- Government debt

-

Tax policy · Budgetary policy

Tax policy · Budgetary policy

Revenue · Spending · Budget

Deficit or Surplus · Deficit spending

Debt (External · Internal)

Finance ministry · Fiscal unionTariff · Non-tariff barrier

Balance of trade · Gains from trade

Trade creation · Trade diversion

Protectionism · Free trade

Commerce ministry · Trade blocReformGovernment debt (also known as public debt, national debt, sovereign debt)[1][2] is money (or credit) owed by a central government. In the US, "government debt" may also refer to the debt of a municipal or local government. By contrast, annual "government deficit" refers to the difference between government receipts and spending in a single year, that is, the increase of debt over a particular year.

As the government draws its income from much of the population, government debt is an indirect debt of the taxpayers. Government debt can be categorized as internal debt (owed to lenders within the country) and external debt (owed to foreign lenders). Governments usually borrow by issuing securities, government bonds and bills. Less creditworthy countries sometimes borrow directly from supranational institutions.

A broader definition of government debt considers all government liabilities, including future pension payments and payments for goods and services the government has contracted but not yet paid.

Another common division of government debt is by duration until repayment is due. Short term debt is generally considered to be for one year or less, long term is for more than ten years. Medium term debt falls between these two boundaries.

Contents

Government and sovereign bonds

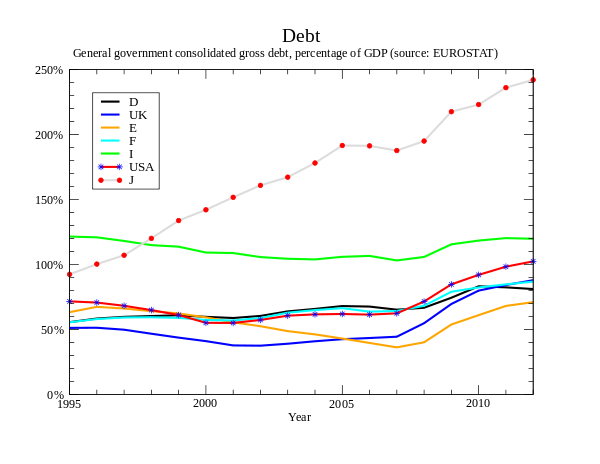

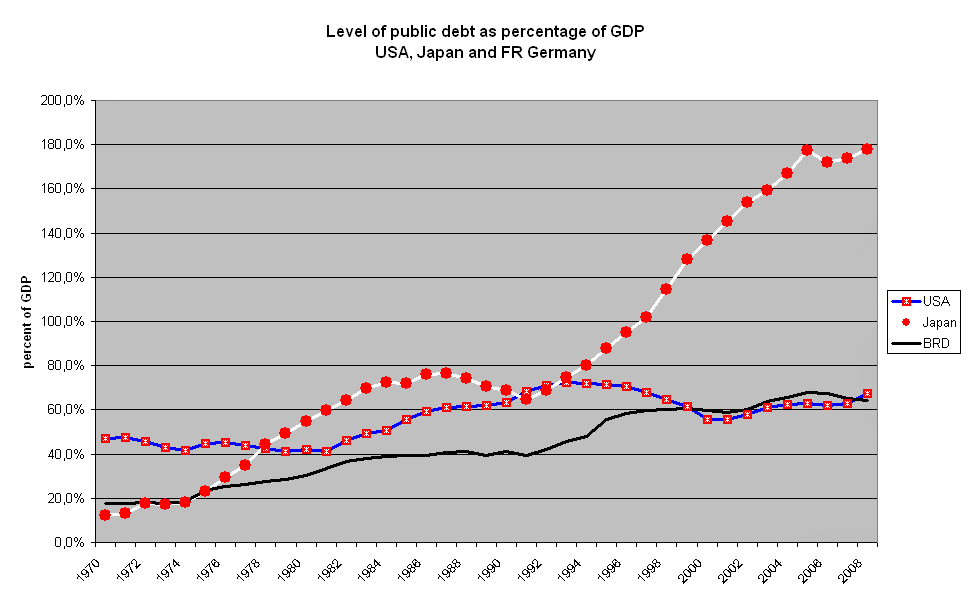

Main article: government bond Public debt as a percent of GDP, evolution for USA, Japan and the main EU economies.

