- Business cycle

-

Economics  Economies by region

Economies by regionGeneral categories Microeconomics · Macroeconomics

History of economic thought

Methodology · Mainstream & heterodoxTechnical methods Mathematical economics

Game theory · Optimization

Computational · Econometrics

Experimental · National accountingFields and subfields Behavioral · Cultural · Evolutionary

Growth · Development · History

International · Economic systems

Monetary and Financial economics

Public and Welfare economics

Health · Education · Welfare

Population · Labour · Managerial

Business · Information

Industrial organization · Law

Agricultural · Natural resource

Environmental · Ecological

Urban · Rural · Regional · GeographyLists Business and Economics Portal The term business cycle (or economic cycle) refers to economy-wide fluctuations in production or economic activity over several months or years. These fluctuations occur around a long-term growth trend, and typically involve shifts over time between periods of relatively rapid economic growth (an expansion or boom), and periods of relative stagnation or decline (a contraction or recession).[1]

Business cycles are usually measured by considering the growth rate of real gross domestic product. Despite being termed cycles, these fluctuations in economic activity do not follow a mechanical or predictable periodic pattern.

Contents

History

Theory

The first systematic exposition of periodic economic crises, in opposition to the existing theory of economic equilibrium, was the 1819 Nouveaux Principes d'économie politique by Jean Charles Léonard de Sismondi.[2] Prior to that point classical economics had either denied the existence of business cycles,[3] blamed them on external factors, notably war,[4] or only studied the long term. Sismondi found vindication in the Panic of 1825, which was the first unarguably internal economic crisis, occurring in peacetime. Sismondi and his contemporary Robert Owen, who expressed similar but less systematic thoughts in 1817 Report to the Committee of the Association for the Relief of the Manufacturing Poor, both identified the cause of economic cycles as overproduction and underconsumption, caused in particular by wealth inequality. They advocated government intervention and socialism, respectively, as the solution. This work did not generate interest among classical economists, though underconsumption theory developed as a heterodox branch in economics until being systematized in Keynesian economics in the 1930s.

Sismondi's theory of periodic crises was developed into a theory of alternating cycles by Charles Dunoyer,[5] and similar theories, showing signs of influence by Sismondi, were developed by Johann Karl Rodbertus. Periodic crises in capitalism formed the basis of the theory of Karl Marx, who further claimed that these crises were increasing in severity and, on the basis of which, he predicted a communist revolution. He devoted hundreds of pages of Das Kapital to crises.

Classification by periods

Economic Waves series

(see Business cycles)

Cycle/Wave Name Years Kitchin inventory 3–5 Juglar fixed investment 7–11 Kuznets infrastructural investment 15–25 Kondratiev wave 45–60 In 1860, French economist Clement Juglar identified the presence of economic cycles 8 to 11 years long, although he was cautious not to claim any rigid regularity.[6] Later, Austrian economist Joseph Schumpeter argued that a Juglar cycle has four stages: (i) expansion (increase in production and prices, low interests rates); (ii) crisis (stock exchanges crash and multiple bankruptcies of firms occur); (iii) recession (drops in prices and in output, high interests rates); (iv) recovery (stocks recover because of the fall in prices and incomes). In this model, recovery and prosperity are associated with increases in productivity, consumer confidence, aggregate demand, and prices.

In the mid-20th century, Schumpeter and others proposed a typology of business cycles according to their periodicity, so that a number of particular cycles were named after their discoverers or proposers:[7]

- the Kitchin inventory cycle of 3–5 years (after Joseph Kitchin);[8]

- the Juglar fixed investment cycle of 7–11 years (often identified as 'the' business cycle);

- the Kuznets infrastructural investment cycle of 15–25 years (after Simon Kuznets);

- the Kondratiev wave or long technological cycle of 45–60 years (after Nikolai Kondratiev).[9]

Interest in these different typologies of cycles has waned since the development of modern macroeconomics, which gives little support to the idea of regular periodic cycles.[10]

Occurrence

There were frequent crises in Europe and America in the 19th and first half of the 20th century, specifically the period 1815–1939, starting from the end of the Napoleonic wars in 1815, which was immediately followed by the Post-Napoleonic depression in the United Kingdom (1815–30), and culminating in the Great Depression of 1929–39, which led into World War II. See Financial crisis: 19th century for listing and details. The first of these crises not associated with a war was the Panic of 1825.

