- Long Depression

-

Not to be confused with long-term depression.

The Long Depression was a worldwide economic crisis, felt most heavily in Europe and the United States, which had been experiencing strong economic growth fueled by the Second Industrial Revolution and the conclusion of the American Civil War. At the time, the episode was labeled the Great Depression, and held that title until the Great Depression of the 1930s. Though a period of general deflation and low growth began in 1873, (ending about 1896), it did not have the severe "economic retrogression [and] spectacular breakdown" of the latter Great Depression.[1]

It was most notable in Western Europe and North America, at least in part because reliable data from the period is most readily available in those parts of the world. The United Kingdom is often considered to have been the hardest hit; during this period it lost some of its large industrial lead over the economies of Continental Europe.[2] While it was occurring, the view was prominent that the economy of the United Kingdom had been in continuous depression from 1873 to as late as 1896 and some texts refer to the period as the Great Depression of 1873–96.[3]

In the United States, economists typically refer to the Long Depression as the Depression of 1873–79, kicked off by the Panic of 1873, and followed by the Panic of 1893, book-ending the entire period of the wider Long Depression.[4] The National Bureau of Economic Research dates the contraction following the panic as lasting from October 1873 to March 1879. At 65 months, it is the longest-lasting contraction identified by the NBER, eclipsing the Great Depression's 43 months of contraction.[5][6]

In the US, from 1873-1879, 18,000 businesses went bankrupt, including hundreds of banks, while unemployment peaked at 14% in 1876[7], long after the panic ended. While most others agree the entire depression was harmful, Economist Murray Rothbard claimed that after the panic, the economy entered a period of rapid growth, with the U.S. growing at the fastest rates ever in its history in the 1870s and 1880s.[8]

Contents

Background

The period preceding the depression was dominated by several major military conflicts and a period of economic expansion. In Europe, the end of the Franco-Prussian War yielded a new political order in Germany, and the £200 million reparations imposed on France led to an inflationary investment boom in Germany and central Europe.[9] New technologies in industry such as the Bessemer converter were being rapidly applied; railroads were booming.[9] In the United States, the end of the American Civil War and a brief post-war recession (1865–1867) gave way to such an investment boom, focused especially on railroads on public lands in the West - an expansion funded greatly by foreign investors.[9]

Causes of the crisis

Main article: Panic of 1873 Run on the Fourth National Bank, No. 20 Nassau Street, New York City, 1873. From Frank Leslie's Illustrated Newspaper, October 4, 1873.

Run on the Fourth National Bank, No. 20 Nassau Street, New York City, 1873. From Frank Leslie's Illustrated Newspaper, October 4, 1873.

The Panic of 1873 has been described as "the first truly international crisis".[9] The optimism that had been driving booming stock prices in central Europe had reached a fever pitch, and fears of a bubble culminated in a panic in Vienna beginning in April 1873. The collapse of the Vienna Stock Exchange began on May 8, 1873 and continued until May 10, when the exchange was closed; when it was reopened three days later, the panic seemed to have faded, and appeared confined to Austria-Hungary.[9] Financial panic arrived in America only months later on Black Thursday, September 18, 1873 after the failure of the banking house of Jay Cooke and Company over the Northern Pacific Railway.[10] The Northern Pacific railway had been given 40 million acres (160,000 km2) of public land in the West and Jay Cooke sought $100,000,000 in capital for the company; the bank failed when the bond issue proved unsalable, and was shortly followed by several other major banks. The New York Stock Exchange closed for ten days on September 20.[9]

The financial contagion then returned to Europe, provoking a second panic in Vienna and further failures in continental Europe before receding. France, which had been experiencing deflation in the years preceding the crash, was spared financial calamity for the moment, as was Britain.[9]

Others have argued the depression was rooted in the 1870 Franco-Prussian War that hurt the French economy and, under the Treaty of Frankfurt (1871), forced that country to make large war reparations payments to Germany. The primary cause of the price depression in the United States was the tight monetary policy that the U.S. followed to get back to the gold standard after the Civil War. The U.S. was taking money out of circulation to achieve this goal, therefore there was less available money to facilitate trade. Because of the monetary policy the price of silver started to fall causing considerable losses of asset values; by most accounts, after 1879 production was growing, thus further putting downward pressure on prices due to increased industrial productivity, trade and competition.

