- Music industry

-

The music industry or music business sells compositions, recordings and performances of music. Among the many individuals and organizations that operate within the industry are the musicians who compose and perform the music; the companies and professionals who create and sell recorded music (e.g., music publishers, producers, studios, engineers, record labels, retail and online music stores, performance rights organizations); those that present live music performances (booking agents, promoters, music venues, road crew); professionals who assist musicians with their careers (talent managers, business managers, entertainment lawyers); those who broadcast music (satellite and broadcast radio); journalists; educators; musical instrument manufacturers; as well as many others.

In the late 19th century and early 20th century, the music industry was dominated by the publishers of sheet music. By the middle of the century records had supplanted sheet music as the largest player in the music business: in the commercial world people began speaking of "the recording industry" as a loose synonym of "the music industry". Since 2000, sales of recorded music have dropped off substantially,[1] while live music has increased in importance.[2] Three "major corporate labels" dominate recorded music — Universal Music Group (after purchasing EMI in November 2011), Sony Music Entertainment,[3] and Warner Music Group — each of which consists of many smaller companies and labels serving different regions and markets. The live music industry is dominated by Live Nation, the largest promoter and music venue owner. Live Nation is a former subsidiary of Clear Channel Communications, which is the largest owner of radio stations in the United States. Other important music industry companies include Creative Artists Agency (a management and booking company) and Apple Inc. (which runs the world's largest music store, the iTunes Store).[4]

Contents

History

18th Century

Until the 18th century, the processes of formal composition and of the printing of music took place for the most part with the support of patronage from aristocracies and churches. In the mid-to-late 18th century, performers and composers such as Wolfgang Amadeus Mozart began to seek commercial opportunities to market their music and performances to the general public. After Mozart's death, his wife (Constanze Weber) continued the process of commercialization of his music through an unprecedented series of memorial concerts, selling his manuscripts, and collaborating with her second husband, Georg Nissen, on a biography of Mozart.[5]

19th Century

In the 19th century, sheet-music publishers dominated the music industry. In the United States, the music industry arose in tandem with the rise of blackface minstrelsy. In the late part of the century the group of music publishers and songwriters which dominated popular music in the United States became known as Tin Pan Alley.

20th Century

Main article: 20th-century musicAt the dawn of the early 20th century, the recording of sound began to function as a disruptive technology in music markets.[citation needed] With the invention of the phonograph, invented by Thomas Edison in 1877, and the onset of widespread radio communications, the way music is heard was changed forever. Opera houses, concert halls, and clubs continued to produce music and perform live, but the power of radio allowed obscure bands to become popular on a nationwide and sometimes worldwide scale.

The "record industry" eventually replaced the sheet music publishers as the industry's largest force. A multitude of record labels came and went. Some note-worthy labels of the earlier decades include the Columbia Records, Crystalate, Decca Records, Edison Bell, The Gramophone Company, Invicta, Kalliope, Pathé, Victor Talking Machine Company and many others.[6]

Many record companies died out as quickly as they had formed, and by the end of the 1980s, the "Big 6" — EMI, CBS, BMG, PolyGram, WEA and MCA — dominated the industry. Sony bought CBS Records in 1987 and changed its name to Sony Music in 1991. In mid-1998, PolyGram merged into Universal Music Group (formerly MCA), dropping the leaders down to a "Big 5".

Genre-wise, music entrepreneurs expanded their industry models into areas like folk music, in which composition and performance had continued for centuries on an ad hoc self-supporting basis. Forming an independent record label, or "indie" label, continues to be a popular choice for up-and-coming musicians to have their music heard, despite the financial backing associated with major labels.

