncentrality parameter can be expressed as [1]where

and

is the cumulative distribution function of the standard normal distribution.

is the cumulative distribution function of the standard normal distribution.

Alternatively, the noncentral t-distribution CDF can be expressed as:

where Γ is the gamma function and I is the regularized incomplete beta function.

Although there are other forms of the cumulative distribution function, the first form presented above is very easy to evaluate through recursive computing.[1] In statistical software R, the cumulative distribution function is implemented as pt.

Probability density function

The probability density function for the noncentral t-distribution with

degrees of freedom and noncentrality parameter can be expressed in several forms.The confluent hypergeometric function form of the density function is

where

is a confluent hypergeometric function.

is a confluent hypergeometric function.An alternative integral form is [2]

A third form of the density is obtained using its cumulative distribution functions, as follows.

This is the approach implemented by the dt function in R.

Properties

Moments of the Noncentral t-distribution

In general, the kth raw moment of the non-central t-distribution is [3]

In particular, the mean and variance of the noncentral t-distribution are

and

Asymmetry

The noncentral t-distribution is asymmetric unless μ is zero, i.e., a central t-distribution. The right tail will be heavier than the left when μ > 0, and vice versa. However, the usual skewness is not generally a good measure of asymmetry for this distribution, because if the degrees of freedom is not larger than 3, the third moment does not exist at all. Even if the degrees of freedom is greater than 3, the sample estimate of the skewness is still very unstable unless the sample size is very large.

Mode

The noncentral t-distribution is always unimodal and bell shaped, but the mode is not analytically available, although it always lies in the interval[4]

-

-

-

when

when  and

and when

when

-

-

Moreover, the mode always has the same sign as the noncentrality parameter

and the negative of the mode is exactly the mode for a noncentral t-distribution with the same number of degrees of freedom but noncentrality parameter

and the negative of the mode is exactly the mode for a noncentral t-distribution with the same number of degrees of freedom but noncentrality parameter

The mode is strictly increasing with

when and strictly decreasing with when In the limit, when approaches zero, the mode is approximated byand when

approaches infinity, the mode is approximated byOccurrences

Use in power analysis

Suppose we have an independent and identically distributed sample

, each of which is normally distributed with mean

, each of which is normally distributed with mean  and variance

and variance  , and we are interested in testing the null hypothesis

, and we are interested in testing the null hypothesis  vs. the alternative hypothesis

vs. the alternative hypothesis  . We can perform a one sample t-test using the test statistic

. We can perform a one sample t-test using the test statisticwhere

is the sample mean and

is the sample mean and  is the unbiased sample variance. Since the right hand side of the second equality exactly matches the characterization of a noncentral t-distribution as described above,

is the unbiased sample variance. Since the right hand side of the second equality exactly matches the characterization of a noncentral t-distribution as described above,  has a noncentral t-distribution with n − 1 degrees of freedom and noncentrality parameter

has a noncentral t-distribution with n − 1 degrees of freedom and noncentrality parameter  .

.If the test procedure rejects the null hypothesis whenever

, where

, where  is the upper

is the upper  quantile of the (central) Student's t-distribution for a pre-specified

quantile of the (central) Student's t-distribution for a pre-specified  , then the power of this test is given by

, then the power of this test is given bySimilar applications of the noncentral t-distribution can be found in the power analysis of the general normal-theory linear models, which includes the above one sample t-test as a special case.

Related distributions

- Central t distribution: The central t-distribution can be converted into a location/scale family. This family of distributions is used in data modeling to capture various tail behaviors. The location/scale generalization of the central t-distribution is a different distribution from the noncentral t-distribution discussed in this article. In particular, this approximation does not respect the asymmetry of the noncentral t-distribution. However, the central t-distribution can be used as an approximation to the non-central t-distribution.[5]

- If is noncentral t-distributed with degrees of freedom and noncentrality parameter and

, then

, then  has a noncentral F-distribution with 1 numerator degree of freedom, denominator degrees of freedom, and noncentrality parameter

has a noncentral F-distribution with 1 numerator degree of freedom, denominator degrees of freedom, and noncentrality parameter  .

.

- If is noncentral t-distributed with degrees of freedom and noncentrality parameter and

, then

, then  has a normal distribution with mean and unit variance.

has a normal distribution with mean and unit variance.

- When the denominator noncentrality parameter of a edit] Special cases

- When

, the noncentral t-distribution becomes the central (Student's) t-distribution with the same degrees of freedom.

, the noncentral t-distribution becomes the central (Student's) t-distribution with the same degrees of freedom.

See also

References

- ^ a b Lenth, Russell V (1989). "Algorithm AS 243: Cumulative Distribution Function of the Non-central t Distribution". Journal of the Royal Statistical Society. Series C (Applied Statistics) 38: 185–189. JSTOR 2347693.