In America the speculative nature of financing due to both the greenback which was paper currency issued to pay for the US Civil War and rampant fraud in the building of the Union Pacific Railway up to 1869 culminated in the Credit Mobilier panic. Railway overbuilding and weak markets collapsed the bubble in 1873. Both the Union Pacific and the Northern Pacific lines were center in the collapse; another railway bubble was the UK railway mania.

Because of the Panic of 1873, governments depegged their currencies, to save money. The demonetization of silver by European and North American governments in the early 1870s was certainly a contributing factor. The Coinage Act of 1873 in America was met with great opposition by farmers and miners, as silver was seen as more of a monetary benefit to rural areas than to banks in big cities. In addition, there were Americans who advocated the continuance of government-issued fiat money (United States Notes) to avoid deflation and promote exports. The western US states were outraged—Nevada, Colorado, and Idaho were huge silver producers with productive mines, and for a few years mining abated. The resumption of the US government buying silver was enacted in 1890 with the Sherman Silver Purchase Act.

Monetarists believe that the 1873 depression was caused by shortages of gold that undermined the gold standard, and that the 1848 California Gold Rush, 1886 Witwatersrand Gold Rush in South Africa and the 1896–99 Klondike Gold Rush helped alleviate such crises. Other analyses have pointed to developmental surges (see Kondratiev wave), theorizing that the Second Industrial Revolution was causing large shifts in the economies of many states, imposing transition costs, which may also have played a role in causing the depression.

Course of the depression

Like the later Great Depression, the Long Depression affected different countries at different times, at different rates, and some countries accomplished rapid growth over certain periods. Globally, however, the 1870s, 1880s, and 1890s were a period of falling price levels and rates of economic growth significantly below the periods preceding and following.

Between 1870 and 1890, iron production in the five largest producing countries more than doubled, from 11 million tons to 23 million tons, steel production increased twentyfold (half a million tons to 11 million tons), and railroad development boomed.[11] But at the same time, prices in several markets collapsed - the price of grain in 1894 was only a third what it had been in 1867,[12] and the price of cotton fell by nearly 50 percent in just the five years from 1872 to 1877,[13] imposing great hardship on farmers and planters. This collapse provoked protectionism in many countries, such as France, Germany, and the United States,[12] while triggering mass emigration from other countries such as Italy, Spain, Austria-Hungary, and Russia.[14] Similarly, while the production of iron doubled between the 1870s and 1890s,[11] the price of iron halved.[12]

Many countries experienced significantly lower growth rates relative to what they had experienced earlier in the 19th century and to what they experienced afterwards:

Growth rates of industrial production (1850s–1913)[15] 1850s–1873 1873–1890 1890–1913  Germany

Germany4.3 2.9 4.1  United Kingdom

United Kingdom3.0 1.7 2.0  United States

United States6.2 4.7 5.3  France

France1.7 1.3 2.5  Italy

Italy0.9 3.0  Sweden

Sweden3.1 3.5 GNP of the Great Powers of Europe

(in billions USD, 1960 prices)[16]1830 1840 1850 1860 1870 1880 1890  Russia

Russia10.5 11.2 12.7 14.4 22.9 23.2 21.1 France8.5 10.3 11.8 13.3 16.8 17.3 19.7 United Kingdom8.2 10.4 12.5 16.0 19.6 23.5 29.4 Germany7.2 8.3 10.3 12.7 16.6 19.9 26.4  Austria-Hungary

Austria-Hungary7.2 8.3 9.1 9.9 11.3 12.2 15.3 Italy5.5 5.9 6.6 7.4 8.2 8.7 9.4 Austria-Hungary

The global economic crisis first erupted in Austria-Hungary, where in May 1873 the Vienna Stock Exchange crashed.[9] In Hungary, the panic of 1873 terminated a mania of railroad-building.[17]

France

France's experience was somewhat unique. Having been defeated in the Franco-Prussian War, the country was required to pay £200 million in reparations to the Germans and was already reeling when the 1873 crash occurred.[9] The French adopted a policy of deliberate deflation while paying off the reparations.[9]

While the United States resumed growth for a time in the 1880s, the Paris Bourse crash of 1882 sent France careening into depression, one which "lasted longer and probably cost France more than any other in the 19th century".[18] The Union Générale, a French bank, failed in 1882, prompting the French to withdraw three million pounds from the Bank of England and triggering a collapse in French stock prices.[19]

