- Economic growth

-

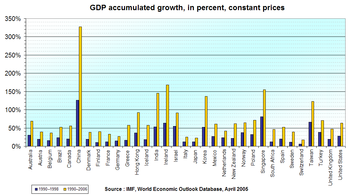

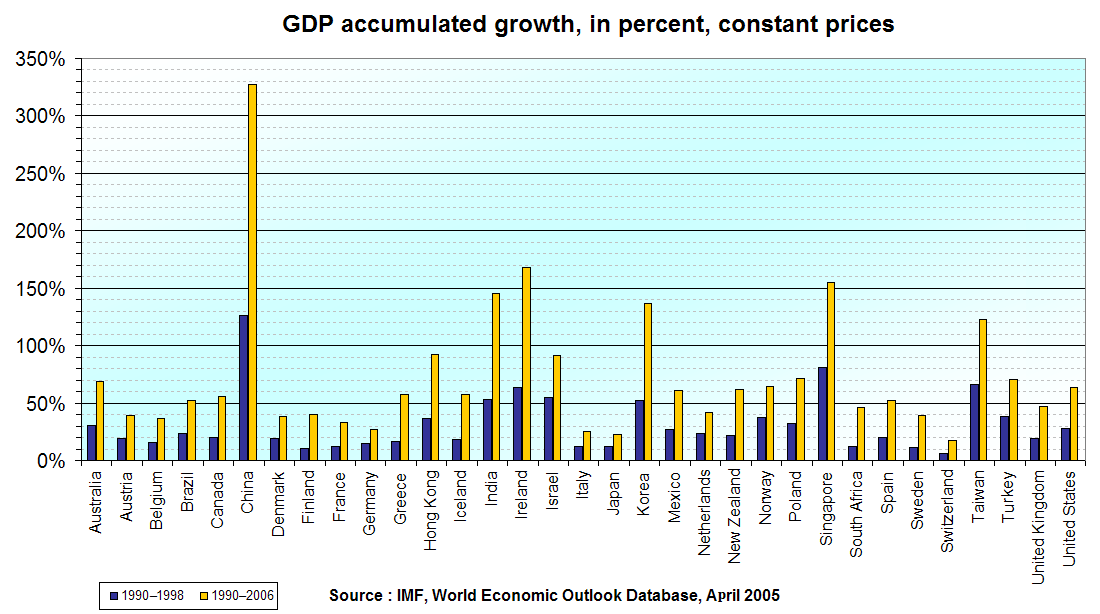

GDP real growth rates, 1990–1998 and 1990–2006, in selected countries.

GDP real growth rates, 1990–1998 and 1990–2006, in selected countries.

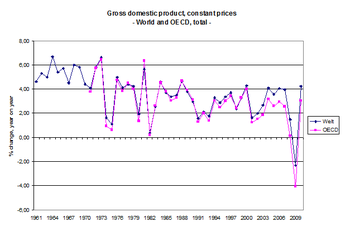

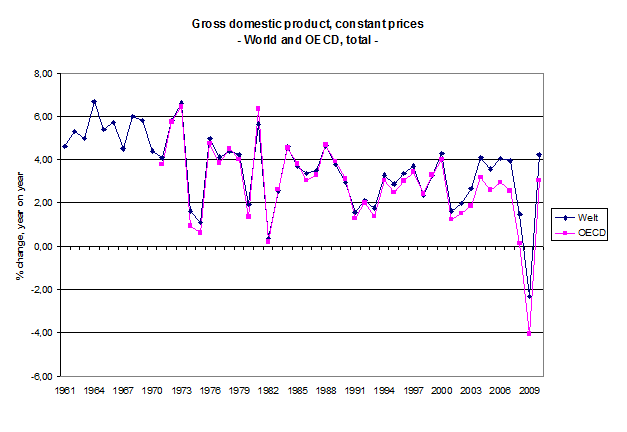

Rate of change of Gross domestic product, world and OECD, since 1961

Rate of change of Gross domestic product, world and OECD, since 1961 Economic growth caused the production-possibility frontier to shift outward.

Economic growth caused the production-possibility frontier to shift outward.In economics, economic growth is defined as the increasing capacity of the economy to satisfy the wants of the members of society. Economic growth is enabled by increases in productivity, which lowers the inputs (labor, capital, material, energy, etc.) for a given amount of output.[1] Lowered costs increase demand for goods and services. Economic growth is also the result of population growth and of the introduction of new products and services.

Economic growth versus the business cycle

Economists distinguish between short-run economic changes in production and long-run economic growth. Short-run variation in economic growth is termed the business cycle. Briefly, the business cycle is made up of booms and busts in production that occur over a period or months or years. The most recent example of a business cycle was the global boom starting in approximately 2002 that ended with the bust of 2008–9. As discussed in the article on the business cycle, economists attribute the ups and downs in the business cycle to a number of causes including: overproduction of goods followed by large inventories that can't be readily sold, overexpansion of credit resulting in piling up of debt that inhibits purchasing; speculative bubbles, and shocks—like wars, political upheavals, and so on.

In contrast, the topic of economic growth is concerned with the long-run trend in production due to basic causes such as industrialization. The business cycle moves up and down, creating fluctuations in the long-run trend in economic growth.

Economic growth per capita

Often, the concern about economic growth focuses on the desire to improve a country's standard of living—the level of goods and services that, on average, individuals purchase or otherwise gain access to. It should be noted that if population has grown along with economic production, increases in GDP do not necessarily result in an improvement in the standard of living. When the focus is on standard of living, economic growth is expressed on a per capita basis.

Economic growth per capita is primarily driven by improvements in productivity, also called economic efficiency. Increased productivity means producing more goods and services with the same inputs of labour, capital, energy, and/or materials. For example, labour and land productivity in agriculture were increased during the Green Revolution. The Green Revolution of the 1940s to 1970s introduced new grain hybrids, which increased yields around the world.

However, there is not necessarily a long term one-to-one relationship between improvements in productivity and improvements in average standard of living.[2] Among other factors that might prevent a long-term improvement in standard of living despite economic growth is the potential for population growth matching or outstripping productivity improvements. When increased food supplies spur population growth rather an improvement in the standard of living, people are said to be caught in the "Malthusian trap," named for Thomas Robert Malthus, the first observer to detail out this dilemma. There is considerable controversy, for example, as to whether the Green Revolution resulted in long-term improvements in the standard of living as it was accompanied by rapid population growth creating population sizes that may be unsustainable.[3]

Economic growth can also be of interest without reference to per capita changes in standard of living. An example of this is the economic growth in England during the Industrial Revolution. Certainly, per capita increases in productivity occurred due to the replacement of hand labour by machines. However, economic growth during this period was in large part so dramatic because England's population simultaneously increased very rapidly (1700 A.D. – 1860 A.D.). The two factors together, more production per worker combined with many more workers, resulted in a sixfold increase in production between 1700 and 1860. Population growth alone accounted for most of this increase.[4]

Measuring economic growth

Economic growth is measured as a percentage change in the Gross Domestic Product (GDP) or Gross National Product (GNP). These two measures, which are calculated slightly differently, total the amounts paid for the goods and services that a country produced. As an example of measuring economic growth, a country which creates $9,000,000,000 in goods and services in 2010 and then creates $9,090,000,000 in 2011, has a nominal economic growth rate of 1% for 2011.