Business cycles in the OECD after World War II were generally more restrained than the earlier business cycles, particularly during the Golden Age of Capitalism (1945/50–1970s), and the period 1945–2008 did not experience a global downturn until the Late-2000s recession. Economic stabilization policy using fiscal policy and monetary policy appeared to have dampened the worst excesses of business cycles, and automatic stabilization due to the aspects of the government's budget also helped mitigate the cycle even without conscious action by policy-makers.

In this period the economic cycle – at least the problem of depressions – was twice declared dead; first in the late 1960s, when Phillips curve was seen as being able to steer the economy – which was followed by stagflation in the 1970s, which discredited the theory, secondly in the early 2000s, following the stability and growth in the 1980s and 1990s in what came to be known as The Great Moderation – which was followed by the Late-2000s recession. Notably, in 2003, Robert Lucas, in his presidential address to the American Economic Association, declared that the "central problem of depression-prevention [has] been solved, for all practical purposes."[11]

Note however that various regions have experienced prolonged depressions, most dramatically the economic crisis in former Eastern Bloc countries following the end of the Soviet Union in 1991; for several of these countries the period 1989–2010 has been an ongoing depression, with real income still lower than in 1989.

Identifying

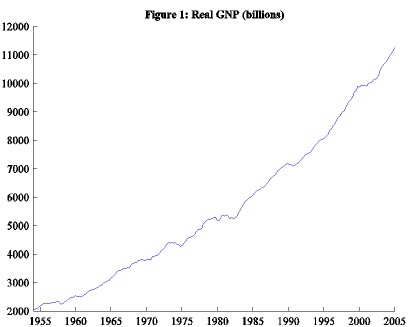

Economic activity in the US 1954–2005

Economic activity in the US 1954–2005

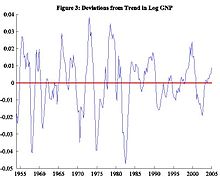

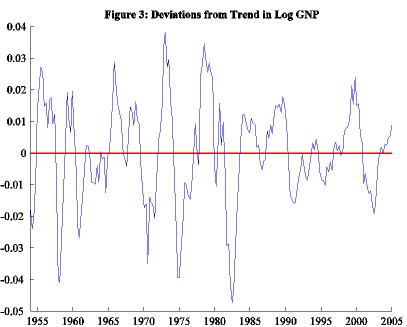

Deviations from the long term growth trend US 1954–2005

Deviations from the long term growth trend US 1954–2005In 1946, economists Arthur F. Burns and Wesley C. Mitchell provided the now standard definition of business cycles in their book Measuring Business Cycles:[12]

Business cycles are a type of fluctuation found in the aggregate economic activity of nations that organize their work mainly in business enterprises: a cycle consists of expansions occurring at about the same time in many economic activities, followed by similarly general recessions, contractions, and revivals which merge into the expansion phase of the next cycle; in duration, business cycles vary from more than one year to ten or twelve years; they are not divisible into shorter cycles of similar characteristics with amplitudes approximating their own.According to A. F. Burns:[13]

Business cycles are not merely fluctuations in aggregate economic activity. The critical feature that distinguishes them from the commercial convulsions of earlier centuries or from the seasonal and other short term variations of our own age is that the fluctuations are widely diffused over the economy—its industry, its commercial dealings, and its tangles of finance. The economy of the western world is a system of closely interrelated parts. He who would understand business cycles must master the workings of an economic system organized largely in a network of free enterprises searching for profit. The problem of how business cycles come about is therefore inseparable from the problem of how a capitalist economy functions.In the United States, it is generally accepted that the National Bureau of Economic Research (NBER) is the final arbiter of the dates of the peaks and troughs of the business cycle. An expansion is the period from a trough to a peak, and a recession as the period from a peak to a trough. The NBER identifies a recession as "a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production".[14]

Spectral analysis of business cycles

Recent research employing spectral analysis has confirmed the presence of Kondratiev waves in the world GDP dynamics at an acceptable level of statistical significance.[15][16] Korotayev et al. also detected shorter business cycles, dating the Kuznets to about 17 years and calling it the third harmonic of the Kondratiev, meaning that there are three Kuznets cycles per Kondratiev.