The financial crisis was compounded by diseases impacting the wine and silk industries[18] French capital accumulation and foreign investment plummeted to the lowest levels experienced by France in the latter half of the 19th century.[18] After a boom in new investment banks after the end of the Franco-Prussian War, the destruction of the French banking industry wrought by the crash cast a pall over the financial sector that lasted until the dawn of the 20th century.[18] French finances were further sunk by failing investments abroad, principally in railroads.[17] The French net national product declined over the ten years from 1882 to 1892.[20]

Italy

A ten-year tariff war broke out between France and Italy after 1887, damaging Franco-Italian relations which had prospered during Italian Unification. As France was Italy's biggest investor, the liquidation of French assets in the country was especially damaging.[20]

Russia

The Russian experience was similar to the US experience - three separate recessions, concentrated in manufacturing, occurred in the period (1874–1877, 1881–1886, and 1891–1892), separated by periods of recovery.[21]

United Kingdom

The United Kingdom, which had previously experienced crises every decade since the 1820s, was unusually insulated from the effects of this financial crisis, even though the Bank of England kept interest rates as high as 9 percent in the 1870s.[9]

Building on an 1870 reform, and the 1879 famine, thousands of Irish tenant farmers affected by depressed producer prices and high rents launched the Land War in 1879, which resulted in the reforming Irish Land Acts.

United States

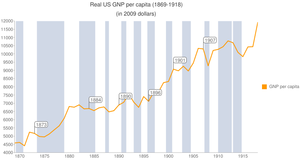

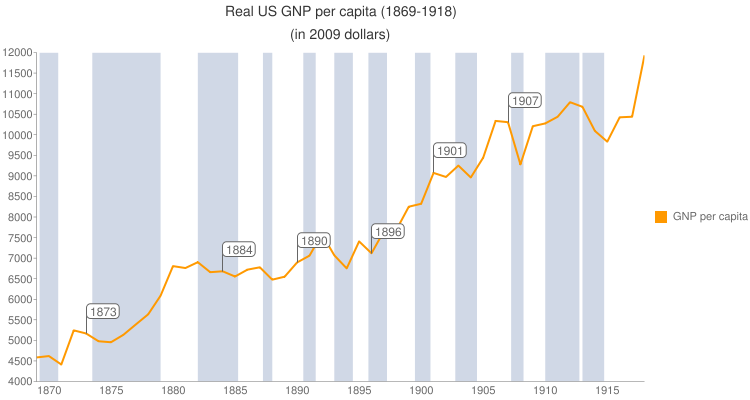

Estimated declines in United States manufacturing output in selected sectors (1872–1876)[22] Industry % decline in output Durable goods 30% Iron and steel 45% Construction 30% Overall 10% In the United States, the Long Depression began with the Panic of 1873. The National Bureau of Economic Research dates the contraction following the panic as lasting from October 1873 to March 1879. At 65 months, it is the longest-lasting contraction identified by the NBER, eclipsing the Great Depression's 43 months of contraction.[5][23] Figures from Milton Friedman and Anna Schwartz show net national product increased 3 percent per year from 1869 to 1879 and real national product grew at 6.8 percent per year during that time frame.[24] However, since between 1869 and 1879 the population of the United States increased by over seventeen and one-half percent,[25] per capita NNP growth was lower. Following the end of the episode in 1879, the U.S. economy would remain unstable, experiencing recessions for 114 of the 253 months until January 1901.[5]

The dramatic shift in prices mauled nominal wages - in the United States, nominal wages declined by one-quarter during the 1870s,[10] and as much as one-half in some places, such as Pennsylvania.[26] Although real wages had enjoyed robust growth in the aftermath of the American Civil War, increasing by nearly a quarter between 1865 and 1873, they stagnated until the 1880s, posting no real growth, before resuming their robust rate of expansion in the later 1880s.[27] The collapse of cotton prices devastated the already war-ravaged economy of the southern United States.[13] Although farm prices fell dramatically, American agriculture continued to expand production.[22]

Thousands of American businesses failed, defaulting on more than a billion dollars of debt.[26] One in four laborers in New York were out of work in the winter of 1873-1874[26] and, nationally, a million became unemployed.[26]

The sectors which experienced the most severe declines in output were manufacturing, construction, and railroads.[22] The railroads had been a tremendous engine of growth in the years before the crisis, yielding a 50% increase in railroad mileage from 1867 to 1873.[22] After absorbing as much as 20% of US capital investment in the years preceding the crash, this expansion came to a dramatic end in 1873; between 1873 and 1878, the total amount of railroad mileage in the United States barely increased at all.[22]