21st Century

Main article: 2000s in the music industryIn the 21st century, consumers spent less money on recorded music than they had in 1990s, in all formats.[7] Total revenues for CDs, vinyl, cassettes and digital downloads in the world dropped 25% from $38.6 billion in 1999 to $27.5 billion in 2008 according to IFPI. Same revenues in the U.S. dropped from a high of $14.6 billion in 1999 to $10.4 billion in 2008. The Economist and The New York Times report that the downward trend is expected to continue for the foreseeable future[8][9] —Forrester Research predicts that by 2013, revenues in USA may reach as low as $9.2 billion.[8] This dramatic decline in revenue has caused large-scale layoffs inside the industry, driven retailers (such as Tower Records) out of business and forced record companies, record producers, studios, recording engineers and musicians to seek new business models.[10]

The "Big 5" major record companies became the "Big 4" in 2004 when Sony acquired BMG, and the "Big 3" when EMI was acquired by Universal in 2011.

In the early years of the decade, the record industry took aggressive action against illegal file sharing. In 2001 it succeeded in shutting down Napster (the leading on-line source of digital music), and it has threatened thousands of individuals with legal action.[10] This failed to slow the decline in revenue and proved a public-relations disaster.[10] However, some academic studies have suggested that downloads did not cause the decline.[11] Legal digital downloads became widely available with the debut of the iTunes Store in 2003. The popularity of internet music distribution has increased and in 2009 more than a quarter of all recorded music industry revenues worldwide are now coming from digital channels.[12] However, as The Economist reports, "paid digital downloads grew rapidly, but did not begin to make up for the loss of revenue from CDs."[9] The 2008 British Music Rights survey[13] showed that 80% of people in Britain wanted a legal P2P service, however only half of the respondents thought that the music's creators should be paid. The survey was consistent with the results of earlier research conducted in the United States, upon which the Open Music Model was based.[14] According to Nielson Soundscan, by 2009 CDs accounted for 79 percent of album sales, with 20 percent coming from digital, representing both a 10 percent drop and gain for both formats in 2 years.[15]

The turmoil in the recorded music industry changed the twentieth-century balance between artists, record companies, promoters, retail music-stores and the consumer. As of 2010[update], big-box stores such as Wal-Mart and Best Buy sell more records than music-only stores, which have ceased to function as a player in the industry. Recording artists now rely on live performance and merchandise for the majority of their income, which in turn has made them more dependent on music promoters like Live Nation (which dominates tour promotion and owns a large number of music venues.)[2] In order to benefit from all of an artist's income streams, record companies increasingly rely on the "360 deal", a new business-relationship pioneered by Robbie Williams and EMI in 2007.[16] At the other extreme, record companies can offer a simple manufacturing and distribution deal, which gives a higher percentage to the artist, but does not cover the expense of marketing and promotion. Many newer artists no longer see any kind of "record deal" as an integral part of their business plan at all. Inexpensive recording hardware and software made it possible to record reasonable quality music in a bedroom and distribute it over the internet to a worldwide audience.[17] This, in turn, caused problems for recording studios, record producers and audio engineers: the Los Angeles Times reports that as many as half of the recording facilities in that city have failed.[18] Changes in the music industry have given consumers access to a wider variety of music than ever before, at a price that gradually approaches zero.[10] However, consumer spending on music-related software and hardware increased dramatically over the last decade, providing a valuable new income-stream for technology companies such as Apple Inc.

Business structure

The music industry is a complex system of many different organizations, firms and individuals and has undergone dramatic changes in the 21st century. However, the majority of the participants in the music industry still fulfill their traditional roles, which are described below.[19]

Recorded music and compositions

There are three types of property that are created and sold by the recording industry: compositions, recordings and media (such as CDs or MP3s). There may be many recordings of a single composition and a single recording will typically be distributed into many media.

Compositions

Compositions are created by songwriters or composers and are originally owned by the composer. The composer may sell the copyright to another party.[20] Compositions are (traditionally) licensed or "assigned" to publishing companies. A publishing contract specifies the business relationship between the copyright owner and the publishing company. The publishing company (or a collection society operating on behalf of many such publishers, songwriters and composers) collects fees (known as "publishing royalties") when the composition is used. A portion of the royalties are paid by the publishing company to the copyright owner, depending on the terms of the contract. Typically (although not universally), the publishing company will provide the owner with an advance against future earnings when the publishing contract is signed. A publishing company will also promote the compositions, such as by acquiring song "placements" on television or in films.