In order to compare per capita economic growth among countries, the total sales of the countries to be compared may be quoted in a single currency. This requires converting the value of currencies of various countries into a selected currency, for example U.S. dollars. One way to do this conversion is to rely on exchange rates among the currencies, for example how many Mexican pesos buy a single U.S. dollar? Another approach is to use the purchasing power parity method. This method is based on how much consumers must pay for the same "basket of goods" in each country.

Inflation or deflation can make it difficult to measure economic growth. If GDP, for example, goes up in a country by 1% in a year, was this due solely to rising prices (inflation) or because more goods and services were produced and saved? To express real growth rather than changes in prices for the same goods, statistics on economic growth are often adjusted for inflation or deflation.

For example, a table may show changes in GDP in the period 1990 to 2000, as expressed in 1990 U.S. dollars. This means that the single currency being used is the U.S. dollar with the purchasing power it had in the U.S. in 1990. The table might mention that the figures are "inflation-adjusted" or real. If no adjustment were made for inflation, the table might make no mention of inflation-adjustment or might mention that the prices are nominal.

The power of annual growth

Over long periods of time, even small rates of growth, like a 2% annual increase, will have large effects. For example, the United Kingdom experienced a 1.97% average annual increase in inflation-adjusted GDP between 1830 and 2008.[5] In 1830, the GDP was 41,373 million pounds. It grew to 1,330,088 million pounds by 2008. (Figures are adjusted for inflation and stated in 2005 values for the pound.) A growth rate which averaged 1.97% over 178 years resulted in a 32-fold increase in GDP by 2008.

The large impact of a relatively small growth rate over a long period of time is due to the power of compounding (also see exponential growth). A growth rate of 2.5% per annum leads to a doubling of GDP within 29 years, whilst a growth rate of 8% per annum (an average exceeded by China between 2000 and 2010) leads to a doubling of GDP within 10 years. Thus, a small difference in economic growth rates between countries can result in very different standards of living for their populations if this small difference continues for many years.

Historical growth

During colonial times, what ultimately mattered for economic growth were the institutions and systems of government imported through colonization. There is a clear reversal of fortune between the poor and wealthy countries, which is evident when comparing the method of colonialism in a region. Geography and endowments of natural resources are not the sole determinants of GDP. In fact, those that were blessed with good factor endowments experienced colonial extraction which only provided limited rapid growth; whereas, countries that were less fortunate in their original endowments experienced European settlement, relative equality, and demand for rule of law. These initially poor colonies end up developing an open franchise, equality, and broad public education, which helps them experience greater economic growth than the colonies that had exploited their economies of scale.

Since the Industrial Revolution, a major factor of productivity was the substitution of energy for human and animal labor and water and wind power, and since that replacement, the great expansion of total power, which was driven by continuous improvements in energy conversion efficiency.[6] Other major historical sources of productivity were mechanization, transportation infrastructures (canals, railroads, and highways),[7] new materials (steel) and power, which includes steam and internal combustion engines and electricity. Other productivity improvements included mechanized agriculture and scientific agriculture including chemical fertilizers and livestock and poultry management, and the Green Revolution. Interchangeable parts made with machine tools powered by electric motors evolved into mass production, which is universally used today.

Great sources of productivity improvement in the late 19th century were the railroads, steam ships, horse-pulled reapers and combine harvesters, and steam-powered factories. The invention of processes for making cheap steel were important for many forms of mechanization and transportation. By the late 19th century, power and machinery were creating overproduction, which eventually caused a reduction of the hourly work week. Prices fell because less labor, materials, and energy were required to produce and transport goods; however, workers real pay rose, allowing workers to improve their diet and buy consumer goods and better housing.[8]

Mass production of the 1920s created overproduction, which was arguably one of several causes of the Great Depression of the 1930s.[9] Following the Great Depression, economic growth resumed, aided in part by demand for entirely new goods and services, such as household electricity, telephones, radio, television, automobiles, and household appliances, air conditioning, and commercial aviation (after 1950), creating enough new demand to stabilize the work week.[10] Building of highway infrastructures also contributed to post World War II growth, as did capital investments in manufacturing and chemical industries. The post World War II economy also benefited from the discovery of vast amounts of oil around the world, particularly in the Middle East.

Economic growth in Western nations slowed after 1973, but growth in Asia has been strong since then, starting with Japan and spreading to Korea, China, the Indian subcontinent and other parts of Asia. The Japanese economy has been growing very slowly since about 1990.

Origins of the concept

In 1377, the Arabian economic thinker Ibn Khaldun provided one of the earliest descriptions of economic growth in his Muqaddimah (known as Prolegomena in the Western world):

"When civilization [population] increases, the available labor again increases. In turn, luxury again increases in correspondence with the increasing profit, and the customs and needs of luxury increase. Crafts are created to obtain luxury products. The value realized from them increases, and, as a result, profits are again multiplied in the town. Production there is thriving even more than before. And so it goes with the second and third increase. All the additional labor serves luxury and wealth, in contrast to the original labor that served the necessity of life."[11]In the early modern period, some people in Western European nations developed the idea that economies could "grow", that is, produce a greater economic surplus, which could be expended on something other than mere subsistence. This surplus could then be used for consumption, warfare, or civic and religious projects. The previous view was that only increasing either population or tax rates could generate more surplus money for the Crown or country.

Later, it was theorized that economic growth also corresponds to a process of continual rapid replacement and reorganization of human activities facilitated by investment motivated to maximize returns. This exponential evolution of our self-organized life-support and cultural systems is remarkably creative and flexible, but highly unpredictable in many ways. As there are difficulties in modelling complex self-organizing systems, various efforts to model the long term evolution of economies have produced mixed results.

During much of the "Mercantilist" period, growth was seen as involving an increase in the total amount of specie, that is circulating medium such as silver and gold, under the control of the state. This "Bullionist" theory led to policies to force trade through a particular state, the acquisition of colonies to supply cheaper raw materials, which could then be manufactured and sold.

Later, such trade policies were justified instead simply in terms of promoting domestic trade and industry. The post-Bullionist insight that it was the increasing capability of manufacturing, which led to policies in the 18th century to encourage manufacturing in itself, and the formula of importing raw materials and exporting finished goods. Under this system, high tariffs were erected to allow manufacturers to establish "factories". Local markets would then pay the fixed costs of capital growth, and then allow them to export abroad, undercutting the prices of manufactured goods.

Under this theory of growth, to foster growth was to grant monopolies, which would give an incentive for an individual to exploit a market or resource, confident that he would make all of the profits when all other extra-national competitors were driven out of business. The "Dutch East India company" and the "British East India company" were examples of such state-granted trade monopolies.[12]

In this period, the view was that growth was gained through "advantageous" trade in which specie would flow into the country, but to trade with other nations on equal terms was disadvantageous. It should be stressed that Mercantilism was not simply a matter of restricting trade. Within a country, it often meant breaking down trade barriers, building new roads, and abolishing local toll booths, all of which expanded markets. This corresponded to the centralization of power in the hands of the Crown (or "Absolutism"). This process helped produce the modern nation-state in Western Europe.

Internationally, Mercantilism led to a contradiction: growth was gained through trade, but to trade with other nations on equal terms was disadvantageous.