The Freedman's Savings Bank was a typical casualty of the financial crisis. Chartered in 1865 in the aftermath of the American Civil War, the bank had been established to advance the economic welfare of America's newly emancipated freedmen.[28] In the early 1870s, the bank had joined in the speculative fever, investing in real estate and unsecured loans to railroads; its collapse in 1874 was a severe blow to African-Americans.[28]

The recession exacted a harsh political toll on President Ulysses S. Grant. Historian Allan Nevins says of the end of Grant's presidency:[29]

Various administrations have closed in gloom and weakness ... but no other has closed in such paralysis and discredit as (in all domestic fields) did Grant's. The President was without policies or popular support. He was compelled to remake his Cabinet under a grueling fire from reformers and investigators; half its members were utterly inexperienced, several others discredited, one was even disgraced. The personnel of the departments was largely demoralized. The party that autumn appealed for votes on the implicit ground that the next Administration would be totally unlike the one in office. In its centennial year, a year of deepest economic depression, the nation drifted almost rudderless.[29]Recovery began in 1878. The mileage of railroad track laid down increased from 2,665 mi (4,289 km) in 1878 to 11,568 in 1882.[22] Construction began recovery by 1879; the value of building permits increased two and a half times between 1878 and 1883, and unemployment fell to 2.5% in spite of high immigration.[19]

The recovery, however, proved short-lived. Business profits declined steeply between 1882 and 1884.[19] The recovery in railroad construction reversed itself, falling from 11,569 mi (18,619 km) of track laid in 1882 to 2,866 mi (4,612 km) of track laid in 1885; the price of steel rails collapsed from $71/ton in 1880 to $20/ton in 1884.[19] Manufacturing again collapsed - durable goods output fell by a quarter again.[19] The decline became another financial crisis in 1884, when multiple New York banks collapsed; simultaneously, in 1883-1884, tens of millions of dollars of foreign-owned American securities were sold out of fears that the United States was preparing to abandon the gold standard.[19] This financial panic destroyed eleven New York banks, more than a hundred state banks, and led to defaults on at least $32 million worth of debt.[19] Unemployment, which had stood at 2.5% between recessions, surged to 7.5% in 1884-1885, and 13% in the northeastern United States, even as immigration plunged in response to deteriorating labor markets.[19]

This second recession led to further deterioration of farm prices. Kansas farmers burned their own corn in 1885 because it was worth less than other fuels such as coal or wood.[19] The country began to recover in 1885.[19]

Reactions to the crisis

Protectionism

The period preceding the Long Depression was one of increasing economic internationalism, championed by efforts such as the Latin Monetary Union, many of which were derailed or stunted by the impacts of economic uncertainty.[30] The extraordinary collapse of farm prices[12] provoked a protectionist response in many nations. Rejecting the free trade policies of the Second Empire, French president Adolphe Thiers led the new Third Republic to protectionism, leading ultimately to the stringent Méline tariff in 1892.[31] Germany's agrarian Junker aristocracy - under attack by cheap, imported grain - successfully agitated for a protective tariff in 1879 in Bismarck's Germany over the protests of his National Liberal Party allies.[31] In 1887, Italy and France embarked on a bitter tariff war.[32] In the United States, Benjamin Harrison won the 1888 US presidential election on a protectionist ticket.[33]

As a result of the protectionist policies enacted by the world's major trading nations, the global merchant marine fleet posted no significant growth over the period 1870-1890, before nearly doubling in tonnage in the prewar economic boom that followed.[34] Only the United Kingdom and the Netherlands remained committed to low tariffs.[32]

Monetary responses

In 1874, a year after the 1873 crash, the United States Congress passed legislation called the Inflation Bill of 1874 designed to confront the issue of falling prices by injecting fresh greenbacks into the money supply.[35] Under pressure from business interests, President Grant vetoed the measure.[35] In 1878, Congress overrode President Hayes's veto to pass the Silver Purchase Act, in a similar but more successful attempt to promote "easy money."[22]

Labor unrest

The United States endured its first nationwide strike in 1877, the Great Railroad Strike of 1877.[22]

New Imperialism

Main article: New ImperialismThe Long Depression contributed to the revival of colonialism leading to the New Imperialism period, symbolized by the scramble for Africa, as the western powers sought new markets for their goods.[36] According to Hannah Arendt's The Origins of Totalitarianism (1951), the "unlimited expansion of power" followed the "unlimited expansion of capital".[37]

In the United States, beginning in 1878-1879, the rebuilding, extending, and refinancing of the western railways, commensurate with the wholesale giveaway of water, timber, fish, minerals, in what had previously been Indian territory, characterized a rising market. This of course led to the expansion of markets and industry, together with the robber barons of railroad owners which culminated in the genteel 1880s and 1890s. The Gilded Age was the outcome for the few rich. The cycle repeated itself with another huge market crash in 1893.