Recordings

Recordings are created by recording artists, often with the assistance of record producers and audio engineers. They were traditionally made in recording studios (who are paid a daily or hourly rate) in a recording session. In the 21st century, advances in recording technology have allowed many producers and artists to create "home studios", bypassing the traditional role of the recording studio. The record producer oversees all aspects of the recording, making many of the logistic, financial and artistic decisions in cooperation with the artist. Audio engineers (including recording, mixing and mastering engineers) are responsible for the audio quality of the recording. A recording session may also require the services of an arranger or studio musicians.

Recordings are (traditionally) owned by record companies. A recording contract specifies the business relationship between a recording artist and the record company. In a traditional contract, the company provides an advance to the artist who agrees to record music that will be owned by the company. The A&R department of a record company is responsible for finding new talent and overseeing the recording process. The company pays for the recording costs and the cost of promoting and marketing the record. For physical media (such as CDs), the company also pays to manufacture and distribute the physical recordings. Smaller record companies (known as "indies") will form business relationships with other companies to handle many of these tasks. If contractually bound to do so, the record company pays the recording artist a portion of the income from the sale of the recordings, generally known as a mechanical royalty. (This is distinct from the publishing royalty, described above.) This portion is similar to a percentage, but may be limited or expanded by a number of factors (such as free goods, recoupable expenses, bonuses, etc.) that are specified by the record contract. Session musicians and orchestra members (as well as a few recording artists in special markets) are under contract to provide work for hire; they're typically only paid one-time fees or regular wages for their services, rather than royalties.

Physical media

Physical media (such as CDs) are sold by music retailers and are owned by the consumer. A music distributor delivers the physical media from the manufacturer to the retailer and maintains relationships with retailers and record companies. The music retailer pays the distributor, who in turn pays the record company for the recordings. The record company pays mechanical royalties to the publisher, composer, and songwriter via a collection society. The record company then pays royalties, if contractually obligated, to the recording artist. In the case of digital downloads, there is no physical media other than the consumer's hard drive. The distributor is optional in this situation; large online shops may pay the labels directly, but digital distributors do exist to service vendors large and small. When purchasing digital downloads, the consumer may be required to agree to record company and vendor licensing terms beyond those which are inherent in copyright; for example, some may allow freely sharing the recording, but others may restrict the user to storing the music on a specific number of hard drives.

Other uses of recorded music and compositions

Sheet music provides an income stream that is paid exclusively to the composers and their publishing company. When a recording is broadcast (either on radio or by a service such as Muzak), performance rights organisations (such as the ASCAP and BMI in the US or MCPS and PRS in the UK), collect a third type of royalty known as a performance royalty, which is paid to composers and recording artists. This royalty is typically much smaller than publishing or mechanical royalties. When recordings are used in television and film, the composer and their publishing company are typically paid through a synchronization license. Subscription services (such as Rhapsody) also provide an income stream directly to record companies, and through them, to artists, contracts permitting.

Regional variations and industry evolution

The industry is further complicated by the fact that the definition of "royalty" and "copyright" varies from country to country and region to region, which changes the terms of some of these business relationships.

In addition to these traditional business relationships, new ways of doing business are being developed in the 21st century. The traditional lines that once divided artist, publisher, record company, distributor, retail and consumer electronics have become blurred. Artists may own their own publishing companies, artist management companies may promote and market recordings on behalf of their clients, artists may promote and market themselves using only free services such as YouTube or social media, consumer electronics companies have become digital music retailers, and so on, in many variations. New digital music distribution technologies have also forced both government and industry to re-examine the definitions of intellectual property and the rights of all the parties involved.