Public debt as a percent of GDP, evolution for USA, Japan and the main EU economies.

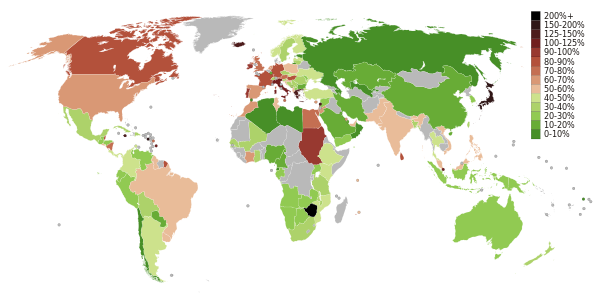

Public debt as a percent of GDP (2010).

Public debt as a percent of GDP (2010).A government bond is a bond issued by a national government. Such bonds are often denominated in the country's domestic currency. Bonds issued by national governments in foreign currencies are normally referred to as sovereign bonds.

Government bonds are sometimes regarded as risk-free bonds, because national governments can raise taxes or reduce spending up to a certain point; in many cases they "print more money" to redeem the bond at maturity. (Some governments are not currently entitled to print money directly, but only through a Central bank at interest[clarification needed].)

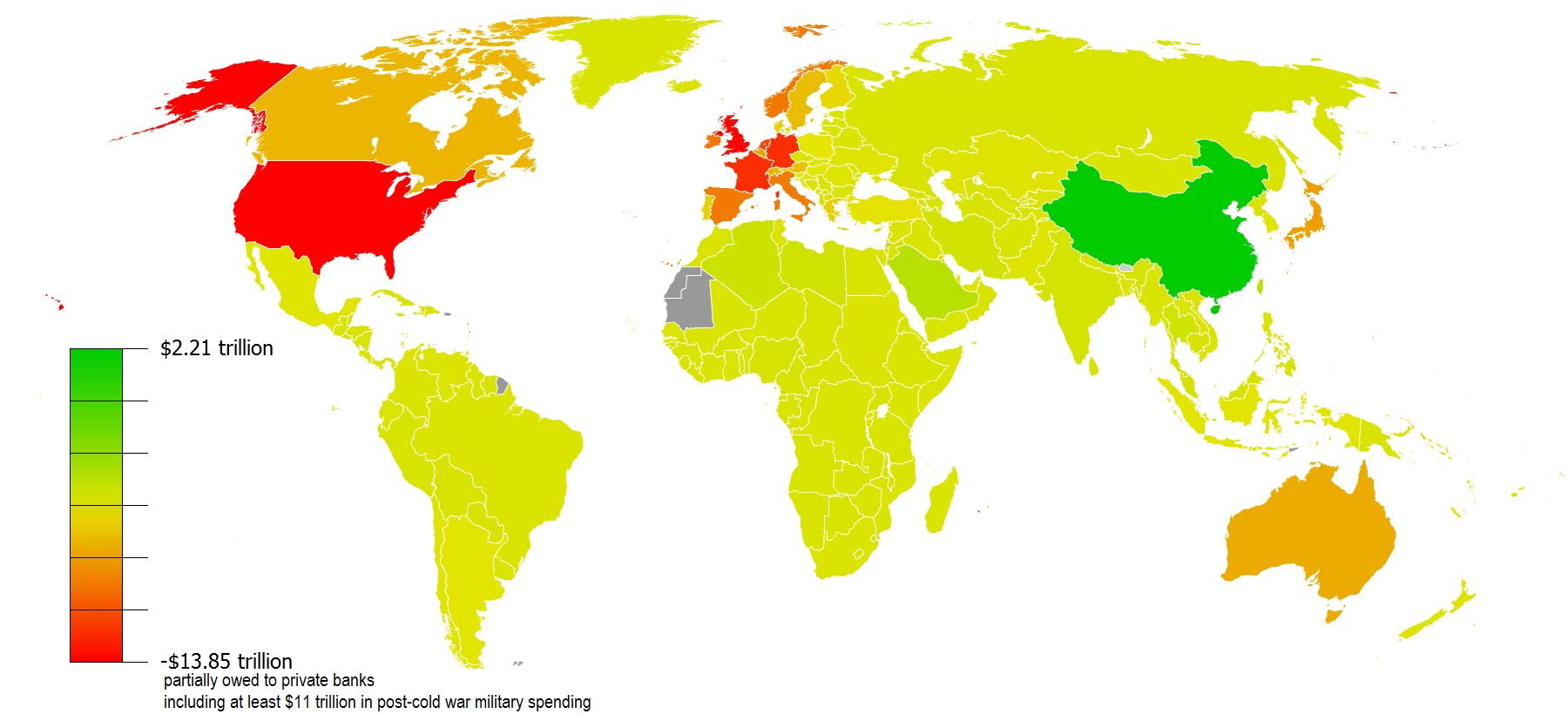

Foreign currency reserves and gold minus external debt based on 2010 data from CIA Factbook.

Foreign currency reserves and gold minus external debt based on 2010 data from CIA Factbook.Investors in sovereign bonds denominated in foreign currency have the additional risk that the issuer may be unable to obtain foreign currency to redeem the bonds.

Public Debt Top 20, 2010 estimate (CIA World Factbook 2011)[3] Country Public Debt

(billion USD)% of GDP per capita (USD) Note (2008 estimate)

(billion USD) USA

USA$ 9,133 62% $ 29,158 ($ 5,415, 38%)  Japan

Japan$ 8,512 198% $ 67,303 ($ 7,469, 172%)  Germany

Germany$ 2,446 83% $ 30,024 ($ 1,931, 66%)  Italy

Italy$ 2,113 119% $ 34,627 ($ 1,933, 106%)  India

India$ 2,107 52% $ 1,772 ($ 1,863, 56%)  China

China$ 1,907 19% $ 1,427 ($ 1,247, 16%)  France

France$ 1,767 82% $ 27,062 ($ 1,453, 68%)  UK

UK$ 1,654 76% $ 26,375 ($ 1,158, 52%)  Brazil

Brazil$ 1,281 59% $ 6,299 ($ 775, 39%)  Canada

Canada$ 1,117 84% $ 32,829 ($ 831, 64%)  Spain

Spain$ 823 60% $ 17,598 ($ 571, 41%)  Mexico