Recovery

In the United States, the National Bureau of Economic Analysis dates the recession through March 1879. In January 1879, the United States returned to the gold standard which it had abandoned during the Civil War; according to economist Rendigs Fels, the gold standard put a floor to the deflation, and this was further boosted by especially good agricultural production in 1879.[38] The view that a single recession lasted from 1873 to 1896 or 1897 is not supported by most modern reviews of the period. It has even been suggested that the trough of this business cycle may have occurred as early as 1875.[39] In fact, from 1869 to 1879, the US economy grew at a rate of 6.8% for real net national product (NNP) and 4.5% for real NNP per capita.[40] Real wages were flat from 1869 to 1879, while from 1879 to 1889, nominal wages rose 23% and prices fell 4.2%.[41]

Explanations

Irving Fisher believed that the Panic of 1873 and the severity of the contractions which followed it could be explained by debt and deflation. Fisher believed that a financial panic would trigger catastrophic deleveraging in an attempt to sell assets and increase capital reserves; this sell-off would trigger a collapse in asset prices and deflation, which would in turn prompt financial institutions to sell off more assets, only to further deflation and strain capital ratios. Fisher believed that had governments or private enterprise embarked on efforts to reflate financial markets, the crisis would have been less severe.[42]

David Ames Wells (1890) wrote of the technological advancements during the period 1870-90, which included the Long Depression. Wells gives an account of the changes in the world economy transitioning into the Second Industrial Revolution in which he documents changes in trade, such as triple expansion steam shipping, railroads, the effect of the international telegraph network and the opening of the Suez Canal.[43] Wells gives numerous examples of productivity increases in various industries and discusses the problems of excess capacity and market saturation.

Wells opening sentence:

“The economic changes that have occurred during the last quarter of a century -or during the present generation of living men- have unquestionably been more important and more varied than during any period of the world’s history”.

Other changes Wells mentions are reductions in warehousing and inventories, elimination of middlemen, economies of scale, the decline of craftsmen and the displacement of agricultural workers. About the whole 1870-90 period Wells said:

"Some of these changes have been destructive, and all of them have inevitably occasioned, and for a long time yet will continue to occasion, great disturbances in old methods, and entail losses of capital and changes in occupation on the part of individuals. And yet the world wonders, and commissions of great states inquire, without coming to definite conclusions, why trade and industry in recent years has been universally and abnormally disturbed and depressed."

Wells notes that many of the government inquires on the “depression of prices” (deflation) found various reasons such as the scarcity of gold and silver. Wells showed that the U.S. money supply actually grew over the period of the deflation. Wells noted that deflation only lowered the cost of goods that benefited from improved methods of manufacturing and transportation. Goods produced by craftsmen did not decrease in value, nor did many services, and the cost of labor actually increased. Also, deflation did not occur in countries that did not have modern manufacturing, transportation and communications.

Nobel laureate economist Milton Friedman, author of A Monetary History of the United States, on the other hand, blamed this prolonged economic crisis on the imposition of a new gold standard, part of which he referred to by its traditional name, The Crime of 1873[44]. This forced shift into a currency whose supply was limited by nature, unable to expand with demand, caused a series of economic and monetary contractions that plagued the entire period of the Long Depression.

Interpretations

Most economic historians see this period as negative for the United States. They argue that most of the stagnation was caused by a monetary contraction caused by abandonment of the bimetallic standard, for a new fiat gold standard, starting with the Coinage Act of 1873. Some economic historians have complained about the characterization as this period as a "depression". However, this period saw a relatively large expansion of industry, of railroads, of physical output, of net national product, and real per capita income. As Friedman and Schwartz have stated, the decade from 1869 to 1879 saw a 3-percent-per annum increase in money national product, an outstanding real national product growth of 6.8 percent per year in this period, and a phenomenal rise of 4.5 percent per year in real product per capita. Even the alleged "monetary contraction" never took place, the money supply increasing by 2.7 percent per year in this period. From 1873 through 1878, before another spurt of monetary expansion, the total supply of bank money rose from $1.964 billion to $2.221 billion—a rise of 13.1 percent or 2.6 percent per year. In short, a modest but definite rise, and scarcely a contraction.[45] Although per-capita nominal income declined very gradually from 1873 to 1879, that decline was more than offset by a gradual increase over the course of the next 17 years.