Various theories on economic growth

Classical growth theory

The modern conception of economic growth began with the critique of Mercantilism, especially by the physiocrats and with the Scottish Enlightenment thinkers such as David Hume and Adam Smith, and the foundation of the discipline of modern political economy. The theory of the physiocrats was that productive capacity, itself, allowed for growth, and the improving and increasing capital to allow that capacity was "the wealth of nations". Whereas they stressed the importance of agriculture and saw urban industry as "sterile", Smith extended the notion that manufacturing was central to the entire economy.[13]

David Ricardo argued that trade was a benefit to a country, because if one could buy a good more cheaply from abroad, it meant that there was more profitable work to be done here. This theory of "comparative advantage" would be the central basis for arguments in favor of free trade as an essential component of growth.[14]

The neoclassical growth model

The notion of growth as increased stocks of capital goods (means of production) was codified as the Solow-Swan Growth Model, which involved a series of equations which showed the relationship between labor-time, capital goods, output, and investment. According to this view, the role of technological change became crucial, even more important than the accumulation of capital. This model, developed by Robert Solow[15] and Trevor Swan[16] in the 1950s, was the first attempt to model long-run growth analytically. This model assumes that countries use their resources efficiently and that there are diminishing returns to capital and labor increases. From these two premises, the neoclassical model makes three important predictions. First, increasing capital relative to labor creates economic growth, since people can be more productive given more capital. Second, poor countries with less capital per person will grow faster because each investment in capital will produce a higher return than rich countries with ample capital. Third, because of diminishing returns to capital, economies will eventually reach a point at which any increase in capital will no longer create economic growth. This point is called a "steady state".

The model also notes that countries can overcome this steady state and continue growing by inventing new technology. In the long run, output per capital depends on the rate of saving, but the rate of output growth should be equal for any saving rate. In this model, the process by which countries continue growing despite the diminishing returns is "exogenous" and represents the creation of new technology that allows production with fewer resources. Technology improves, the steady state level of capital increases, and the country invests and grows. The data does not support some of this model's predictions, in particular, that all countries grow at the same rate in the long run, or that poorer countries should grow faster until they reach their steady state. Also, the data suggests the world has slowly increased its rate of growth.

However, modern economic research shows that the baseline version of the neoclassical model of economic growth is not supported by the evidence.

Endogenous growth theory

Main article: Endogenous growth theoryGrowth theory advanced again with the theories of economist Paul Romer and Robert Lucas, Jr. in the late 1980s and early 1990s.

Unsatisfied with Solow's explanation, economists worked to "endogenize" technology in the 1980s. They developed the endogenous growth theory that includes a mathematical explanation of technological advancement.[17][18] This model also incorporated a new concept of human capital, the skills and knowledge that make workers productive. Unlike physical capital, human capital has increasing rates of return. Therefore, overall there are constant returns to capital, and economies never reach a steady state. Growth does not slow as capital accumulates, but the rate of growth depends on the types of capital a country invests in. Research done in this area has focused on what increases human capital (e.g. education) or technological change (e.g. innovation).[19]

John Joseph Puthenkalam's research aims at the process of economic growth theories that lead to economic development. After analyzing the existing capitalistic growth-development theoretical apparatus, he introduces the new model which integrates the variables of freedom, democracy and human rights into the existing models and argue that any future economic growth-development of any nation depends on this emerging model as we witness the third wave of unfolding demand for democracy in the Middle East. He develops the knowledge sector in growth theories with two new concepts of 'mirco knowledge' and 'macro knowledge'. Micro knowledge is what an individual learns from school or from various existing knowledge and macro knowledge is the core philosophical thinking of a nation that all individuals inherently receive. How to combine both these knowledge would determine further growth that leads to economic development of developing nations. For further reading, please refer to "Integrating Freedom, Democracy and Human Rights into Theories of Economic Growth" (1998,2000&2009).

Theory of cognitive wealth (cognitive capitalism)

The theory of "Cognitive capitalism" asserts that cognitive ability is the crucial factor which creates wealth in modern economies, and that the geographical factors which have been necessary in ancient societies are no longer so important. The average cognitive ability of a nation determines its wealth, each IQ point increase boosting a country's average GDP by $229. Of even more significance, the IQ of the brightest 5% of people in the nation (the cognitive elite) boosts GDP by $468 per IQ point. The cognitive elite support general efficiency, technological innovation, efficient administration, independent institutions, and economic freedom. Via these factors intelligence and knowledge stimulate growth leading to national wealth, which in turn may boost cognitive ability in a virtuous circle. The theory was developed by the two psychologists Heiner Rindermann and James Thompson.[20] The theory is related to human capital theory.

Unified growth theory

Unified growth theory was developed by Oded Galor and his co-authors to address the inability of endogenous growth theory to explain key empirical regularities in the growth processes of individual economies and the world economy as a whole. Endogenous growth theory was satisfied with accounting for empirical regularities in the growth process of developed economies over the last hundred years. As a consequence, it was not able to explain the qualitatively different empirical regularities that characterized the growth process over longer time horizons in both developed and less developed economies. Unified growth theories are endogenous growth theories that are consistent with the entire process of development, and in particular the transition from the epoch of Malthusian stagnation that had characterized most of the process of development to the contemporary era of sustained economic growth.[21]

The big push

Theories of economic growth, the mechanisms that let it take place and its main determinants are abound. One popular theory in the 1940s, for example, was that of the "Big Push" which suggested that countries needed to jump from one stage of development to another through a virtuous cycle, in which large investments in infrastructure and education coupled with private investments would move the economy to a more productive stage, breaking free from economic paradigms appropriate to a lower productivity stage.[22]

Creative destruction and economic growth

Main article: Creative destructionMany economists view entrepreneurship as having a major influence on a society's rate of technological progress and thus economic growth.[23] Joseph Schumpeter was a key figure in understanding the influence of entrepreneurs on technological progress.[23] In Schumpeter's Capitalism, Socialism and Democracy, published in 1942, an entrepreneur is a person who is willing and able to convert a new idea or invention into a successful innovation. Entrepreneurship forces "creative destruction" across markets and industries, simultaneously creating new products and business models. In this way, creative destruction is largely responsible for the dynamism of industries and long-run economic growth. Former Federal Reserve chairman Alan Greenspan has described the influence of creative destruction on economic growth as follows: "Capitalism expands wealth primarily through creative destruction—the process by which the cash flow from obsolescent, low-return capital is invested in high-return, cutting-edge technologies."[24]

Transformational growth

Transformational growth describes the changes in both institutions and the working of markets, as growth and innovation take place. Edward J. Nell (The New School, NY) is the originator of the General Theory of Transformational Growth, which traces the pattern of capitalist development through a succession of stages, in each of which markets adjust differently, and in doing so, give rise to market pressures leading to innovations, which move the system to the next stage. In each stage, the working of markets will be governed in part by the structure of costs and the pattern of growth in demand, both of which depend on technology and innovation. The approach draws on the empirical work of Simon Kuznets, and makes use of Nicholas Kaldor’s notion of stylized facts; it also draws on the work of W. Arthur Lewis and Gunnar Myrdal in regard to stages of development. It is, however, consistent only in part with Robert Solow’s neo-Classical approach; as in that construction the substitution of capital for labor is crucial. However, transformational growth rejects the idea of a steady state and presents a model of multiple sectors regularly changing in size and importance. On the other hand, Douglass North’s emphasis on institutions is echoed here.[25]