Cycles or fluctuations?

In recent years economic theory has moved towards the study of economic fluctuation rather than a 'business cycle'[17] – though some economists use the phrase 'business cycle' as a convenient shorthand. For Milton Friedman calling the business cycle a "cycle" is a misnomer, because of its non-cyclical nature. Friedman believed that for the most part, excluding very large supply shocks, business declines are more of a monetary phenomenon.[18]

Rational expectations theory leads to the efficient-market hypothesis, which states that no deterministic cycle can persist because it would consistently create arbitrage opportunities.[19] Much economic theory also holds that the economy is usually at or close to equilibrium.[citation needed] These views led to the formulation of the idea that observed economic fluctuations can be modeled as shocks to a system.

In the tradition of Slutsky, business cycles can be viewed as the result of stochastic shocks that on aggregate form a moving average series. However, the recent research employing spectral analysis has confirmed the presence of business (Juglar) cycles in the world GDP dynamics at an acceptable level of statistical significance.[15]

Explanations

The explanation of fluctuations in aggregate economic activity is one of the primary concerns of macroeconomics. The main framework for explaining such fluctuations is Keynesian economics. In the Keynesian view, business cycles reflect the possibility that the economy may reach short-run equilibrium at levels below or above full employment. If the economy is operating with less than full employment, i.e., with high unemployment, Keynesian theory states that monetary policy and fiscal policy can have a positive role to play in smoothing the fluctuations of the business cycle.

There are a number of alternative heterodox economic theories of business cycles, largely associated with particular schools or theorists. There are also some divisions and alternative theories within mainstream economics, notably real business cycle theory and credit-based explanations such as debt deflation and the financial instability hypothesis.

Exogenous vs. endogenous

Within mainstream economics, the debate over external (exogenous) versus internal (endogenous) being the causes of the economic cycles, with the classical school (now neo-classical) arguing for exogenous causes and the underconsumptionist (now Keynesian) school arguing for endogenous causes. These may also broadly be classed as "supply-side" and "demand-side" explanations: supply-side explanations may be styled, following Say's law, as arguing that "supply creates its own demand", while demand-side explanations argue that effective demand may fall short of supply, yielding a recession or depression.

This debate has important policy consequences: proponents of exogenous causes of crises such as neoclassicals largely argue for minimal government policy or regulation (laissez faire), as absent these external shocks, the market functions, while proponents of endogenous causes of crises such as Keynesians largely argue for larger government policy and regulation, as absent regulation, the market will move from crisis to crisis. This division is not absolute – some classicals (including Say) argued for government policy to mitigate the damage of economic cycles, despite believing in external causes, while Austrian School economists argue against government involvement as only worsening crises, despite believing in internal causes.

The view of the economic cycle as caused exogenously dates to Say's law, and much debate on endogeneity or exogeneity of causes of the economic cycle is framed in terms of refuting or supporting Say's law; this is also referred to as the "general glut" debate.

Until the Keynesian revolution in mainstream economics in the wake of the Great Depression, classical and neoclassical explanations (exogenous causes) were the mainstream explanation of economic cycles; following the Keynesian revolution, neoclassical macroeconomics was largely rejected. There has been some resurgence of neoclassical approaches in the form of real business cycle (RBC) theory. The debate between Keynesians and neo-classical advocates was reawakened following the recession of 2007.

Mainstream economists working in the neoclassical tradition, as opposed to the Keynesian tradition, have usually viewed the departures of the harmonic working of the market economy as due to exogenous influences, such as the State or its regulations, labor unions, business monopolies, or shocks due to technology or natural causes.