Furthermore, real per-capita income either stayed approximately constant (1873-1880; 1883-1885) or rose (1881-1882; 1886-1896), so that the average consumer appears to have been considerably better off at the end of the 'depression' than before. Studies of other countries where prices also tumbled, including the US, Germany, France, and Italy, reported more markedly positive trends in both nominal and real per-capita income figures. Profits generally were also not adversely affected by deflation, although they declined (particularly in Britain) in industries that were struggling against superior, foreign competition. Furthermore, some economists argue that deflation is not inherently harmful to an economy and cite the economic growth of the period as evidence of this.[46] Rothbard further denies that a monetary contraction took place because the money supply increasing by 2.7 percent per year in this period. Again, this spoke to a difference between him and most other economists, including Mises, Friedman, and Hayek, all of whom defined inflation/deflation according to changing demand for money, not a static amount of money, itself. As Mises put it:

- In theoretical investigation there is only one meaning that can rationally be attached to the expression Inflation: an increase in the quantity of money (in the broader sense of the term, so as to include fiduciary media as well), that is not offset by a corresponding increase in the need for money (again in the broader sense of the term), so that a fall in the objective exchange-value of money must occur.[47]

Rothbard also objected to any concern over the fact that prices in general fell sharply during the entire period. They fell from the end of the Civil War until 1879. Friedman and Schwartz estimated that prices in general fell from 1869 to 1879 by 3.8 percent per annum. They blamed this on deflation, which most economists agree is even more devastating than inflation, but Rothbard, again, asserted that deflation was good, even desirable. When a government imposes a monopoly currency, like a gold standard, and the banking system therefore cannot increase the money supply in response to demand, any healthy economic growth can cause production and economic growth to happen so fast that there is not enough money to keep up with it. In effect, demand for money (to match the new wealth of goods and services) will increase far faster than supply. This spiraling deflation, Rothbard asserted, was actually a good thing.

- Prices will fall, and the consequences will be not depression or stagnation, but prosperity (since costs are falling, too) economic growth, and the spread of the increased living standard to all the consumers. The analogous "great depression" in England in this period was also a myth for the same reasons.[46]

Rothbard's argument, therefore, was that while incomes fell in dollars, the dollars bought more, so incomes were actually increasing, in real terms.

Accompanying the overall growth in real prosperity was a marked shift in consumption from necessities to luxuries: by 1885, 'more houses were being built, twice as much tea was being consumed, and even the working classes were eating imported meat, oranges, and dairy produce in quantities unprecedented'. The change in working class incomes and tastes was symbolized by 'the spectacular development of the department store and the chain store'.

Prices certainly fell, but almost every other index of economic activity - output of coal and pig iron, tonnage of ships built, consumption of raw wool and cotton, import and export figures, shipping entries and clearances, railway freight clearances, joint-stock company formations, trading profits, consumption per head of wheat, meat, tea, beer, and tobacco - all of these showed an upward trend.[48]

Most economists object to this interpretation, arguing that increasing cost of money causes malinvestment, distorting and redistributing wealth in exactly the same (but opposite) sense that inflation does. In this case, investors are punished, because nominal revenues and prices fall, but their investment remains the same size. Likewise, a home buyer quickly finds himself "underwater", because the buying price of the house remains the same, but both his nominal income and the price of the house plummets[49]. Certain branches of economic activity were indeed depressed between 1873 and 1896; in Britain these included foreign trade prior to 1875, agriculture in the late 1870s, and (as a result of increased foreign competitiveness) 'basic industries' such as the iron industry beginning in the 1880s. These troubled sectors of the economy were a source of increased structural unemployment and of 'continuous ululations of business people' inspiring calls for 'reciprocity' and 'fair trade' and provoking various royal and parliamentary inquiries. Britain and other gold standard nations were also far from being immune to genuine cyclical downturns, sometimes lasting several years and interrupting the otherwise positive trend of per-capita real income.