Nell (1988, p. xiii) argued that

We do not live in a Free Market system. This is not because such a system has become overburdened, or because labor unions and monopolies have usurped its functions, or because the market has become tangled in regulations and red tape. It is because the fundamental institutions of economic society have changed: crafts have become industries, firms have become corporations, and markets are administratered. These are not 'imperfections' or examples of 'market failure'; as the basic institutions changed, the market itself came to work differently. An economy of family firms and family farms might once have functioned like an Idealized Free Market. But the modern system of corporate industry does not. It behaves differently in regard both to output and employment and to pricing: output and employment are adjusted to current sales, but prices are planned with an eye to the financing of investment, so are governed by long-term considerations, and tend to be unresponsive to shot term changes. So, the automatic and anonymous rule of supply and demand in the market came to be replaced by a form of private administration. Moreover, where the earlier economic system had grown slowly, and by accretion, so that it functioned according to static principles, the corporate industry that replaced it depended on an internal dynamic. It either grew, or collapsed. But this Growth was not a simple expansion- it was developmental. The economic system was transformed. And then this Transformational Growth faltered, as it did in the 1930s, in the 1980s and again recently, the system malfunctioned in a wide variety of ways. Finally, the transformation from a craft economy to modern industry is world-wide. It cannot be understood and policy cannot be planned. This is especially true with the development of transnational corporations and international capital.

The full development of the theory of transformational growth came in the 90s, and was published Edward J. Nell as The General Theory of Transformational Growth (Cambridge University Press, 1998),[26] starting from a critique of equilibrium –supporting creative destruction instead – working through methodological and philosophical questions about the role of contracts and obligations in understanding the persistence of institutional structures, to the circulation of money, understanding productivity and the structure of production – especially the relationship between the wage bill of capital goods and the capital requirements in consumer goods – then going on to dynamics, and from there to aggregate demand and the business cycle.[27]

Nell has explored the move from ‘Replicative growth,’ governed by the price mechanism, where growth proceeds by new firms replicating old, to ‘Innovative growth’, regulated by the multiplier-accelerator, where firms invest in expanding and improving their own facilities, and the role of prices is chiefly found in long-term capital planning. Replicative growth describes the result of investment in the same technology and same pattern of firms and firm sizes, where the new firms produce the same list of goods and services, with the same composition of labor and means of production. The economy simply replicates itself, following the incentives offered by the price system. In the short run a Marshallian production function is assumed – applying additional labor to given plant and equipment yields diminishing returns, a more or less plausible idea in craft and agricultural conditions. The long-run is thus characterized by constant returns, but in the short run, adjustments of employment with given equipment will show diminishing returns. This is essentially the neo-Classical picture of the 19th Century economy.

By contrast, the standard neo-Classical growth model, based on Solow, 1956, (and also Swan, 1956) projects diminishing marginal returns into the long run – without explanation – assuming that each point on the function represents a different fully adjusted capital structure. It also fails to provide a role for prices in adjusting output to changes in demand. Indeed, aggregate demand plays no role at all; full employment, that is, full utilization of capacity, is explicitly assumed, rather than demonstrated, and prices are assumed to be constant. Saving governs investment. Banishing both prices and demand leaves the model hopelessly one-sided; it deals only with the growth-consumption- relative size aspect of the economy, ignoring the wages-prices-profits complex. But Solow assumed diminishing returns and that the marginal productivity conditions will be met – in the absence of price flexibility! If marginal products diminish, marginal costs rise, and in competitive markets prices must change as output changes. And if prices change there should be effects on demand. There is a problem. To correct it we will study a simple system of ‘growth as replication’, based on a Keynesian-Marshallian price adjustment mechanism, operating in the short run. Replication means that, for theoretical purposes, this kind of growth can be measured in units of the optimal sized firm, which, if the technology is what we call ‘Marshallian’, will be the size indicated by the minimum of a U-shaped average cost curve. (Austin Robinson, 1931) Moreover, the economy replicates itself following the incentives generated by a price mechanism that puts the burden of adjustment to demand fluctuations on profits. In Hicks’ terms, this is a ‘flexprice’ system. Such flexibility, in turn, creates pressures that lead to Transformational Growth, changing the system to one of Intensive Growth.

Replicative growth displays what might be called the ‘Victorian pattern’ of growth, in which shares are constant, as is the rate of profit, because the proportional change in the capital-output ratio just matches that in labor productivity, which, in turn, just equals the proportional change in the real wage. The move to innovative growth comes about as firms try to make their costs more flexible, to lighten the burden of adjustment. They invest in themselves. In the process they engage in innovation, reap economies of scale, and basically work their way beyond Craft technology to newly invented systems of Mass Production, and the Victorian pattern no longer holds. In the new system the assumption of generalized diminishing returns makes no sense; instead returns to and expanded level of employment appear to be constant over a broad range. In these circumstances there is no price mechanism; Kaldor’s effort to introduce price flexibility and adjustment at full employment appears to be misguided.

Transformational growth and business cycles

Transformational growth had a major impact on government and government policy, bringing about a countercyclical federal budget, and important changes in the agenda of government. To study these policy changes called for further development of the simple theory of effective demand. Changes in the flexibility of prices required study of pricing, and competition among corporations. Profits functioned as business saving, becoming more important in the US than household saving, and had to be understood in relation to prices (markups) and investment, to which they were closely linked, both in theory and in fact.

Nell published in 1998 (Transformational Growth and the Business Cycle, London: Routledge, 1998). The book contained the work of a study group of New School students, testing the empirical validity of the approach, by examining the time series of prices, wages, employment, output, and productivity in six countries. About the same time Nell wrote a book in 1996 (Making Sense of a Changing Economy, London: Routledge, 1996) and laying out the ‘paradoxes of individualism’, and providing both a critique of the social philosophy of individualism and suggestions for a more satisfactory approach.

Useful work growth theory

Main article: Useful work growth theoryThe useful work growth theory, also called the Ayres-Warr model, states that physical and chemical work performed by energy, or more correctly exergy, has historically been the most important driver of economic growth.[6] [28] Key support for this theory is a mathematical model showing that the efficiency of electrical generation is a good proxy for the Solow residual, or technological progress, that is, the portion of economic growth that is not attributable to capital, labor, or materials.[29][30]

Useful work theory provides a greatly improved explanation of economic growth over previous production functions. The theory relates the slowing of economic growth to energy conversion efficiencies approaching thermodynamic limits, and cautions that declining resource quality could bring an end to economic growth in a few decades.

The useful work theory is part of a body of economic research and analysis sponsored by the International Institute for Applied Systems Analysis (IIASA) and INSEAD and is cited by the International Energy Agency.[31]

Inequality and economic growth

The effect of inequality on economic growth

The classical theory

Inequality has a positive effect on economic development. The marginal propensity to save increases with wealth and inequality increases savings, capital accumulation, and economic growth.[32]

The neoclassical theory

The neoclassical theory ignores the relevance of income distribution for macroeconomic analysis. It interprets the observed relationship between inequality and economic growth as a reflection of the growth process on the distribution of income.

The modern theory

The modern theory suggests that income distribution, plays an important role in the determination of aggregate economic activity and economic growth.