Live music

A promoter brings together a performing artist and a venue owner and arranges contracts. A booking agency represents the artist to promoters, makes deals and books performances. Consumers usually buy tickets either from the venue or from a ticket distribution service such as Ticketmaster. In the US, Live Nation is the dominant company in all of these roles: they own most of the large venues in the US, they are the largest promoter, and they own Ticketmaster.

Choices about where and when to tour are decided by the artist's management and the artist, sometimes in consultation with the record company. Record companies may provide tour support; they may finance a tour in the hopes that it will help promote the sale of recordings. However, in the 21st century, it has become more common to release recordings to promote tours, rather than book tours to promote records.

Successful artists will usually employ a road crew: a semi-permanent touring organization that travels with the artist. This is headed by a tour manager and provides stage lighting, live sound reinforcement, musical instrument tuning and maintenance and transportation. On large tours, the road crew may also include an accountant, stage manager and catering. Local crews are typically hired to help move equipment on and off stage. On small tours, all of these jobs may be handled by just a few roadies, or by the musicians themselves.

Artist management, representation and staff

Artists may hire a number of people from other fields to assist them with their career. The artist manager oversees all aspects of an artist's career in exchange for a percentage of the artist's income. An entertainment lawyer assists them with the details of their contracts with record companies and other deals. A business manager handles financial transactions, taxes and bookkeeping. Unions, such as AFTRA in the U.S., provide health insurance and other services for musicians.

Other income streams

A successful artist functions in the market as a brand and, as such, may derive income from many other streams, such as merchandise or internet-based services. These are typically overseen by the artist's manager and take the form of relationships between the artist and companies that specialize in these products.

Statistics

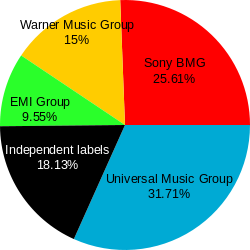

Further information: Global music industry market share data US music market shares, according to Nielsen SoundScan (2005)

US music market shares, according to Nielsen SoundScan (2005)

Nielsen SoundScan reported that the big four accounted for 81.87% of the US music market in 2005:[21]

- Universal Music Group (USA based) — 31.71%

- Sony Music Entertainment (USA based) — 25.61%

- Warner Music Group (USA based) — 15%

- EMI Group (UK based) — 9.55%

- Independent labels — 18.13%

and in 2004, 82.64%:

- Universal Music Group—29.59%

- Sony Music Entertainment—28.46% (13.26% Sony, 15.20% BMG)

- Warner Music Group—14.68%

- EMI Group—9.91%

- Independent labels—17.36%

World music market sales shares, according to IFPI (2005)

World music market sales shares, according to IFPI (2005)The global market was estimated at $30–40 billion in 2004.[22] Total annual unit sales (CDs, music videos, MP3s) in 2004 were 3 billion.

According to an IFPI report published in August 2005,[23] the big four accounted for 71.7% of retail music sales:

- Universal Music Group—25.5%

- Sony Music Entertainment—21.5%

- EMI Group—13.4%

- Warner Music Group—11.3%

- Independent labels—28.3%

Prior to December 1998, the industry was dominated by the "Big Six": Sony Music and BMG had not yet merged, and PolyGram had not yet been absorbed into Universal Music Group. After the PolyGram-Universal merger, the 1998 market shares reflected a "Big Five", commanding 77.4% of the market, as follows, according to MEI World Report 2000:

- Universal Music Group — 28.8%

- Sony Music Entertainment — 21.1%

- EMI — 14.1%

- Warner Music Group — 13.4%

- Independent labels — 22.6%

Note: the IFPI and Nielsen Soundscan use different methodologies, which makes their figures difficult to compare casually, and impossible to compare scientifically.[24]