Mexico$ 577 37% $ 5,071 ($ 561, 36%)  Greece

Greece$ 454 143% $ 42,216 ($ 335, 97%)  Netherlands

Netherlands$ 424 63% $ 25,152 ($ 392, 58%)  Turkey

Turkey$ 411 43% $ 5,218 ($ 362, 40%)  Belgium

Belgium$ 398 101% $ 38,139 ($ 350, 90%)  Egypt

Egypt$ 398 80% $ 4,846 ($ 385, 87%)  Poland

Poland$ 381 53% $ 9,907 ($ 303, 45%)  South Korea

South Korea$ 331 23% $ 6,793 ($ 326, 24%)  Singapore

Singapore$ 309 106% $ 65,144  Taiwan

Taiwan$ 279 34% $ 12,075 Public Debt is total of all government borrowings less repayments that are denominated in a country's home currency. * CIA's World Factbook list only percentage of GDP, the debt amount and per capita is calculated with GDP (PPP) and population figures of same report.

See also: List of sovereign states by public debtMunicipal, provincial, or state bonds

Further information: Municipal bondMunicipal bonds, "munis" in the United States, are debt securities issued by local governments (municipalities).

Denominated in reserve currencies

Governments often borrow money in a currency in which the demand for debt securities is strong. An advantage of issuing bonds in a currency such as the US dollar, the pound sterling, or the euro is that many investors wish to invest in such bonds. Countries such as the United States, Germany, Italy and France have only issued in their domestic currency (or in the Euro in the case of Euro members).

Relatively few investors are willing to invest in currencies that do not have a long track record of stability. A disadvantage for a government issuing bonds in a foreign currency is that there is a risk that it will not be able to obtain the foreign currency to pay the interest or redeem the bonds. In 1997 and 1998, during the Asian financial crisis, this became a serious problem when many countries were unable to keep their exchange rate fixed due to speculative attacks.