The credit market imperfection approach, developed by Galor and Zeira (1993), demonstrates that inequality in the presence of credit market imperfections has a long lasting detrimental effect on human capital formation and economic development.[33]

The political economy approach, developed by Alesina and Rodrik 1994) and Persson and Tabellini (1994), suggests that inequality is harmful for economic development because inequality generates a pressure to adopt redistributive policies that have an adverse effect on investment and economic growth.[34]

Evidence

Perotti (1996) examines of the channels through which inequality may affect economic growth. He shows that in accordance with the credit market imperfection approach, inequality is associated with lower level of human capital formation and higher level of fertility, while lower level of human capital is associated with lower growth and lower levels of economic growth. In contrast, his examination of the political economy channel refutes the political economy mechanism. He demonstrates that inequality is associated with lower levels of taxation, while lower levels of taxation, contrary to the theories, are associated with lower level of economic growth[35]

The effect of growth on inequality

Economist Xavier Sala-i-Martin argues that global income inequality is diminishing,[36] and the World Bank argues that the rapid reduction in global poverty is in large part due to economic growth.[37] The decline in poverty has been the slowest where growth performance has been the worst (i.e. in Africa).[38]

Finance and economic growth

Substantial academic literature and government strategies support the finance-led growth hypothesis, based on an observation first made almost a century ago by Joseph Schumpeter that financial markets significantly boost real economic growth and development. Schumpeter asserted that finance had a positive impact on economic growth as a result of its effects on productivity growth and technological change.[39] As early as 1989 the World Bank also endorsed the view that financial deepening matters for economic growth "by improving the productivity of investment".[40] A number of case studies on Asia and Southern African countries show the positive nexus between development of financial intermediation and economic growth.[citation needed]

Institutions and growth

According to Acemoğlu, Johnson and Robinson, the positive correlation between high income and cold climate is a by-product of history. Europeans adopted very different colonization policies in different colonies, with different associated institutions. In places where these colonizers faced high mortality rates (e.g., due to the presence of tropical diseases), they could not settle permanently, and they were thus more likely to establish extractive institutions, which persisted after independence; in places where they could settle permanently (e.g. those with temperate climates), they established institutions with this objective in mind and modeled them after those in their European homelands. In these 'neo-Europes' better institutions in turn produced better development outcomes. Thus, although other economists focus on the identity or type of legal system of the colonizers to explain institutions, these authors look at the environmental conditions in the colonies to explain institutions. For instance, former colonies have inherited corrupt governments and geo-political boundaries (set by the colonizers) that are not properly placed regarding the geographical locations of different ethnic groups, creating internal disputes and conflicts which in turn hinder development. In another example, societies that emerged in colonies without solid native populations established better property rights and incentives for long-term investment than those where native populations were large.[41]

Human capital and growth

One ubiquitous element of both theoretical and empirical analyses of economic growth is the role of human capital. The skills of the population enter into both neoclassical and endogenous growth models.[42] The most commonly used measure of human capital is the level of school attainment in a country, building upon the data development of Robert Barro and Jong-Wha Lee.[43] This measure of human capital, however, requires the strong assumption that what is learned in a year of schooling is the same across all countries. It also presumes that human capital is only developed in formal schooling, contrary to the extensive evidence that families, neighborhoods, peers, and health also contribute to the development of human capital. In order to measure human capital more accurately, Eric Hanushek and Dennis Kimko introduced measures of mathematics and science skills from international assessments into growth analysis.[44] They found that quality of human capital was very significantly related to economic growth. This approach has been extended by a variety of authors, and the evidence indicates that economic growth is very closely related to the cognitive skills of the population.[45]

Quality of life

Happiness has been shown to increase with a higher GDP per capita, at least up to a level of $15,000 per person.[46]

Economic growth has the indirect potential to alleviate poverty, as a result of a simultaneous increase in employment opportunities and increase labour productivity.[47] A study by researchers at the Overseas Development Institute (ODI) of 24 countries that experienced growth found that in 18 cases, poverty was alleviated.[47] However, employment is no guarantee of escaping poverty, the International Labour Organisation (ILO) estimates that as many as 40% of workers as poor, not earning enough to keep their families above the $2 a day poverty line.[47] For instance, in India most of the chronically poor are wage earners in formal employment, because their jobs are insecure and low paid and offer no chance to accumulate wealth to avoid risks.[47] This appears to be the result of a negative relationship between employment creation and increased productivity, when a simultaneous positive increase is required to reduced poverty. According to the UNRISD, increasing labour productivity appears to have a negative impact on job creation: in the 1960s, a 1% increase in output per worker was associated with a reduction in employment growth of 0.07%, by the first decade of this century the same productivity increase implies reduced employment growth by 0.54%.[47]

Increases in employment without increases in productivity leads to a rise in the number of "working poor", which is why some experts are now promoting the creation of "quality" and not "quantity" in labour market policies.[47] This approach does highlight how higher productivity has helped reduce poverty in East Asia, but the negative impact is beginning to show.[47] In Viet Nam, for example, employment growth has slowed while productivity growth has continued.[47] Furthermore, productivity increases do not always lead to increased wages, as can be seen in the US, where the gap between productivity and wages has been rising since the 1980s.[47] The ODI study showed that other sectors were just as important in reducing unemployment, as manufacturing.[47] The services sector is most effective at translating productivity growth into employment growth. Agriculture provides a safety net for jobs and economic buffer when other sectors are struggling.[47] This study suggests a more nuanced understanding of economic growth and quality of life and poverty alleviation.

Negative effects of economic growth

A number of critical arguments have been raised against economic growth.[48]

It may be that economic growth improves the quality of life up to a point, after which it doesn't improve the quality of life, but rather obstructs sustainable living.[49] Historically, sustained growth has reached its limits (and turned to catastrophic decline) when perturbations to the environmental system last long enough to destabilise the bases of a culture.[49]

Consumerism

Growth may lead to consumerism by encouraging the creation of what some regard as artificial needs: Industries cause consumers to develop new taste, and preferences for growth to occur. Consequently, "wants are created, and consumers have become the servants, instead of the masters, of the economy."[48]

Resource depletion

Many earlier predictions of resource depletion, such as Thomas Malthus' 1798 predictions about approaching famines in Europe, The Population Bomb (1968),[50][51][52] Limits to Growth (1972),[50][51][52] and the Simon–Ehrlich wager (1980) [53] did not materialize, nor has diminished production of most resources occurred so far, one reason being that advancements in technology and science have allowed some previously unavailable resources to be produced.[53] In some cases, substitution of more abundant materials, such as plastics for cast metals, lowered growth of usage for some metals. In the case of the limited resource of land, famine was relieved firstly by the revolution in transportation caused by railroads and steam ships, and later by the Green Revolution and chemical fertilizers, especially the Haber process for ammonia synthesis.[54][55]

In the case of minerals, lower grades of mineral resources are being extracted, requiring higher inputs of capital and energy for both extraction and processing.[56] An example is natural gas from shale and other low permeability rock, which can be developed with much higher inputs of energy, capital, and materials than conventional gas in previous decades. Another example is offshore oil and gas, which has exponentially increasing cost as water depth increases.