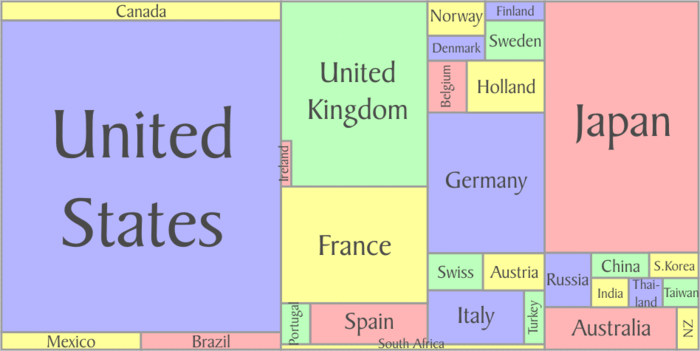

Total value by country

According to the IFPI more than 95% of the total revenue from music in 2003 was derived from the 30 major countries in the proportions shown above, organized roughly by geographic location. In the industry, it is commonly accepted that the three major music markets are the United States, Japan and the United Kingdom.

Albums sales and market value

The following table shows album sales and market value in the world in the 1990s–2000s.

# Country Album Sales Share Share of World Market Value 1 USA 37–40% 30–35% 2 Japan 9–12% 16–19% 3 UK 7–9% 6.4–9.1% 4 Germany 7–8% 5.3–6.4% 5 France 4.5–5.5% 5.4–6.3% 6 Canada 2.6–3.3% 1.9–2.8% 7 Australia 1.5–1.8% 1.5–2.0% 8 Brazil 2.0–3.8% 1.1–3.1% 9 Italy 1.7–2.0% 1.5–2.0% 10 Spain 1.7–2.3% 1.4–1.8% 11 Netherlands 1.2–1.8% 1.3–1.8% 12 Mexico 2.1–4.6% 0.8–1.8% 13 Belgium 0.7–0.8% 0.8–1.2% 14 Switzerland 0.75–0.9% 0.8–1.1% 15 Austria 0.5–0.7% 0.8–1.0% 17 Russia 2.0–2.9% 0.5–1.4% 18 Taiwan 0.9–1.6% 0.5–1.1% 19 Argentina 0.5–0.7% 0.5–1.0% 20 Denmark 0.45–0.65% 0.5–0.8% Singles sales

Physical single sales in the world in the 1990s–2000s and digital single sales in 2005.

# Country Physical Sales Share Digital Sales Share in 2005 EU 34–50% 13.2% 1 UK 26–32% 1.7% 2 Japan 4–25% 85% 3 USA 14.5–16% 6.3% 4 Germany 9–12% 5% 5 France 4–12.5% 1.9% 6 Australia 1.8–4.6% 0.48% 7 Netherlands 1.3–1.7% < 0.2% 8 Belgium 0.8-1.8% < 0.2% 9 Sweden 0.6-0.96% < 0.2% 10 Switzerland 0.5-0.92% < 0.2% 11 Austria 0.58-0.82% < 0.2% 12 Italy 0.3-1.0% < 0.2% 13 Spain 0.3-0.7% < 0.2% 14 Norway 0.3-0.47% < 0.2% 15 Ireland 0.2-0.5% < 0.2% 16 Canada 0.1-0.6% < 0.2% 17 Portugal 0.01-1.0% < 0.2% 18 Republic of Korea 0.02-0.45% < 0.1% 19 New Zealand 0.19-0.29% < 0.1% 20 Denmark 0.10-0.25% < 0.1% Recorded music retail sales

Interim physical retail sales in 2005 - all figures in millions.

Approximately 21% of the gross CD revenue numbers in 2003 can be attributed to used CD sales growing to approximately 27% in 2007 (the growth is attributed to increasing on-line sales of used product by outlets such as Amazon.com, the growth of used music media is expected to continue to grow as the cost of digital downloads continues to rise.)