However, a large part at least of the deflation commencing in the 1870s was a reflection of unprecedented advances in factor productivity. Real unit production costs for most final goods dropped steadily throughout the 19th century, and especially from 1873 to 1896. At no previous time had there been an equivalent 'harvest of [technological] advances...so general in their application and so radical in their implications'. That is why, notwithstanding the dire predictions of many eminent economists, Britain did not end up paralyzed by strikes and lock-outs. Falling prices did not mean falling money wages. Instead of inspiring large numbers of workers to go on strike, falling prices were inspiring them to go shopping.[50]

See also

- List of recessions in the United States

- Economic history

- Kondratiev wave

- New Imperialism

- Second Industrial Revolution

- Panic of 1893

References

- ^ Rosenberg, Hans (1943). "Political and Social Consequences of the Great Depression of 1873-1896 in Central Europe". The Economic History Review. 13 (Blackwell Publishing) (1/2): 58–73. doi:10.1111/j.1468-0289.1943.tb01613.x. http://www.jstor.org/stable/2590515.

- ^ Musson, A.E. (1959). "The Great Depression in Britain, 1873-1896: A Reappraisal". The Journal of Economic History (Cambridge University Press) 19 (2): 199–228. http://www.jstor.org/stable/2114975.

- ^ Capie, Forrest; Wood, Geoffrey (1997). "Great Depression of 1873–1896". In Glasner, David; Cooley, Thomas F.. Business cycles and depressions: an encyclopedia. New York: Garland Publishing. pp. 148–49. ISBN 0824009444.

- ^ History of Economic Downturns in the US -- But Now You Know

- ^ a b c "Business Cycle Expansions and Contractions". National Bureau of Economic Research. http://www.nber.org/cycles/cyclesmain.html. Retrieved January 4, 2009.

- ^ Fels, Rendigs (1949). "The Long-Wave Depression, 1873-97". The Review of Economics and Statistics (The MIT Press) 31 (1): 69–73. doi:10.2307/1927196. JSTOR 1927196.

- ^ The Long Depression of 1873: Parallels and Comparisons. Are we Missing Economic Information from an Important Piece of American Financial History? http://www.mybudget360.com/finance-investing-the-long-depression-of-1873-parallels-and-comparisons-are-we-missing-economic-information-from-an-important-piece-of-american-financial-history/

- ^ Rothbard (2002), 164

- ^ a b c d e f g h i j k David Glasner, Thomas F. Cooley (1997). "Crisis of 1873". Business Cycles and Depressions: An Encyclopedia. Taylor & Francis. ISBN 0824009444.

- ^ a b Ron Chernow (1998). Titan. New York: Vintage Books. p. 160. ISBN 1-4000-7730-3.

- ^ a b Eric Hobsbawm (1989). The Age of Empire (1875–1914). New York: Vintage Books. p. 35. ISBN 0-679-72175-4.

- ^ a b c d Eric Hobsbawm (1989). The Age of Empire (1875-1914). New York: Vintage Books. p. 36. ISBN 0-679-72175-4.

- ^ a b Eric Foner (2002). Reconstruction: America's unfinished revolution, 1863–1877. HarperCollins. pp. 535. ISBN 0060937165.

- ^ Eric Hobsbawm (1989). The Age of Empire (1875–1914). New York: Vintage Books. p. 37. ISBN 0-679-72175-4.

- ^ Andrew Tylecote (1993). The long wave in the world economy. Routledge. p. 12. ISBN 0415036909.

- ^ Paul Kennedy (1989). The Rise and Fall of the Great Powers. Fontana Press. p. 219.

- ^ a b France and the Economic development of Europe (1800-1914). Routledge. 2000. p. 320. ISBN 0415190118.

- ^ a b c d France and the Economic development of Europe (1800-1914). Routledge. 2000. pp. 70–71. ISBN 0415190118.

- ^ a b c d e f g h i j David Glasner, Thomas F. Cooley (1997). "Depression of 1882-1885". Business Cycles and Depressions: An Encyclopedia. Taylor & Francis. ISBN 0824009444.

- ^ a b France and the Economic development of Europe (1800-1914). Routledge. 2000. p. 457. ISBN 0415190118.

- ^ David Glasner, Thomas F. Cooley (1997). "Business cycles in Russia (1700-1914)". Business Cycles and Depressions: An Encyclopedia. Taylor & Francis. ISBN 0824009444.

- ^ a b c d e f g h David Glasner, Thomas F. Cooley (1997). "Depression of 1873-1879". Business Cycles and Depressions: An Encyclopedia. Taylor & Francis. ISBN 0824009444.

- ^ Fels, Rendigs (1949). "The Long-Wave Depression, 1873-79". The Review of Economics and Statistics 31 (1): 69–73. doi:10.2307/1927196. JSTOR 1927196.