However, some "Malthusians", such as William R. Catton, Jr., author of the 1980 book "Overshoot," are skeptical of these various advancements in technology which make available previously inaccessible or lower grade resources. The counter-argument is that such advances as well as increases in efficiency merely accelerate the drawing down of finite resources. Catton has referred to the contemporary increases in rates of resource extraction as "stealing ravenously from the future."[57] The apparent and temporary "increase" of resource extraction with the use of new technology leads to the popular perception that resources are infinite or can be substituted without limit, but this perception fails to consider that ultimately, even lower quality resources are finite and become uneconomic to extract when the ore quality is too low. Because of cultural lag, the perception of infinite resources and substitutes may linger on for generations, and may not change, since the inevitable resource bankruptcy is passed on to posterity. Catton has called the faith in technology a form of "cargoism," which takes its meaning from various "Cargo Cults" in Melanesia and Micronesia. Furthermore, Joseph Tainter, anthropologist, historian and author of the book "The Collapse of Complex Societies," has pointed out that each new addition of complexity to technology can only be sustained if there is a good enough return to justify the technology, and that over time, increases in complexity have improved productivity at an ever decreasing rate. As an example, in the early 1900's when much of the world's oil was untapped, it was sufficient to drill a few metres into the ground and install inexpensive rigs to extract oil at rapid rates. At the beginning of the 21st century, in order to achieve the same flowrates or less, oilfields must be drilled much deeper and managed with sophisticated techniques and equipment costing many hundreds of millions of dollars. If such trends continue, there may arrive a time when it becomes uneconomic to increase complexity in order to access lower grade resources with no net improvement in productivity.

Environmental impact

Some critics[who?] argue that a narrow view of economic growth, combined with globalization, is creating a scenario where we could see a systemic collapse of our planet's natural resources.[58] Other critics draw on archaeology to cite examples of cultures they claim have disappeared because they grew beyond the ability of their ecosystems to support them.[59] Concerns about possible negative effects of growth on the environment and society led some to advocate lower levels of growth, from which comes the ideas of uneconomic growth and de-growth, and Green parties which argue that economies are part of a global society and a global ecology and cannot outstrip their natural growth without damaging them.

Canadian scientist, David Suzuki stated in the 1990s that ecologies can only sustain typically about 1.5–3% new growth per year, and thus any requirement for greater returns from agriculture or forestry will necessarily cannibalize the natural capital of soil or forest.[citation needed] Some think this argument can be applied even to more developed economies.[citation needed]

Those more optimistic about the environmental impacts of growth believe that, although localized environmental effects may occur, large scale ecological effects are minor. The argument as stated by commentators Julian Lincoln Simon states that if these global-scale ecological effects exist, human ingenuity will find ways of adapting to them.[60]

Equitable growth

While acknowledging the central role economic growth can potentially play in human development, poverty reduction and the achievement of the Millennium Development Goals, it is becoming widely understood amongst the development community that special efforts must be made to ensure poorer sections of society are able to participate in economic growth.[61] For instance, with low inequality a country with a growth rate of 2% per head and 40% of its population living in poverty, can halve poverty in ten years, but a country with high inequality would take nearly 60 years to achieve the same reduction.[62] In the words of the Secretary General of the United Nations Ban Ki-Moon:

- "While economic growth is necessary, it is not sufficient for progress on reducing poverty."[61]

Researchers at the Overseas Development Institute compares situations such as in Uganda, where during a period of annual growth of 2.5% between 2000 and 2003, the percentage of people living in poverty actually increased by 3.8%.[61] The ODI thus emphasises the need to ensure social protection is extended to allow universal access and that policies are introduced to encourage the private sector to create new jobs as the economy grows (as opposed to jobless growth) and seek to employ people from disadvantaged groups.[61]

Implications of global warming

Up to the present there are close correlations of economic growth with carbon dioxide emissions across nations, although there is also a considerable divergence in carbon intensity (carbon emissions per GDP).[63] The Stern Review notes that the prediction that "under business as usual, global emissions will be sufficient to propel greenhouse gas concentrations to over 550ppm CO2e by 2050 and over 650–700ppm by the end of this century is robust to a wide range of changes in model assumptions". The scientific consensus is that planetary ecosystem functioning without incurring dangerous risks requires stabilization at 450–550 ppm.[64]

As a consequence, growth-oriented environmental economists propose massive government intervention into switching sources of energy production, favouring wind, solar, hydroelectric, and nuclear. This would largely confine use of fossil fuels to either domestic cooking needs (such as for kerosene burners) or where carbon capture and storage technology can be cost-effective and reliable.[65] The Stern Review, published by the United Kingdom Government in 2006, concluded that an investment of 1% of GDP would be sufficient to avoid the worst effects of climate change, and that failure to do so could risk climate-related costs equal to 20% of GDP. Because carbon capture and storage is as yet widely unproven, and its long term effectiveness (such as in containing carbon dioxide 'leaks') unknown, and because of current costs of alternative fuels, these policy responses largely rest on faith of technological change.

On the other hand, Nigel Lawson claimed that people in a hundred years' time would be "seven times as well off as we are today", therefore it is not reasonable to impose sacrifices on the "much poorer present generation".[66]

Prominent growth economists

See also

- Boom and bust

- Capital accumulation

- Demographic economics

- Development economics

- Eco-sufficiency

- Ecological economics

- Economic determinism

- Economic development

- Export-led growth

- FORGE Program

- Growth accounting

- Growth elasticity of poverty

- Human development theory

- Index of Leading Indicators

- Investment

- Investment-specific technological progress

- The Limits to Growth

- List of countries by GDP (real) growth rate

- Malthusian trap

- Measures of national income

- Production-possibility frontier

- Stagflation

- Steady state economy

- Sustainability

- Unified growth theory

- Zero growth

References

- ^ Kendrick, John W. (1961). Productivity Trends in the United States. Princeton University Press for NBER. p. 111.

- ^ Gregory Clark, A Farewell to Alms, a Brief Economic History of the World, Princeton University Press, 2007

- ^ Spitz, Pierre (1987)"The Green Revolution Re-Examined in India in Glass". In Glaeser, Bernhard. The Green Revolution revisited: critique and alternatives. Allen & Unwin. pp. 57–75. ISBN 0-04-630014-7

- ^ Gregory Clark, A Farewell to Alms, a Brief Economic History of the World, Princeton University Press, 2007, pages 245–246 and Figure 12.8.

- ^ Lawrence H. Officer, "What Was the U.K. GDP Then?" MeasuringWorth, 2011. URL:http://www.measuringworth.com/ukgdp/

- ^ a b Ayres, Robert U.; Warr, Benjamin (2004). Accounting for Growth: The Role of Physical Work. http://www.iea.org/work/2004/eewp/Ayres-paper1.pdf

- ^ Grubler, Arnulf (1990). The Rise and Fall of Infrastructures. http://www.iiasa.ac.at/Admin/PUB/Documents/XB-90-704.pdf

- ^ Wells, David A. (1890). Recent Economic Changes and Their Effect on Production and Distribution of Wealth and Well-Being of Society. New York: D. Appleton and Co.. ISBN 0543724743. http://books.google.com/books?id=2V3qF4MWh_wC&printsec=frontcover&dq=RECENT+ECONOMIC+CHANGES+AND+THEIR+EFFECT+ON+DISTRIBUTION+OF+WEALTH+AND+WELL+BEING+OF+SOCIETY+WELLS#v=onepage&q&f=false.

- ^ Beaudreau, Bernard C. (1996). Mass Production, the Stock Market Crash and the Great Depression. New York, Lincoln, Shanghi: Authors Choice Press.

- ^ Moore, Stephen; Simon, Julian (Dec. 15, 1999). The Greatest Century That Ever Was: 25 Miraculous Trends of the last 100 Years, The Cato Institute: Policy Analysis, No. 364. http://www.cato.org/pubs/pas/pa364.pdfDiffusion curves for various innovations start at Fig. 14

- ^ Ibn Khaldun, Muqaddimah, 2:272–73, quoted in Dieter Weiss (1995), "Ibn Khaldun on Economic Transformation", International Journal of Middle East Studies 27 (1), p. 29–37 [30].