Risk

Main article: Credit riskLending to a national government in the country's own sovereign currency is often considered "risk free" and is done at a so-called "risk-free interest rate." This is because, up to a point, the debt and interest can be repaid by raising tax receipts (either by economic growth or raising tax rates), a reduction in spending, or failing that by simply printing more money. It is widely considered that this would increase inflation and reduce the value of the invested capital. This has happened many times throughout history, and a typical example of this is provided by Weimar Germany of the 1920s which suffered from hyperinflation due to its government's inability to pay the national debt deriving from the costs of World War I.

In practice, the market interest rate tends to be different for debts of different countries. An example is in borrowing by different European Union countries denominated in euros. Even though the currency is the same in each case, the yield required by the market is higher for some countries' debt than for others. This reflects the views of the market on the relative solvency of the various countries and the likelihood that the debt will be repaid.

A politically unstable state is anything but risk-free as it may—being sovereign—cease its payments. Examples of this phenomenon include Spain in the 16th and 17th centuries, which nullified its government debt seven times during a century, and revolutionary Russia of 1917 which refused to accept the responsibility for Imperial Russia's foreign debt.[4] Another political risk is caused by external threats. It is mostly uncommon for invaders to accept responsibility for the national debt of the annexed state or that of an organization it considered as rebels. For example, all borrowings by the Confederate States of America were left unpaid after the American Civil War. On the other hand, in the modern era, the transition from dictatorship and illegitimate governments to democracy does not automatically free the country of the debt contracted by the former government. Today's highly developed global credit markets would be less likely to lend to a country that negated its previous debt, or might require punishing levels of interest rates that would be unacceptable to the borrower.

U.S. Treasury bonds denominated in U.S. dollars are often considered "risk free" in the U.S. This disregards the risk to foreign purchasers of depreciation in the dollar relative to the lender's currency. In addition, a risk-free status implicitly assumes the stability of the US government and its ability to continue repayments during any financial crisis.

Lending to a national government in a currency other than its own does not give the same confidence in the ability to repay, but this may be offset by reducing the exchange rate risk to foreign lenders. On the other hand, national debt in foreign currency cannot be disposed of by starting a hyperinflation; and this increases the credibility of the debtor. Usually small states with volatile economies have most of their national debt in foreign currency. For countries in the Eurozone, the euro is the local currency, although no single state can trigger inflation by creating more currency.

Lending to a local or municipal government can be just as risky as a loan to a private company, unless the local or municipal government has sufficient power to tax. In this case, the local government could to a certain extent pay its debts by increasing the taxes, or reduce spending, just as a national one could. Further, local government loans are sometimes guaranteed by the national government, and this reduces the risk. In some jurisdictions, interest earned on local or municipal bonds is tax-exempt income, which can be an important consideration for the wealthy.

Clearing and defaults

Public debt clearing standards are set by the Bank for International Settlements, but defaults are governed by extremely complex laws which vary from jurisdiction to jurisdiction. Globally, the International Monetary Fund can take certain steps to intervene to prevent anticipated defaults. It is sometimes criticized for the measures it advises nations to take, which often involve cutting back on government spending as part of an economic austerity regime. In triple bottom line analysis, this can be seen as degrading capital on which the nation's economy ultimately depends.

Those considerations do not apply to private debts, by contrast: credit risk (or the consumer credit rating) determines the interest rate, more or less, and entities go bankrupt if they fail to repay. Governments cannot really go bankrupt (and suddenly stop providing services to citizens), thus a far more complex way of managing defaults is required.

Smaller jurisdictions, such as cities, are usually guaranteed by their regional or national levels of government. When New York City declined into what would have been a bankrupt status during the 1960s (had it been a private entity), by the early 1970s a "bailout" was required from New York State and the United States. In general, such measures amount to merging the smaller entity's debt into that of the larger entity and thereby giving it access to the lower interest rates the larger entity enjoys. The larger entity may then assume some agreed-upon oversight in order to prevent recurrence of the problem.

Structure

In the dominant economic policy generally ascribed to theories of John Maynard Keynes, sometimes called Keynesian economics, there is tolerance for fairly high levels of public debt to pay for public investment in lean times, which, if boom times follow, can then be paid back from rising tax revenues.

