- Credit (finance)

-

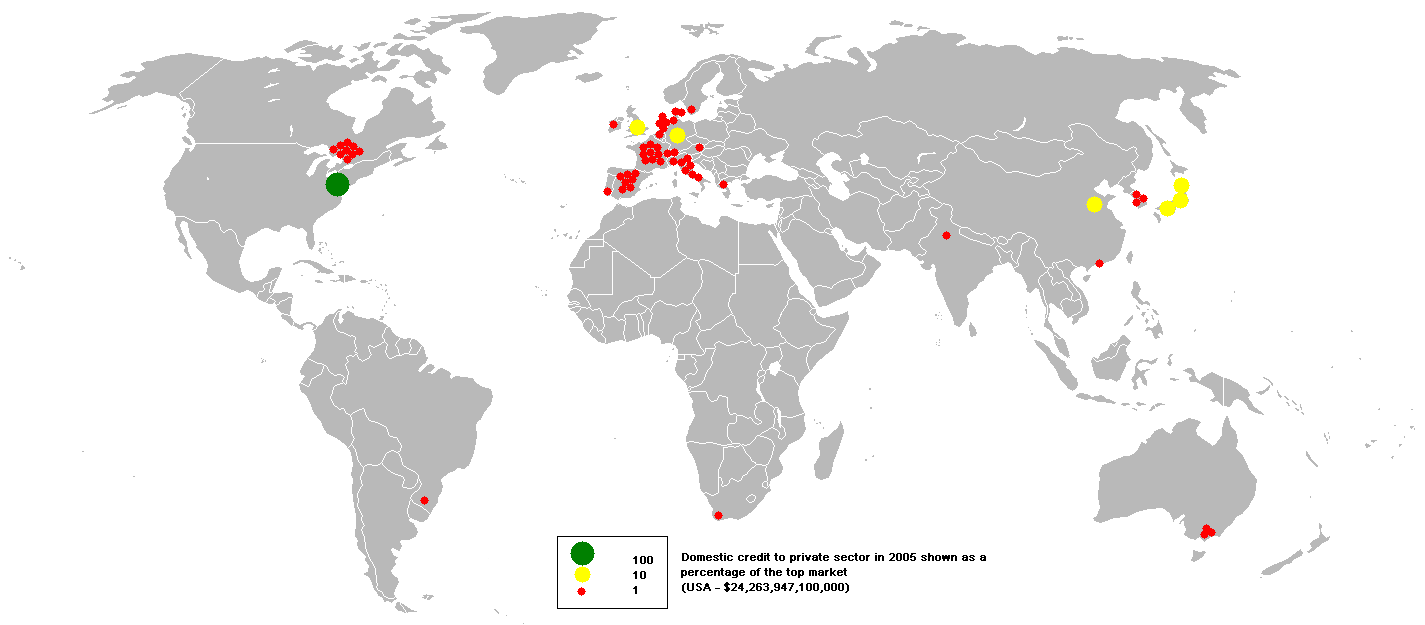

Domestic credit to private sector in 2005

Domestic credit to private sector in 2005

Finance Government spending:

Government final consumption expenditure

Warrant of payment

Government operations

Redistribution of wealth

Transfer payment

Government revenue:

Taxation

Deficit spending

Government budget

Government budget deficit

Government debt

Non-tax revenueCredit is the trust which allows one party to provide resources to another party where that second party does not reimburse the first party immediately (thereby generating a debt), but instead arranges either to repay or return those resources (or other materials of equal value) at a later date. The resources provided may be financial (e.g. granting a loan), or they may consist of goods or services (e.g. consumer credit). Credit encompasses any form of deferred payment.[1] Credit is extended by a creditor, also known as a lender, to a debtor, also known as a borrower.

Credit does not necessarily require money. The credit concept can be applied in barter economies as well, based on the direct exchange of goods and services (Ingham 2004 p.12-19). However, in modern societies credit is usually denominated by a unit of account. Unlike money, credit itself cannot act as a unit of account.