Contrarily, in the heterodox tradition of Jean Charles Léonard de Sismondi, Clement Juglar, and Marx the recurrent upturns and downturns of the market system are an endogenous characteristic of it.[20]

The 19th century school of Underconsumptionism also posited endogenous causes for the business cycle, notably the paradox of thrift, and today this previously heterodox school has entered the mainstream in the form of Keynesian economics via the Keynesian revolution.

Keynesian

According to Keynesian economics, fluctuations in aggregate demand cause the economy to come to short run equilibrium at levels that are different from the full employment rate of output. These fluctuations express themselves as the observed business cycles. Keynesian models do not necessarily imply periodic business cycles. However, simple Keynesian models involving the interaction of the Keynesian multiplier and accelerator give rise to cyclical responses to initial shocks. Paul Samuelson's "oscillator model"[21] is supposed to account for business cycles thanks to the multiplier and the accelerator. The amplitude of the variations in economic output depends on the level of the investment, for investment determines the level of aggregate output (multiplier), and is determined by aggregate demand (accelerator).

In the Keynesian tradition, Richard Goodwin[citation needed] accounts for cycles in output by the distribution of income between business profits and workers wages. The fluctuations in wages are almost the same as in the level of employment (wage cycle lags one period behind the employment cycle), for when the economy is at high employment, workers are able to demand rises in wages, whereas in periods of high unemployment, wages tend to fall. According to Goodwin, when unemployment and business profits rise, the output rises.

Credit/debt cycle

Main articles: Credit cycle and Debt deflationOne alternative theory is that the primary cause of economic cycles is due to the credit cycle: the net expansion of credit (increase in private credit, equivalently debt, as a percentage of GDP) yields economic expansions, while the net contraction causes recessions, and if it persists, depressions. In particular, the bursting of speculative bubbles is seen as the proximate cause of depressions, and this theory places finance and banks at the center of the business cycle.

A primary theory in this vein is the debt deflation theory of Irving Fisher, which he proposed to explain the Great Depression. A more recent complementary theory is the Financial Instability Hypothesis of Hyman Minsky, and the credit theory of economic cycles is often associated with Post-Keynesian economics such as Steve Keen.

Post-Keynesian economist Hyman Minsky has proposed a explanation of cycles founded on fluctuations in credit, interest rates and financial frailty, called the Financial Instability Hypothesis. In an expansion period, interest rates are low and companies easily borrow money from banks to invest. Banks are not reluctant to grant them loans, because expanding economic activity allows business increasing cash flows and therefore they will be able to easily pay back the loans. This process leads to firms becoming excessively indebted, so that they stop investing, and the economy goes into recession.

While credit causes have not been a primary theory of the economic cycle within the mainstream, they have gained occasional mention, such as (Eckstein & Sinai 1986), cited approvingly by (Summers 1986).

Real business cycle theory

Main article: Real Business Cycle theoryWithin mainstream economics, Keynesian views have been challenged by real business cycle models in which fluctuations are due to technology shocks. This theory is most associated with Finn E. Kydland and Edward C. Prescott, and more generally the Chicago school of economics (freshwater economics). They consider that economic crisis and fluctuations cannot stem from a monetary shock, only from an external shock, such as an innovation.

There were great increases in productivity, industrial production and real per capita product throughout period from 1870–1890 that included the Long Depression and two other recessions.[22][23] See:Long depression#Myth of the Long Depression There were also significant increases in productivity in the years leading up to the Great Depression. Both the Long and Great Depressions were characterized by overcapacity and market saturation.[24][25]

Over the period since the Industrial Revolution, technological progress has had a much larger effect on the economy than any fluctuations in credit or debt, the primary exception being the Great Depression, which caused a multi-year steep economic decline. The effect of technological progress can be seen by the purchasing power of an average hour's work, which has grown from $3 in 1900 to $22 in 1990, measured in 2010 dollars.[26] There were similar increases in real wages during the 19th century. See: Productivity improving technologies (historical) A table of innovations and long cycles can be seen at: Kondratiev wave#Modern modifications of Kondratiev theory

Carlota Perez blames "financial capital" for excess speculation, which she claims is likely to occur in the "frenzy" stage of a new technology, such as the 1998–2000 computer, internet, dot.com mania and bust. Perez also says excess speculation is likely to occur in the mature phase of a technological age.[27]

RBC theory has been categorically rejected by a number of mainstream economists in the Keynesian tradition, such as (Summers 1986) and Paul Krugman.