COUNTRY UNITS VALUE CHANGE Singles CD DVD Total Units $US Local Currency Units Value 1 USA 14.7 300.5 11.6 326.8 4783.2 4783.2 −5.70% −5.30% 2 Japan 28.5 93.7 8.5 113.5 2258.2 239759 −6.90% −9.20% 3 UK 24.3 66.8 2.9 74.8 1248.5 666.7 −1.70% −4.00% 4 Germany 8.5 58.7 4.4 71 887.7 689.7 −7.70% −5.80% 5 France 11.5 47.3 4.5 56.9 861.1 669.1 7.50% −2.70% 6 Italy 0.5 14.7 0.7 17 278 216 −8.40% −12.30% 7 Canada 0.1 20.8 1.5 22.3 262.9 325 0.70% −4.60% 8 Australia 3.6 14.5 1.5 17.2 259.6 335.9 −22.90% −11.80% 9 India – 10.9 – 55.3 239.6 11500 −19.20% −2.40% 10 Spain 1 17.5 1.1 19.1 231.6 180 −13.40% −15.70% 11 Netherlands 1.2 8.7 1.9 11.1 190.3 147.9 −31.30% −19.80% 12 Russia – 25.5 0.1 42.7 187.9 5234.7 −9.40% 21.20% 13 Mexico 0.1 33.4 0.8 34.6 187.9 2082.3 44.00% 21.50% 14 Brazil 0.01 17.6 2.4 24 151.7 390.3 −20.40% −16.50% 15 Austria 0.6 4.5 0.2 5 120.5 93.6 −1.50% −9.60% 16 Switzerland ** 0.8 7.1 0.2 7.8 115.8 139.2 n/a n/a 17 Belgium 1.4 6.7 0.5 7.7 115.4 89.7 −13.80% −8.90% 18 Norway 0.3 4.5 0.1 4.8 103.4 655.6 −19.70% −10.40% 19 Sweden 0.6 6.6 0.2 7.2 98.5 701.1 −29.00% −20.30% 20 Denmark 0.1 4 0.1 4.2 73.1 423.5 3.70% −4.20% Top 20 74.5 757.1 42.8 915.2 12378.7 −6.60% −6.30% In its June 30, 2000 annual report filed with the U.S. Securities and Exchange Commission, Seagram reported that Universal Music Group made 40% of the worldwide classical music sales over the preceding year.[25]

Music industry organizations

- Academy of Country Music aka ACM

- Alliance of Artists and Recording Companies aka AARC

- American Association of Independent Music aka A2IM

- American Federation of Musicians aka AFM

- American Federation of Television and Radio Artists aka AFTRA

- American Society of Composers, Authors and Publishers aka ASCAP

- Asosiasi Industri Rekaman Indonesia aka ASIRI

- Association of Independent Music aka AIM

- Australian Recording Industry Association aka ARIA

- Billboard Magazine, known for the Billboard Hot 100

- British Phonographic Industry (BPI)

- Broadcast Music Incorporated aka BMI

- Canadian Recording Industry Association (CRIA)

- Country Music Association

- Federation of the Italian Music Industry (FIMI)

- Gesellschaft für musikalische Aufführungs- und mechanische Vervielfältigungsrechte (GEMA) in Germany

- Harry Fox Agency (for-profit branch of the NMPA)

- Indian Music Industry (IMI)

- International Federation of the Phonographic Industry (IFPI)

- Irish Recorded Music Association (IRMA)

- Latin Academy of Recording Arts & Sciences (LARAS)

- Mechanical-Copyright Protection Society (MCPS)

- Musicians' Union

- National Academy of Recording Arts and Sciences (NARAS)

- National Association of Recording Merchandisers (NARM)

- National Music Publishers Association (NMPA)

- Philippine Association of the Record Industry (PARI)

- PRS for Music

- Recording Artists' Coalition aka RAC

- Recording Industry Association of America (RIAA)

- Recording Industry Association of Japan (RIAJ)

- Recording Industry Association of New Zealand (RIANZ)

- Recording Industry of South Africa (RISA)

- Society of European Stage Authors & Composers (SESAC)

- SoundExchange

See also

- List of record labels and Category:Record labels

- List of best-selling music artists – World's top-selling music artists chart.