- ^ Milton Friedman, Anna Jacobson Schwartz. A monetary history of the United States, 1867-1960. Princeton University Press, 1971. p. 37

- ^ "United States Census". http://www2.census.gov/prod2/statcomp/documents/HistoricalStatisticsoftheUnitedStates1789-1945.pdf. Retrieved 07-19-2010. If the census figures are accurate, it is 17.83 percent.

- ^ a b c d Philip Mark Katz (1998). Appomattox to Montmartre: Americans and the Paris Commune. Harvard University Press. p. 167. ISBN 0674323483.

- ^ The Cambridge Economic History of the United States. Cambridge University Press. 2000. p. 223. ISBN 0521553075.

- ^ a b Eric Foner (2002). Reconstruction: America's unfinished revolution, 1863-1877. HarperCollins. pp. 531–532. ISBN 0060937165.

- ^ a b Nevins, Allan, Hamilton Fish: The Inner History of the Grant Administration (1936) online edition 2:811

- ^ France and the Economic development of Europe (1800-1914). Routledge. 2000. pp. 38–39. ISBN 0415190118.

- ^ a b France and the Economic development of Europe (1800-1914). Routledge. 2000. p. 39. ISBN 0415190118.

- ^ a b France and the Economic development of Europe (1800-1914). Routledge. 2000. p. 40. ISBN 0415190118.

- ^ The Reader's companion to American history. Houghton Mifflin Harcourt. 1991. ISBN 0395513723.

- ^ Eric Hobsbawm (1989). The Age of Empire (1875-1914). New York: Vintage Books. p. 50. ISBN 0-679-72175-4.

- ^ a b Eric Foner (2002). Reconstruction: America's unfinished revolution, 1863-1877. HarperCollins. p. 522. ISBN 0060937165.

- ^ Eric Hobsbawm (1989). The Age of Empire (1875-1914). New York: Vintage Books. p. 45. ISBN 0-679-72175-4.

- ^ Hannah Arendt (1973). The Origins of Totalitarianism. Houghton Mifflin Harcourt. p. 137. ISBN 0156701537.

- ^ Fels, Rendigs (1951). "American Business Cycles, 1865–79". The American Economic Review (American Economic Association) 41 (3): 325–349. http://www.jstor.org/stable/1802106.

- ^ Davis, Joseph (2006). "An Improved Annual Chronology of U.S.; Business Cycles since the 1790s". The Journal of Economic History 66 (1): 103–21.

- ^ Rothbard (2002), 154

- ^ Rothbard (2002), 161

- ^ David Glasner, Thomas F. Cooley (1997). "Debt-deflation theory". Business Cycles and Depressions: An Encyclopedia. Taylor & Francis. ISBN 0824009444.

- ^ Wells, David A. (1890). Recent Economic Changes and Their Effect on Production and Distribution of Wealth and Well-Being of Society. New York: D. Appleton and Co.. ISBN 0543724743. http://books.google.com/?id=2V3qF4MWh_wC&printsec=frontcover&dq=RECENT+ECONOMIC+CHANGES+AND+THEIR+EFFECT+ON+DISTRIBUTION+OF+WEALTH+AND+WELL+BEING+OF+SOCIETY+WELLS#v=onepage&q&f=false.

- ^ The Crime of 1873, bit Milton Friedman http://www.unc.edu/~salemi/Econ006/Friedman_Crime_1873.pdf

- ^ Friedman, Schwartz. A Monetary History of the United States: 1867-1960.

- ^ a b Murray N. Rothbard. "A History of Money and Banking in the United States: The Colonial Era to World War II" (pdf), The War of 1812 and its Aftermath, p.145, 153-156.

- ^ The Theory of Money and Credit, Mises (1912, [1981], p. 272)

- ^ A.E. Musson. "The Great Depression in Britain, 1873–1896: a Reappraisal", The Journal of Economic History (1959), 19: 199-228

- ^ Why Deflation is Bad...for You, Private Property, and Capitalism -- But Now You Know.net

- ^ George Selgin. "Less Than Zero - The Case for a Falling Price Level in a Growing Economy", The Institute of Economic Affairs, 1997, p.49-53. Referenced 2011-01-15.

Sources

- Rothbard, Murray A History of Money and banking in the United States: The Colonial Era to world War II(2002). The Ludwig Von Mises Institute.

Recessions in the United States Categories:- Economic history

- Recessions

- Modern Europe

- 19th century in economics

- 1870s economic history

- 1873 in economics

Wikimedia Foundation. 2010.