- ^ East India Company http://en.wikipedia.org/wiki/East_India_Company

- ^ An Inquiry into the Nature and Causes of the Wealth of Nations http://econlib.org/library/Smith/smWN.html

- ^ The Theory of Comparative Advantage http://internationalecon.com/Trade/Tch40/T40-0.php

- ^ Robert M. Solow (1956), "A Contribution to the Theory of Economic Growth," Quarterly Journal of Economics, 70(1), p p. 65-94.

- ^ Trevor W. Swan (1956). "Economic Growth and Capital Accumulation', Economic Record, 32, pp. 334–61.

- ^ Romer, 1986

- ^ Lucas, 1988

- ^ Elhanah Helpman, The Mystery of Economic Growth, Havard University Press, 2004.

- ^ Rindermann, H. & Thompson, J. (2011). Cognitive capitalism: The effect of cognitive ability on wealth, as mediated through scientific achievement and economic freedom. Psychological Science, 22, 754–763.

- ^ Galor O., 2005, From Stagnation to Growth: Unified Growth Theory. Handbook of Economic Growth, Elsevier

- ^ Paul Rosenstein-Rodan[specify]

- ^ a b "Economic growth." Encyclopædia Britannica. 2008. Encyclopædia Britannica 2006 Ultimate Reference Suite DVD. 14 June 2008.

- ^ Greenspan, Alan (May 3, 2002). "Stock Options and Related Matters". The Federal Reserve Board. http://www.federalreserve.gov/Boarddocs/Speeches/2002/20020503/default.htm. Retrieved June 23, 2009.

- ^ For an account see Karim Errouaki (2009)From Classical Growth Theory to Transformational Growth. UM, New School, NY.

- ^ For a review essay of the book see S. Abu Turab Rizvi (1998) ‘’The General Theory of Transformational Growth,’’ (London: Cambridge University Press, 1998, by Edward J. Nell). Journal of Economic Literature. Vol. 36, No. 4, Dec., 1998. For an account of the Theory of Transformational Growth see Ross Thomson (2004)‘’Transformational Growth and the Universality of Technology’’. In Argyrous, G., Forstater, M and Mongiovi, G. (eds.) (2004) Growth, Distribution, And Effective Demand: Essays in Honor of Edward J. Nell. New York: M.E. Sharpe.

- ^ For an account of the methodology/philosophy which underlies the Theory of Transformational Growth see Karim Errouaki (2008)’’Rethinking the Foundations of Transformational Growth’’. UM, The New School, NY.

- ^ Ayres, Robert U.; Warr, Benjamin (2006). Economic growth, technological progress and energy use in the U.S. over the last century: Identifying common trends and structural change in macroeconomic time series, INSEAD. http://www.helsinki.fi/iehc2006/papers2/Warr.pdf

- ^ Ayres, R. U.; Ayres, L. W.; Warr, B. (2002). Exergy, Power and Work in the U. S. Economy 1900-1998, Insead’s Center For the Management of Environmental Resources, 2002/52/EPS/CMER. http://www.iea.org/work/2004/eewp/Ayres-paper3.pdf

- ^ Ayres, Robert; Warr, Banjamin. The Economic Growth Engine: How Energy and Work Drive Material Prosperity (The International Institute for Applied Systems Analysis). Edward Elgar Publishing; Reprint edition (October 31, 2010). ISBN 1849804354.

- ^ International Energy Agency (2004). World Energy Outlook 2004. http://www.iea.org/textbase/nppdf/free/2004/weo2004.pdf<Chapter 10>

- ^ Kaldor, Nicoals, 1955, Alternative Theories of Distribution,” Review of Economic Studies, 23(2), 83–100.

- ^ Galor, Oded and Joseph Zeira, 1993, "Income Distribution and Macroeconomics," Review of Economic Studies, 60(1), 35–52.

- ^ Alesina, Alberto and Dani Rodrik, 1994. "Distributive Politics and Economic Growth," Quarterly Journal of Economics, 109(2), 65–90; Persson, Torsten and Guido Tabellini, 1994, “Is Inequality Harmful for Growth?” American Economic Review 84(3), 600–621.

- ^ Perotti, Roberto, 1996, “Growth, Income Distribution, and Democracy: What the Data Say” Journal of Economic Growth, 1(2), 149–187.

- ^ Global Inequality Fades as the Global Economy Grows Xavier Sala-i-Martin. 2007 Index of Economic Freedom.

- ^ Poverty, Growth, and Inequality World Bank

- ^ Fischer, Stanley. "Globalization and Its Challenges." American Economic Review May 2003, p. 13.

- ^ Schumpeter, Joseph A. “The theory of Economic Development”, 1912, translated by Redvers Opie. Cambridge. MA: Harvard University Press, 1934.

- ^ World Bank, World Development Report, Washington DC, 1989, 9. 30.

- ^ Daron Acemoğlu, Simon Johnson and James A. Robinson.The Colonial Origins of Comparative Development: An Empirical Investigation. American Economic Review 91(5): 1369–401. 2001.

- ^ Mankiw, N. Gregory, David Romer, and David Weil. 1992. "A contribution to the empirics of economic growth." Quarterly Journal of Economics 107, no. 2 (May): 407–437; Sala-i-Martin, Xavier, Gernot Doppelhofer, and Ronald I. Miller. 2004. "Determinants of long-term growth: A Bayesian Averaging of Classical Estimates (BACE) approach." American Economic Review 94, no. 4 (September): 813–835; Romer, Paul. 1990. "Human capital and growth: Theory and evidence." Carnegie-Rochester Conference Series on Public Policy 32: 251–286.

- ^ Barro, Robert J., and Jong-Wha Lee. 2001. "International data on educational attainment: Updates and implications." Oxford Economic Papers 53, no. 3 (July): 541–563.

- ^ Hanushek, Eric A., and Dennis D. Kimko. 2000. "Schooling, labor force quality, and the growth of nations." American Economic Review 90, no. 5 (December): 1184–1208

- ^ Hanushek, Eric A., and Ludger Woessmann. 2008. "The role of cognitive skills in economic development." Journal of Economic Literature 46, no. 3 (September): 607–668; Hanushek, Eric A., and Ludger Woessmann. 2011. "How much do educational outcomes matter in OECD countries?" Economic Policy, 26, no. 67: 427–491.

- ^ In Pursuit of Happiness Research. Is It Reliable? What Does It Imply for Policy? The Cato institute. April 11, 2007

- ^ a b c d e f g h i j k Claire Melamed, Renate Hartwig and Ursula Grant 2011. Jobs, growth and poverty: what do we know, what don't we know, what should we know? London: Overseas Development Institute

- ^ a b Case, K.E., and Fair, R.C. 2006. Principles of Macroeconomics. Prentice Hall. ISBN 0-13-222645-6, ISBN 978-0-13-222645-5.