- ^ L. Scharf, Statistical Signal Processing, (Massachusetts: Addison-Wesley, 1991), p.177.

- ^ Hogben, D; Wilk, MB (1961). "The moments of the non-central t-distribution". Biometrika 48: 465–468. JSTOR 2332772.

- ^ van Aubel, A; Gawronski, W (2003). "Analytic properties of noncentral distributions". Applied Mathematics and Computation 141: 3–12. doi:10.1016/S0096-3003(02)00316-8. http://www.sciencedirect.com/science/article/B6TY8-47G44WX-V/2/7705d2642b1a384b13e0578898a22d48.

- ^ Helena Chmura Kraemer; Minja Paik (1979). "A Central t Approximation to the Noncentral t Distribution". Technometrics 21 (3): 357–360. JSTOR 1267759.

External links

- Eric W. Weisstein. "Noncentral Student's t-Distribution." From MathWorld—A Wolfram Web Resource

Some common univariate probability distributions Continuous beta • Cauchy • chi-squared • exponential • F • gamma • Laplace • log-normal • normal • Pareto • Student's t • uniform • WeibullDiscrete List of probability distributions Statistics Descriptive statistics Summary tablesPearson product-moment correlation · Rank correlation (Spearman's rho, Kendall's tau) · Partial correlation · Scatter plotBar chart · Biplot · Box plot · Control chart · Correlogram · Forest plot · Histogram · Q-Q plot · Run chart · Scatter plot · Stemplot · Radar chartData collection Designing studiesDesign of experiments · Factorial experiment · Randomized experiment · Random assignment · Replication · Blocking · Optimal designUncontrolled studiesStatistical inference Frequentist inferenceSpecific testsZ-test (normal) · Student's t-test · F-test · Pearson's chi-squared test · Wald test · Mann–Whitney U · Shapiro–Wilk · Signed-rank · Kolmogorov–Smirnov testCorrelation and regression analysis Errors and residuals · Regression model validation · Mixed effects models · Simultaneous equations modelsNon-standard predictorsPartition of varianceCategorical, multivariate, time-series, or survival analysis Decomposition (Trend · Stationary process) · ARMA model · ARIMA model · Vector autoregression · Spectral density estimationApplications Category · Portal · Outline · Index - When

Categories:- Continuous distributions

![\tilde{F}_{\nu,\mu}(x)=

\Phi(-\mu)+\frac{1}{2}\sum_{j=0}^\infty\left[p_jI_y\left(j+\frac{1}{2},\frac{\nu}{2}\right)+q_jI_y\left(j+1,\frac{\nu}{2}\right)\right],](7/157e51f5fa96d3272cd2216ae8099e69.png)

is the

is the

![f(x)=

\begin{cases}\frac{\nu}{x} \left[F_{\nu+2,\mu}(x\sqrt{1+2/\nu}) - F_{\nu,\mu}(x)\right],

&\mbox{if } x\neq 0 ; \\

\frac{ \Gamma(\,(\nu+1)/2\,)}{\sqrt{\pi\nu} \Gamma(\nu/2)}

\exp\left\{-{\mu^2}/{2}\right\},

&\mbox{if } x=0.

\end{cases}](0/f709336fa0a74865e45078d103f2074f.png)

![\mbox{E}\left[T^k\right]=

\begin{cases}

\left(\frac{\nu}{2}\right)^{\frac{k}{2}}\frac{\Gamma\left(\frac{\nu-k}{2}\right)}{\Gamma\left(\frac{\nu}{2}\right)}\mbox{exp}\left(-\frac{\mu^2}{2}\right)\frac{d^k}{d \mu^k}\mbox{exp}\left(\frac{\mu^2}{2}\right),

& \mbox{if }\nu>k ; \\

\mbox{Does not exist} ,

& \mbox{if }\nu\le k .\\

\end{cases}](2/b628ea03c2310b3742fc141d4936b3b1.png)

![\mbox{E}\left[T\right]=

\begin{cases}

\mu\sqrt{\frac{\nu}{2}}\frac{\Gamma((\nu-1)/2)}{\Gamma(\nu/2)},

&\mbox{if }\nu>1 ;\\

\mbox{Does not exist},

&\mbox{if }\nu\le1 ,\\

\end{cases}](1/561664a2be666be0bc1547d7e3bed88b.png)

![\mbox{Var}\left[T\right]=

\begin{cases}

\frac{\nu(1+\mu^2)}{\nu-2}

-\frac{\mu^2\nu}{2}

\left(\frac{\Gamma((\nu-1)/2)}{\Gamma(\nu/2)}\right)^2 ,

&\mbox{if }\nu>2 ;\\

\mbox{Does not exist},

&\mbox{if }\nu\le2 .\\

\end{cases}](4/d04e8bbb52ced7172435e383fa7c84c0.png)

Wikimedia Foundation. 2010.