- MIDEM –The World's Music market.

- Album cover

- Music Directory Canada (book)

Notes

- ^ "The Music Industry". The Economist. October 15, 2008. http://www.economist.com/background/displayBackground.cfm?story_id=10498664.

- ^ a b Seabrook, John (August 10, 2009). "The Price of the Ticket". The New Yorker. Annals of Entertainment: 34. http://www.newyorker.com/reporting/2009/08/10/090810fa_fact_seabrook.

- ^ Sony Corporation announced October 1, 2008 that it had completed the acquisition of Bertelsmann’s 50% stake in Sony BMG, which was originally announced on August 5, 2008. Ref: "Sony's acquisition of Bertelsmann's 50% Stake in Sony BMG complete." (Press release). Sony Corporation of America. http://www.sony.com/SCA/press/081001.shtml.

- ^ "Mobile World Congress 2011". dailywireless.org. February 14, 2011. http://www.dailywireless.org/2011/02/14/mobile-world-congress-2011/. ""Amazon is now the world’s biggest book retailer. Apple, the world’s largest music retailer.""

- ^ Dear Constanze The Guardian

- ^ http://www.angelfire.com/band/vintage78rpm/great78/Early_Record_Labels.htm Early record companies

- ^ McCardle, Megan (May 2010). "The Freeloaders". The Atlantic. http://www.theatlantic.com/magazine/archive/2010/05/the-freeloaders/8027/. Retrieved 2010-12-10. "industry revenues have been declining for the past 10 years"

- ^ a b Arango, Tim (November 25, 2008). "Digital Sales Surpass CDs at Atlantic". The New York Times. http://www.nytimes.com/2008/11/26/business/media/26music.html. Retrieved July 6, 2009.

- ^ a b "The music industry". The Economist. Jan 10, 2008. http://www.economist.com/business/displaystory.cfm?story_id=E1_TDQJRGGQ.

- ^ a b c d Knopper, Steve (2009). Appetite for Self-Destruction: the Spectacular Crash of the Record Industry in the Digital Age. Free Press. ISBN 1416552154.

- ^ Borland, John (March 29, 2004). "Music sharing doesn't kill CD sales, study says". C Net. http://news.cnet.com/2100-1027_3-5181562.html. Retrieved July 6, 2009.

- ^ "IFPI publishes Digital Music Report 2010". The International Federation of the Phonographic Industry. http://www.ifpi.org/content/section_resources/dmr2010.html.

- ^ Andrew Orlowski. 80% want legal P2P - survey. The Register, 2008.

- ^ Shuman Ghosemajumder. Advanced Peer-Based Technology Business Models. MIT Sloan School of Management, 2002.

- ^ France, Lisa (2010-07-20). "Is the death of the CD looming?". CNN. http://edition.cnn.com/2010/SHOWBIZ/Music/07/19/cd.digital.sales/index.html. Retrieved 2011-11-03.

- ^ Rosso, Wayne (January 16, 2009). "Perspective: Recording industry should brace for more bad news". CNET. http://news.cnet.com/Recording-industry-should-brace-for-more-bad-news/2010-1027_3-6226487.html. Retrieved 2009.

- ^ Jefferson Graham (October 14, 2009). "Musicians ditch studios for tech such as GiO for Macs". U.S.A. Today. http://www.usatoday.com/tech/news/2009-10-13-apogee-gio-music_N.htm.

- ^ Nathan Olivarez-Giles (October 13, 2009). "Recording studios are being left out of the mix". The Los Angeles Times. http://www.latimes.com/business/la-fi-smallbiz-studios13-2009oct13,0,3516140.story.

- ^ All of the information in this section can be found in:

- Krasilovsky, M. William; Shemel, Sidney; Gross, John M.; Feinstein, Jonathan, This Business of Music (10th ed.), Billboard Books, ISBN 0823077292

- ^ In the case of work for hire, the composition is owned immediately by another party.