- ^ a b Beddoe, R.; Costanza, R.; Farley, J.; Garza, E.; Kent, J.; Kubiszewski, I.; Martinez, L.; Mccowen, T. et al.; Costanza, R; Farley, J; Garza, E; Kent, J; Kubiszewski, I; Martinez, L; Mccowen, T; Murphy, K; Myers, N; Ogden, Z; Stapleton, K; Woodward, J (Feb 2009). "Overcoming systemic roadblocks to sustainability: the evolutionary redesign of worldviews, institutions, and technologies" (Free full text). Proceedings of the National Academy of Sciences of the United States of America 106 (8): 2483–2489. doi:10.1073/pnas.0812570106. ISSN 0027-8424. PMC 2650289. PMID 19240221. http://www.pnas.org/cgi/pmidlookup?view=long&pmid=19240221.

- ^ a b "Chapter 17: Growth and Productivity-The Long-Run Possibilities". Oswego.edu. 1999-06-10. http://www.oswego.edu/~edunne/200ch17.html. Retrieved 2010-12-22.

- ^ a b Ronald Bailey (2004-02-04). "Science and Public Policy - Reason Magazine". Reason.com. http://www.reason.com/news/show/34758.html. Retrieved 2010-12-22.

- ^ a b Hayward, Steven F.. "That Old Time Religion". AEI. http://www.aei.org/publications/pubID.21588/pub_detail.asp. Retrieved 2010-12-22.

- ^ a b http://www.wired.com/wired/archive/5.02/ffsimon_pr.html

- ^ Wells, David A. (1891). Recent Economic Changes and Their Effect on Production and Distribution of Wealth and Well-Being of Society. New York: D. Appleton and Co.. ISBN 0543724743. http://books.google.com/?id=2V3qF4MWh_wC&printsec=frontcover&dq=RECENT+ECONOMIC+CHANGES+AND+THEIR+EFFECT+ON+DISTRIBUTION+OF+WEALTH+AND+WELL+BEING+OF+SOCIETY+WELLS#v=onepage&q&f=false.Opening line of the Preface.

- ^ Smil, Vaclav (2004). Enriching the Earth: Fritz Haber, Carl Bosch, and the Transformation of World Food Production. MIT Press. ISBN 0262693135.

- ^ Hall, Charles A.S.; Cleveland, Cutler J.; Kaufmann, Robert (1992). Energy and Resource Quality: The ecology of the Economic Process. Niwot, Colorado: University Press of Colorado.

- ^ "Overshoot" by William Catton, p. 3 [1980]

- ^ Donella H. Meadows, Jorgen Randers, Dennis L. Meadows. Limits to Growth: The 30-Year Update. White River Junction, Vermont : Chelsea Green, 2004. See also Allan Schnaiberg. The Environment: From Surpus to Scarcity. New York: Oxford University Press.

- ^ Jared Diamond. Collapse: How Societies Choose to Fail or Succeed. Penguin, 2006.

- ^ The Ultimate Resource, Julian Simon

- ^ a b c d Claire Melamed, Kate Higgins and Andy Sumner (2010) http://www.odi.org.uk/resources/details.asp?id=4892&title=millennium-development-goals-equitable-growth-policy-brief Economic growth and the MDGs] Overseas Development Institute

- ^ Ravallion, M. (2007) Inequality is bad for the poor in S. Jenkins and J. Micklewright, (eds.) Inequality and Poverty Re-examined, Oxford University Press, Oxford.

- ^ Stern Review, Part III Stabilization. Table 7.1 p. 168

- ^ Stern Review Economics of Climate Change. Part III Stabilization p.183

- ^ Jaccard, M. 2005 Sustainable Fossil Fuels. Cambridge University Press.

- ^ "Examination of Witnesses (Questions 32–39)". 16 May 2007. http://www.publications.parliament.uk/pa/jt200607/jtselect/jtclimate/170/7051604.htm. Retrieved 2007-11-29.

Further reading

- Edward J. Nell (1980) Growth, Profits and Property, edited by E.J. Nell, Cambridge: Cambridge University Press, 1980.

- Edward J. Nell (1988) Prosperity and Public Spending: Transformational Growth and the Role of the State, London, UK: Unwin and Hyman.

- Joseph Halevi, David Laibman and Edward J. Nell (eds.) (1992) Beyond the Steady State: Essays in the Revival of Growth Theory, edited with , London, UK:

- Barro, Robert J. (1997) Determinants of Economic Growth: A Cross-Country Empirical Study. MIT Press: Cambridge, MA.

- Edward J. Nell (1998) The General Theory of Transformational Growth: Keynes After Sraffa. Cambridge University Press, 1998.

- Edward J. Nell (1998) Transformational Growth and the Business Cycle, London, Routledge.

- Argyrous, G., Forstater, M and Mongiovi, G. (eds.) (2004) Growth, Distribution, And Effective Demand: Essays in Honor of Edward J. Nell. New York: M.E. Sharpe.

- Galor, O. (2005) From Stagnation to Growth: Unified Growth Theory. Handbook of Economic Growth, Elsevier.

- Jones, Charles I. (2002) Introduction to Economic Growth 2nd ed. W. W. Norton & Company: New York, N.Y.

- Kirzner, Israel. (1973) Competition and Entrepreneurship

- Edward J. Nell and Willi Semmler (eds.) (1991) Nicholas Kaldor and Mainstream Economics: Confrontation and Convergence, edited with Willi Semmler, Essays from the Kaldor Conference, London, UK: Macmillan, 1991.

- Puthenkalam, John Joseph, "Integrating Freedom, Democracy and Human Rights into Theories of Economic Growth", Manila, 1998.

- Lucas, Robert E., Jr. (2003) The Industrial Revolution: Past and Future, Federal Reserve Bank of Minneapolis, Annual Report online edition

- Mises, Ludwig E. (1949) Human Action 1998 reprint by the Mises Institute

- Schumpeter, Jospeph A. (1912) The Theory of Economic Development 1982 reprint, Transaction Publishers

- Weil, David N. (2008) Economic Growth 2nd ed. Addison Wesley.

- Vladimir N. Pokrovskii (2011) Econodynamics. The Theory of Social Production, Springer, Berlin.

External links

Articles and lectures

- Economic Growth by Paul Romer, The Concise Encyclopedia of Economics.

- "Economic growth." Encyclopædia Britannica. 2007. Encyclopædia Britannica Online. 17 November 2007.

- Beyond Classical and Keynesian Macroeconomic Policy. Paul Romer's plain-English explanation of endogenous growth theory.

- Does Economic Growth increase Living Standards?

- Who's afraid of economic growth? Essay by Daniel Ben-Ami on the contemporary anxiety about economic growth.

- CEPR Economics Seminar Series Two seminars on the importance of growth with economists Dean Baker and Mark Weisbrot

- On global economic history by Jan Luiten van Zanden. Explores the idea of the inevitability of the Industrial Revolution.

- The Economist Has No Clothes – essay by Robert Nadeau in Scientific American on the basic assumptions behind current economic theory

- World Growth Institute. An organization dedicated to helping the developing world realize its full potential via economic growth.

- Economics for Everyone- Evaluating Economic Growth

- Understanding the world today Multiple reports on economic growth

Data

- Historical data - since 1954 - comparing the US GDP growth rate versus the US Fed Funds Rate

- Angus Maddison's Historical Dataseries -Series for almost all countries on GDP, Population and GDP per capita from the year 0 up to 2003

- OECD Economic growth statistics

- multinational data sets easy to use data set showing gdp, per capita and population, by country and region, 1970 to 2008. Updated regularly.

Categories:- Economic growth

- Welfare economics

- Macroeconomics

- Economic indicators

- Economics terminology

Wikimedia Foundation. 2010.