As this theory gained global popularity in the 1930s, many nations took on public debt to finance large infrastructural capital projects — such as highways or large hydroelectric dams. It was thought that this could start a virtuous cycle and a rising business confidence since there would be more workers with money to spend. Some have argued that the greatly increased military spending of World War II really ended the Great Depression. Of course, military expenditures are based upon the same tax (or debt) and spend fundamentals as the rest of the national budget, so this argument does little to undermine Keynesian theory. Indeed, some[who?] have suggested that significantly higher national spending necessitated by war essentially confirms the basic Keynesian analysis (see Military Keynesianism).

Nonetheless, the Keynesian scheme remained dominant, thanks in part to Keynes' own pamphlet How to Pay for the War, published in the United Kingdom in 1940. Since the war was being paid for, and being won, Keynes and Harry Dexter White, Assistant Secretary of the United States Department of the Treasury, were, according to John Kenneth Galbraith, the dominating influences on the Bretton Woods agreements. These agreements set the policies for the Bank for International Settlements (BIS), International Monetary Fund (IMF), and World Bank, the so-called Bretton Woods Institutions, launched in the late 1940s for the last two (the BIS was founded in 1930).

These are the dominant economic entities setting policies regarding public debt. Due to its role in setting policies for trade disputes, the World Trade Organization also has immense power to affect foreign exchange relations, as many nations are dependent on specific commodity markets for the balance of payments they require to repay debt.

Understanding the structure of public debt and analyzing its risk requires one to:

- Assess the expected value of any public asset being constructed, at least in future tax terms if not in direct revenues. A choice must be made about its status as a public good — some public "assets" end up as public bads, such as nuclear power plants which are extremely expensive to decommission — these costs must also be worked in to asset values.

- Determine whether any public debt is being used to finance consumption, which includes all social assistance and all military spending.

- Determine whether triple bottom line issues are likely to lead to failure or defaults of governments — say due to being overthrown.

- Determine whether any of the debt being undertaken may be held to be odious debt, which might permit it to be disavowed without any effect on a country's credit status. This includes any loans to purchase "assets" such as leaders' palaces, or the people's suppression or extermination. International law does not permit people to be held responsible for such debts — as they did not benefit in any way from the spending and had no control over it.

- Determine if any future entitlements are being created by expenditures — financing a public swimming pool for instance may create some right to recreation where it did not previously exist, by precedent and expectations.

Scale

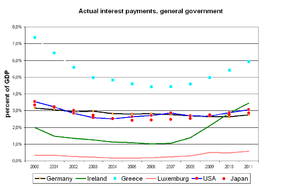

Interest burden of public debt with respect to GDP.