Politically-based business cycle

Another set of models tries to derive the business cycle from political decisions. The partisan business cycle suggests that cycles result from the successive elections of administrations with different policy regimes. Regime A adopts expansionary policies, resulting in growth and inflation, but is voted out of office when inflation becomes unacceptably high. The replacement, Regime B, adopts contractionary policies reducing inflation and growth, and the downwards swing of the cycle. It is voted out of office when unemployment is too high, being replaced by Party A.

The political business cycle is an alternative theory stating that when an administration of any hue is elected, it initially adopts a contractionary policy to reduce inflation and gain a reputation for economic competence. It then adopts an expansionary policy in the lead up to the next election, hoping to achieve simultaneously low inflation and unemployment on election day.[28]

The political business cycle theory is strongly linked to the name of Michał Kalecki[29] who argued that no democratic government under capitalism would allow the persistence of full employment [This sentence is confusing, and the reference given does not support this statement. Please clarify and correct the reference], so that recessions would be caused by political decisions. Persistent full employment would mean increasing workers' bargaining power to raise wages and to avoid doing unpaid labor, potentially hurting profitability. (He did not see this theory as applying under fascism, which would use direct force to destroy labor's power.) In recent years, proponents of the "electoral business cycle" theory have argued that incumbent politicians encourage prosperity before elections in order to ensure re-election—and make the citizens pay for it with recessions afterwards.

Marxist economics

For Marx the economy based on production of commodities to be sold in the market is intrinsically prone to crisis. In the heterodox Marxian view profit is the major engine of the market economy, but business (capital) profitability has a tendency to fall that recurrently creates crises, in which mass unemployment occurs, businesses fail, remaining capital is centralized and concentrated and profitability is recovered. In the long run these crises tend to be more severe and the system will eventually fail.[30] Some Marxist authors such as Rosa Luxemburg viewed the lack of purchasing power of workers as a cause of a tendency of supply to be larger than demand, creating crisis, in a model that has similarities with the Keynesian one. Indeed a number of modern authors have tried to combine Marx's and Keynes's views. Others have contrarily emphasized basic differences between the Marxian and the Keynesian perspective: while Keynes saw capitalism as a system worth maintaining and susceptible to efficient regulation, Marx viewed capitalism as a historically doomed system that cannot be put under societal control.[31]

Austrian school

Main article: Austrian business cycle theoryEconomists of the heterodox Austrian school argue that business cycles are primarily caused by excessive creation of bank credit – or fiduciary media – which is encouraged by central banks when they set interest rates too low, especially when combined with the practice of fractional reserve banking. The expansion of the money supply causes a "boom" in which resources are misallocated due to falsified interest rate signals, which then leads to the "bust" as the market self-corrects, the malinvestments are liquidated, and the money supply contracts.

One of the primary critiques of Austrian business cycle theory is the observation that the United States suffered recurrent economic crises in the 19th century, most notably the Panic of 1873, prior to the establishment of a U.S. central bank in 1913. Adherents, such as the historian Thomas Woods argue that these earlier financial crises were prompted by government and bankers' efforts to expand credit despite restraints imposed by the prevailing gold standard, and are thus consistent with Austrian Business Cycle Theory.

Georgism

Henry George identifies land price fluctuations as the primary cause of most business cycles.[32] The theory is generally ignored in most of today's discussions of the subject[33] despite the fact that the two great economic contractions of the last 100 years (1929–1933 and 2008–??) both involved speculative real estate bubbles.