- ^ Paul Cashmere (Jan. 5, 2006). "Universal Is The Biggest Music Company of 2005". Undercover (Australia). http://www.undercover.com.au/News-Story.aspx?id=1215. Retrieved May 27, 2006.

- ^ According to the RIAA the world music market is estimated at $40 billion, but according to IFPI (2004) it is estimated at $32 billion.

- ^ IFPI releases definitive statistics on global market for recorded music

- ^ [1]"Digital Music Futures and the Independent Music Industry", Clicknoise, February 1, 2007.

- ^ BUSINESS AND PROPERTIES The Seagram Company Ltd.

References

- Krasilovsky, M. William; Shemel, Sidney; Gross, John M.; Feinstein, Jonathan, This Business of Music (10th ed.), Billboard Books, ISBN 0823077292

Further reading

- Lebrecht, Norman: When the Music Stops: Managers, Maestros and the Corporate Murder of Classical Music, Simon & Schuster 1996

- Imhorst, Christian: The ‘Lost Generation’ of the Music Industry, published under the terms of the GNU Free Documentation License 2004

- Gerd Leonhard: Music Like Water – the inevitable music ecosystem

- The Methods Reporter: Music Industry Misses Mark with Wrongful Suits

- Music CD Industry – a mid-2000 overview put together by Duke University undergraduate students

- d’Angelo, Mario: Does globalisation mean ineluctable concentration ? in The Music Industry in the New Economy, Report of the Asia-Europe Seminar, Lyon, Oct. 25–28, 2001, IEP de Lyon/Asia-Europe Foundation/Eurical, Editors Roche F., Marcq B., Colomé D., 2002, pp. 53–54.

- d'Angelo, Mario: Perspectives of the Management of Musical Institutions in Europe, OMF, Musical Activities and Institutions Sery, ParisIV-Sorbonne University, Ed. Musicales Aug. Zurfluh, Bourg-la-Reine, 2006.

- The supply of recorded music: A report on the supply in the UK of prerecorded compact discs, vinyl discs and tapes containing music. Competition Commission, 1994.

- Tschmuck, Peter: Creativity and Innovation in the Music Industry, Springer 2006.

- Ulrich Dolata: The Music Industry and the Internet. A Decade of Disruptive and Uncontrolled Sectoral Change. Research Contributions to Organizational Sociology and Innovation Studies. Discussion Paper 2011-02. full text online

External links

- New York Metro article by Michael Wolff analyzing the decline of the record industry

- Salon article on Courtney Love's criticism of record industry business practices

- Federal Trade Commission press release regarding price fixing

- Antitrust settlement in Nevada price-fixing case

- Songwriter Janis Ian's critique of the record industry's policies

- The Net is the Independent Artist's Radio – August 10, 2005 MP3 Newswire article

- Music Downloads: Pirates- or Customers?. Silverthorne, Sean. Harvard Business School Working Knowledge, 2004.

- The British Library - Music Industry Guide (sources of information)

- The ASCAP Resource Guide: Recording Industry

- BPI: Music business – Industry Structure

- Academic articles about the music industry The Music Business Journal

Music History of music Prehistoric · Ancient · Biblical · Medieval · Renaissance · Baroque · Classical period · Romantic · 20th century · Contemporary · 21st century

Composition Education and careers Production Cultural and regional genres of music African (Central African · East African · North African · Southern African · West African) · Asian (Central Asian · East Asian · Middle Eastern · South Asian · Southeast Asian) · European (Central European · Eastern European · Northern European · Southeastern European · Southern European · Western European) · Latin American (Central American · South American) · North American (Canadian · Caribbean · United States) · Oceanian (Australian · Melanesian · Micronesian · New Zealand · Polynesian)Lists Index · Glossary of jazz and popular musical terms · Glossary of musical terminology · Outline · Musical forms by era · Instruments · AudioRelated topics Category · Portal · WikiProject Categories:

Wikimedia Foundation. 2010.