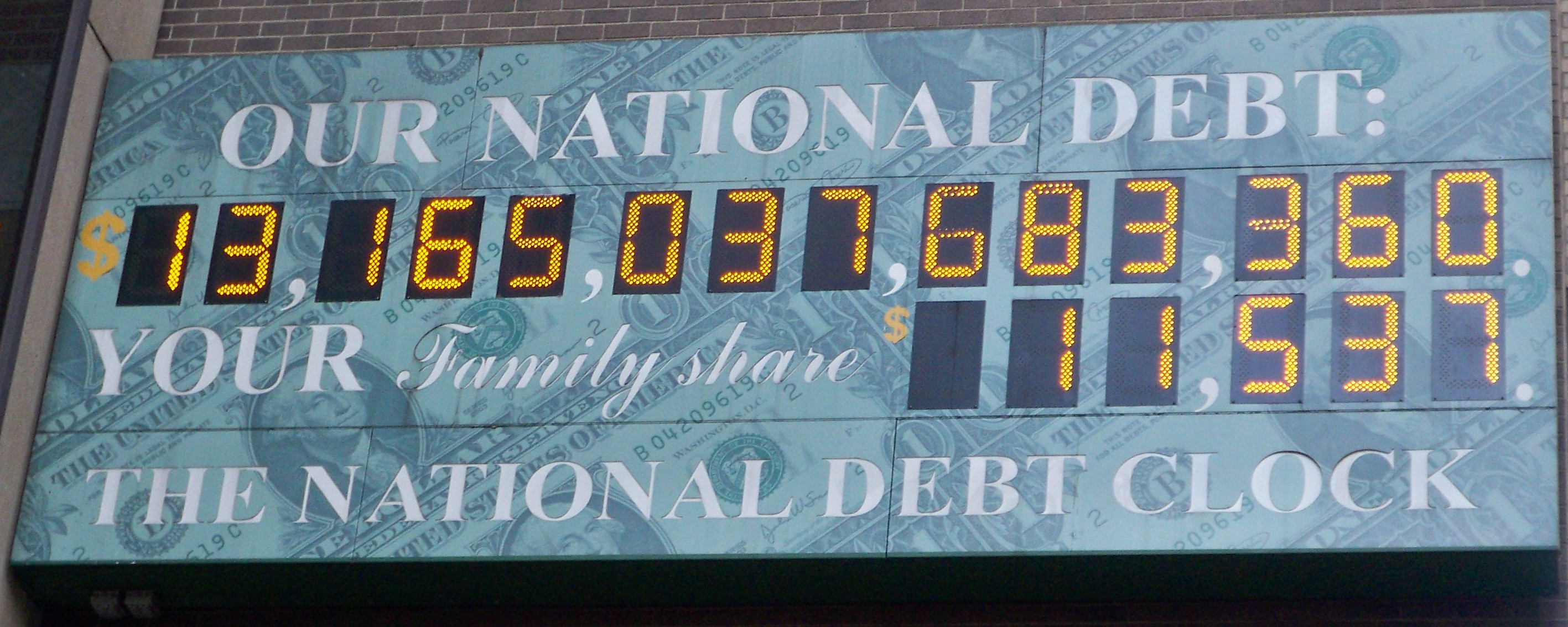

Interest burden of public debt with respect to GDP. National Debt Clock outside the IRS office in NYC, July 1, 2010

National Debt Clock outside the IRS office in NYC, July 1, 2010Global debt is of great concern since interest payments can often place great demands on governments and individuals. This has led to calls for universal debt relief for poorer countries.

A less extreme and more innovative measure would be to permit civil society groups in every nation to buy the debt in exchange for minority equity positions in community organizations. Even in dictatorships, the combination of banks and civil society power could force land reform and overthrow unaccountable governments, since the people and banks would be aligned against the oppressive government.

Using a debt to GDP ratio is one of the most accepted measures of assessing a nation's debt. For example, in theory one of the criteria of admission to the European Union's Euro currency is that a country's debt should not exceed 60% of that country's GDP.

The debt of the United States over time is documented online at the Department of the Treasury's website TreasuryDirect.[5]

Problems

Sovereign debt problems have been a major public policy issue since World War II, including the treatment of debt related to that war, the developing country "debt crisis" in the 1980s, and the shocks of the 1998 Russian financial crisis and Argentina's default in 2001.

Not all so-called developing countries have been affected to the same extent. For example Yugoslavia had low government debt (perhaps because it was unable to borrow on world markets) until its breakup and the coming of democracy, when the new national governments started to borrow money from the IMF. Croatia has a government debt of $47 billion today while the whole of Yugoslavia (six times as many people as Croatia) in 1980 had debt of $14 billion.[citation needed]

Implicit debt

Government "implicit" debt is the promise by a government of future payments from the state. Usually this refers to long term promises of social payments such as pensions and health expenditure; not promises of other expenditure such as education or defense (which are largely paid on a "quid pro quo" basis to government employees and contractors).

A problem with these implicit government insurance liabilities is that it is hard to cost them accurately, since the amounts of future payments depend on so many factors. First of all, the social security claims are not "open" bonds or debt papers with a stated time frame, "time to maturity", "nominal value", or "net present value".

In the United States, as in most other countries, there is no money earmarked in the government's coffers for future social insurance payments. This insurance system is called PAYGO (pay-as-you-go). Alternative social insurance strategies might have included a system that involved save and invest.