George observed that one of the factors that is absolutely necessary for all production — land — has an inherent tendency to rise in price on an exponential basis as the economy grows. The reason for this is that the quantity of land (the stock of locations and natural resources) is fixed, while its quality is improved due to improvements such as transportation infrastructures and economic development of the surroundings. Investors see this tendency as the economy grows and they buy land ahead of the boom areas, withholding it from use in order to take advantage of its increased value in the future. Because housing and commercial real estate provide collateral for a large portion of lending, there is a tendency for real estate prices to rise faster than the rate of inflation in business cycle upswings.

Speculation in land concentrates profits in landholders and diverts economic resources to speculation in land, squeezing profits away from production that has to occur on this land.

In effect, land speculation creates a built-in supply shock, that squeezes the economy just as economic output increases. This is a systemic retardation of the economy, placing a sharp brake on further economic expansion. This shock to the economy occurs as long as there is land speculation, creating an underlying tendency toward inflation and recession late in the growth phase of the business cycle. Land speculation, according to George, is always the cause of economic downturns. There are any number of contributing causes; things like oil price shocks, consumer confidence crises, international trade fluctuations, natural disasters — but none of these things creates the underlying weakness.

Land speculation slows the economy in two ways. It increases production costs by making land in general more expensive (shifting the AS curve upward) as well as decreasing productivity by denying access to the best locations, shifting the AS curve to the left and lowering "potential output".[34]

The recent housing bubble offers some validation to George's theory and has created great distortions around the world. In the U.S. the bubble caused extreme regional differences in land prices, creating uncompetitive business conditions due to higher wages and taxes. State (CA, IL) and local governments in many of these high cost areas are suffering large budget shortfalls as businesses close or relocate to low cost areas such as the Atlanta, GA region, which has low land prices and was a leader in economic growth for the last several decades.

The Wisconsin Business School publishes an on line database with building cost and land values for 46 U.S. metro areas.[35]

Mitigating

Most social indicators (mental health, crimes, suicides) worsen during economic recessions. As periods of economic stagnation are painful for the many who lose their jobs, there is often political pressure for governments to mitigate recessions. Since the 1940s, following the Keynesian revolution, most governments of developed nations have seen the mitigation of the business cycle as part of the responsibility of government, under the rubric of stabilization policy.

Since in the Keynesian view, recessions are caused by inadequate aggregate demand, when a recession occurs the government should increase the amount of aggregate demand and bring the economy back into equilibrium. This the government can do in two ways, firstly by increasing the money supply (expansionary monetary policy) and secondly by increasing government spending or cutting taxes (expansionary fiscal policy).

By contrast, some economists, notably New classical economist Robert Lucas, argue that the welfare cost of business cycles are very small to negligible, and that governments should focus on long-term growth instead of stabilization.

However, even according to Keynesian theory, managing economic policy to smooth out the cycle is a difficult task in a society with a complex economy. Some theorists, notably those who believe in Marxian economics, believe that this difficulty is insurmountable. Karl Marx claimed that recurrent business cycle crises were an inevitable result of the operations of the capitalistic system. In this view, all that the government can do is to change the timing of economic crises. The crisis could also show up in a different form, for example as severe inflation or a steadily increasing government deficit. Worse, by delaying a crisis, government policy is seen as making it more dramatic and thus more painful.

Additionally, since the 1960s neoclassical economists have played down the ability of Keynesian policies to manage an economy. Since the 1960s, economists like Nobel Laureates Milton Friedman and Edmund Phelps have made ground in their arguments that inflationary expectations negate the Phillips curve in the long run. The stagflation of the 1970s provided striking support for their theories, defying the simple Keynesian prediction that recessions and inflation cannot occur together.[original research?] Friedman has gone so far as to argue that all the central bank of a country should do is to avoid making large mistakes, as he believes they did by contracting the money supply very rapidly in the face of the Wall Street Crash of 1929, in which they made what would have been a recession into the Great Depression.[citation needed]

See also

- Dynamic stochastic general equilibrium

- Welfare cost of business cycles

- World-systems approach

- Information revolution

- Innovation saturation

- Market trend

- Skyscraper Index

- Inventory investment over the business cycle

Notes

- ^ O'Sullivan, Arthur; Steven M. Sheffrin (2003). Economics: Principles in action. Upper Saddle River, New Jersey 07458: Pearson Prentice Hall. pp. 57, 310. ISBN 0-13-063085-3. http://www.pearsonschool.com/index.cfm?locator=PSZ3R9&PMDbSiteId=2781&PMDbSolutionId=6724&PMDbCategoryId=&PMDbProgramId=12881&level=4.