Movements of financial capital are normally dependent on either credit or equity transfers. Credit is in turn dependent on the reputation or creditworthiness of the entity which takes responsibility for the funds. Credit is also traded in financial markets. The purest form is the credit default swap market, which is essentially a traded market in credit insurance. A credit default swap represents the price at which two parties exchange this risk – the protection "seller" takes the risk of default of the credit in return for a payment, commonly denoted in basis points (one basis point is 1/100 of a percent) of the notional amount to be referenced, while the protection "buyer" pays this premium and in the case of default of the underlying (a loan, bond or other receivable), delivers this receivable to the protection seller and receives from the seller the par amount (that is, is made whole).

Contents

Trade credit

The word credit is used in commercial trade in the term "trade credit" to refer to the approval for delayed payments for purchased goods. Credit is sometimes not granted to a person who has financial instability or difficulty. Companies frequently offer credit to their customers as part of the terms of a purchase agreement. Organizations that offer credit to their customers frequently employ a credit manager.

Consumer credit

Consumer debt can be defined as ‘money, goods or services provided to an individual in lieu of payment.’ Common forms of consumer credit include credit cards, store cards, motor (auto) finance, personal loans (installment loans), consumer lines of credit, retail loans (retail installment loans) and mortgages. This is a broad definition of consumer credit and corresponds with the Bank of England's definition of "Lending to individuals". Given the size and nature of the mortgage market, many observers classify mortgage lending as a separate category of personal borrowing, and consequently residential mortgages are excluded from some definitions of consumer credit - such as the one adopted by the Federal Reserve in the US.

The cost of credit is the additional amount, over and above the amount borrowed, that the borrower has to pay. It includes interest, arrangement fees and any other charges. Some costs are mandatory, required by the lender as an integral part of the credit agreement. Other costs, such as those for credit insurance, may be optional. The borrower chooses whether or not they are included as part of the agreement.

Interest and other charges are presented in a variety of different ways, but under many legislative regimes lenders are required to quote all mandatory charges in the form of an annual percentage rate (APR). The goal of the APR calculation is to promote ‘truth in lending’, to give potential borrowers a clear measure of the true cost of borrowing and to allow a comparison to be made between competing products. The APR is derived from the pattern of advances and repayments made during the agreement. Optional charges are not included in the APR calculation. So if there is a tick box on an application form asking if the consumer would like to take out payment insurance, then insurance costs will not be included in the APR calculation (Finlay 2009).

See also

- Commercial credit reporting

- Credit bureau

- Credit history

- Credit risk

- Credit score

- Debt

- Default (finance)

- Financial literacy

- Installment credit

- Line of credit

- Payday loan

- Person-to-person lending

- Predatory lending

- Revolving credit

- Risk-return spectrum

- Settlement (finance)

- Sub prime lending

- Social Credit

References

- ^ Sullivan, Arthur; Steven M. Sheffrin (2003). Economics: Principles in action. Upper Saddle River, New Jersey 07458: Pearson Prentice Hall. pp. 512. ISBN 0-13-063085-3. http://www.pearsonschool.com/index.cfm?locator=PSZ3R9&PMDbSiteId=2781&PMDbSolutionId=6724&PMDbCategoryId=&PMDbProgramId=12881&level=4.

- Finlay, S. (2009). Consumer Credit Fundamentals. Second Edition. Palgrave Macmillan.

- Ingham, G. (2004). The Nature of Money. Polity Press.

External links

Quotations related to Credit at Wikiquote

Quotations related to Credit at WikiquoteDebt Debt instruments Managing debt Bankruptcy · Consolidation · Debt management plan · Debt relief · Debt restructuring · Debt-snowball method · DIP financingDebt collection and evasion Bad debt · Charge-off · Collection agency · Debt bondage · Debt compliance · Debtors' prison · Garnishment · Phantom debt · Strategic default · Tax refund interceptionDebt markets Consumer debt · Corporate debt · Deposit account · Debt buyer · Fixed income · Government debt · Money market · Municipal debt · Securitization · Venture debtDebt in economics Default · Insolvency · Interest · Interest rate

Wikimedia Foundation. 2010.