Furthermore, population projections predict that when the "baby boomers" start to retire the working population in the United States, and in many other countries, will be a smaller percentage of the population than it is now, for many years to come. This will increase the burden on the country of these promised pension and other payments - larger than the 65 percent[6] of GDP that it is now. The "burden" of the government is what it spends, since it can only pay its bills through taxes, debt, and increasing the money supply (government spending = tax revenues + change in government debt held by public + change in monetary base held by the public). "Government social benefits" paid by the United States government during 2003 totaled $1.3 trillion.[7]

In 2010 the European Commission required EU Member Countries to publish their debt information in standardized methodology, explicitly including debts that were previously hidden in a number of ways to satisfy minimum requirements on local (national) and European (Stability and Growth Pact) level.[8]By country

See also

- 2010 European sovereign debt crisis

- Bond (finance)

- Brady Bonds

- Credit default swap

- Developing countries' debt

- External debt

- Financial repression

- Fiscal policy

- Generational accounting

- Government budget deficit

- Government investment

- Government spending

- Hedge fund

- Investment bond

- Public finance

- Sovereign bond

- Speculation

- Tax

- Taxpayers union

- United States public debt

- Warrant (of Payment)

References

- ^ "Bureau of the Public Debt Homepage". United State Department of the Treasury. Accessed October 12, 2010. http://www.publicdebt.treas.gov/.

- ^ "FAQs: National Debt". United State Department of the Treasury. Accessed October 12, 2010. http://www.ustreas.gov/education/faq/markets/national-debt.shtml.

- ^ "Country Comparison :: Public debt". cia.gov. https://www.cia.gov/library/publications/the-world-factbook/rankorder/2186rank.html. Retrieved November 8, 2011.

- ^ Hedlund, Stefan (2004). "Foreign Debt". Encyclopedia of Russian History (reprinted in Encyclopedia.com). http://www.encyclopedia.com/doc/1G2-3404100454.html. Retrieved 3 March 2010.

- ^ "Government - Historical Debt Outstanding – Annual". Treasurydirect.gov. 2010-10-01. http://www.treasurydirect.gov/govt/reports/pd/histdebt/histdebt.htm. Retrieved 2011-11-08.

- ^ "Report for Selected Countries and Subjects". International Monetary Fund. http://www.imf.org/external/pubs/ft/weo/2008/02/weodata/weorept.aspx?sy=2004&ey=2009&ssd=1&sort=country&ds=.&br=0&pr1.x=59&pr1.y=16&c=193%2C542%2C122%2C137%2C124%2C181%2C156%2C138%2C423%2C196%2C128%2C142%2C172%2C182%2C132%2C576%2C134%2C961%2C174%2C184%2C532%2C144%2C176%2C146%2C178%2C528%2C436%2C112%2C136%2C111%2C158&s=GGD_NGDP&grp=0&a=. Retrieved 2010-10-12.(General government gross debt 2008 estimates rounded to one decimal place)

- ^ "Government Social Benefits Table". http://www.bea.doc.gov/bea/dn/nipaweb/TableView.asp?SelectedTable=84&FirstYear=2002&LastYear=2004&Freq=Qtr.[dead link]

- ^ "COUNCIL REGULATION (EC) No 479/2009". http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2009:145:0001:0009:en:PDF. Retrieved 2011-11-08.

External links

- The IMF Public Financial Management Blog

- OECD government debt statistics

- Canadian Taxpayers Federation debt clock

- French public debt clock

- UK national debt clock

- Germany's taxpayers union and debt clock (at the top of the page)

- Japan's national debt

- Riksgäldskontoret – Swedish national debt office

- United States Treasury, Bureau of Public Debt — The Debt to the Penny and Who Holds It

- The US National Debt Clock by Ed Hall

- Slaying the Dragon of Debt, Regional Oral History Office, The Bancroft Library, University of California, Berkeley

- National debt: Country comparison

Databases

- Public Debt Database A complete listing of all Public Debt securities issued by the United States Treasury and its predecessors between 1775 and 1976.

- CLYPS dataset on public debt level and composition in Latin America

Debt Debt instruments Managing debt Bankruptcy · Consolidation · Debt management plan · Debt relief · Debt restructuring · Debt-snowball method · DIP financingDebt collection and evasion Bad debt · Charge-off · Collection agency · Debt bondage · Debt compliance · Debtors' prison · Garnishment · Phantom debt · Strategic default · Tax refund interceptionDebt markets Consumer debt · Corporate debt · Deposit account · Debt buyer · Fixed income · Government debt · Money market · Municipal debt · Securitization · Venture debtDebt in economics Default · Insolvency · Interest · Interest rate Categories:

Wikimedia Foundation. 2010.