- ^ Over Production and Under Consumption, ScarLett, History Of Economic Theory and Thought

- ^ Batra, R. (2002). "Economics in Crisis: Severe and Logical Contradictions of Classical, Keynesian, and Popular Trade Models".

- ^ http://www.thefreemanonline.org/featured/classical-economists-good-or-bad/

- ^ Charles Dunoyer and the Emergence of the Idea of an Economic Cycle, Rabah Benkemoune, History of Political Economy 2009 41(2):271–295; DOI:10.1215/00182702-2009-003

- ^ M. W. Lee, Economic fluctuations. Homewood, IL, Richard D. Irwin, 1955

- ^ Schumpeter, J. A. (1954). History of Economic Analysis. London: George Allen & Unwin.

- ^ Kitchin, Joseph (1923). "Cycles and Trends in Economic Factors". Review of Economics and Statistics (The MIT Press) 5 (1): 10–16. doi:10.2307/1927031. JSTOR 1927031.

- ^ Kondratieff, N. D.; Stolper, W. F. (1935). "The Long Waves in Economic Life". Review of Economics and Statistics (The MIT Press) 17 (6): 105–115. doi:10.2307/1928486. JSTOR 1928486.

- ^ http://www.albany.edu/~bd445/Eco_301/Slides/Business_Cycle_Notes_(Print).pdf

- ^ Fighting Off Depression, New York Times, http://www.nytimes.com/2009/01/05/opinion/05krugman.html

- ^ A. F. Burns and W. C. Mitchell, Measuring business cycles, New York, National Bureau of Economic Research, 1946.

- ^ A. F. Burns, Introduction. In: Wesley C. Mitchell, What happens during business cycles: A progress report. New York, National Bureau of Economic Research, 1951

- ^ "US Business Cycle Expansions and Contractions". NBER. http://www.nber.org/cycles.html. Retrieved 2009-02-20.[dead link]

- ^ a b See, e.g. Korotayev, Andrey V., & Tsirel, Sergey V. A Spectral Analysis of World GDP Dynamics: Kondratieff Waves, Kuznets Swings, Juglar and Kitchin Cycles in Global Economic Development, and the 2008–2009 Economic Crisis. Structure and Dynamics. 2010. Vol.4. #1. P.3-57.

- ^ Spectral analysis is a mathematical technique that is used in such fields as electrical engineering for analyzing electrical circuits and radio waves to deconstruct a complex signal to determine the main frequencies and their relative contribution. Signal analysis is usually done with equipment. Data analysis is done with special computer software.

- ^ Mankiw, Gregory (1989). "Real Business Cycles: A New Keynesian Perspective". The Journal of Economic Perspectives (JSTOR) 3 (3): 79–90. ISSN 0895-3309. JSTOR 1942761.

- ^ Milton and Rose D. Friedman, Two Lucky People,(Chicago, Illinois: University of Chicago Press, 1998) p. 50. On that page Milton Friedman admits to "skepticism about whether there is indeed an economic phenomenon justifying the designation`cycle,' or whether the economic fluctuations glorified by that title are not merely reactions to a series of random shocks, along the lines of a famous 1927 article by Eugen Slutsky." Friedman, Milton; Anna Jacobson Schwartz (1993). A Monetary History of the United States, 1867–1960. Princeton: Princeton University Press. pp.678

- ^ Template:Social Science Research Network

- ^ Mary S. Morgan, The History of Econometric Ideas, Cambridge University Press, 1991.

- ^ Samuelson, P. A., 1939, Interactions between the multiplier analysis and the principle of acceleration, Review of Economic Statistics 21, 75–78

- ^ Wells, David A. (1890). Recent Economic Changes and Their Effect on Production and Distribution of Wealth and Well-Being of Society. New York: D. Appleton and Co.. ISBN 0543724743. http://books.google.com/?id=2V3qF4MWh_wC&printsec=frontcover&dq=RECENT+ECONOMIC+CHANGES+AND+THEIR+EFFECT+ON+DISTRIBUTION+OF+WEALTH+AND+WELL+BEING+OF+SOCIETY+WELLS#v=onepage&q&f=false.

- ^ Rothbard, Murray (2002). History of Money and Banking in the United States. Ludwig Von Mises Inst. ISBN 0945466331. http://mises.org/books/historyofmoney.pdf.

- ^ Wells, David A. (1890). Recent Economic Changes and Their Effect on Production and Distribution of Wealth and Well-Being of Society. New York: D. Appleton and Co.. ISBN 0543724743. http://books.google.com/?id=2V3qF4MWh_wC&printsec=frontcover&dq=RECENT+ECONOMIC+CHANGES+AND+THEIR+EFFECT+ON+DISTRIBUTION+OF+WEALTH+AND+WELL+BEING+OF+SOCIETY+WELLS#v=onepage&q&f=false.Opening line of the Preface.

- ^ Beaudreau, Bernard C. (1996). Mass Production, the Stock Market Crash and the Great Depression. New York, Lincoln, Shanghi: Authors Choice Press.

- ^ Lebergott, Stanley (1993). Pursuing Happiness: American Consumers in the Twentieth Century. Princeton, NJ: Princeton University Press. pp. a:Adapted from Fig. 9.1. ISBN 0-691-04322-1.

- ^ [|Perez, Carlota] (2002). Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. UK: Edward Elgar Publishing Limited. ISBN 1843763311.

- ^ • Allan Drazen, 2008. "political business cycles," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

• William D. Nordhaus, 1989:2. "Alternative Approaches to the Political Business Cycle," Brookings Papers on Economic Activity, p p. 1-68. - ^ Michal Kalecki, 1899–1970.

- ^ Henryk Grossmann Das Akkumulations- und Zusammenbruchsgesetz des kapitalistischen Systems (Zugleich eine Krisentheorie), Hirschfeld, Leipzig, 1929

- ^ Paul Mattick, Marx and Keynes: The Limits of Mixed Economy, Boston, Porter Sargent, 1969

- ^ George, Henry. (1881). Progress and Poverty: An Inquiry into the Cause of Industrial Depressions and of Increase of Want with Increase of Wealth; The Remedy. Kegan Paul (reissued by Cambridge University Press, 2009; ISBN 978-1-108-00361-2)

- ^ Hansen, Alvin H. Business Cycles and National Income. New York: W. W. Norton & Company, 1964, p 39

- ^ Quote from Henry George on real causes of business cycles

- ^ Wisconsin School of Business & The Lincoln Institute of Land Policy (Updated Quarterly). "Land Prices for 46 Metro Areas". http://www.lincolninst.edu/subcenters/land-values/metro-area-land-prices.asp

References

- From (2008) The New Palgrave Dictionary of Economics, 2nd Edition:

- Christopher J. Erceg. "monetary business cycle models (sticky prices and wages)." Abstract.

- Christian Hellwig. "monetary business cycles (imperfect information)." Abstract.

- Ellen R. McGrattan "real business cycles." Abstract.

- Eckstein, Otto; Allen Sinai (1990). "1. The Mechanisms of the Business Cycle in the Postwar Period". In Robert J. Gordon. The American Business Cycle: Continuity and Change. University of Chicago Press. ISBN 9780226304533. http://books.google.com/?id=P2f-icI-fM0C&pg=PA39.

- Summers, Lawrence H. (1986). "Some Skeptical Observations on Real Business Cycle Theory". Federal Reserve Bank of Minneapolis Quarterly Review 10 (Fall): 23–27. http://www.minneapolisfed.org/research/QR/QR1043.pdf.

Categories:

Wikimedia Foundation. 2010.