- Gold standard

-

For other uses, see Gold standard (disambiguation).

Under a gold standard, paper notes are convertible into pre-set, fixed quantities of gold.

Under a gold standard, paper notes are convertible into pre-set, fixed quantities of gold.

The gold standard is a monetary system in which the standard economic unit of account is a fixed mass of gold. There are distinct kinds of gold standard. First, the gold specie standard is a system in which the monetary unit is associated with circulating gold coins, or with the unit of value defined in terms of one particular circulating gold coin in conjunction with subsidiary coinage made from a lesser valuable metal.

Similarly, the gold exchange standard typically involves the circulation of only coins made of silver or other metals, but where the authorities guarantee a fixed exchange rate with another country that is on the gold standard. This creates a de facto gold standard, in that the value of the silver coins has a fixed external value in terms of gold that is independent of the inherent silver value. Finally, the gold bullion standard is a system in which gold coins do not circulate, but in which the authorities have agreed to sell gold bullion on demand at a fixed price in exchange for the circulating currency.

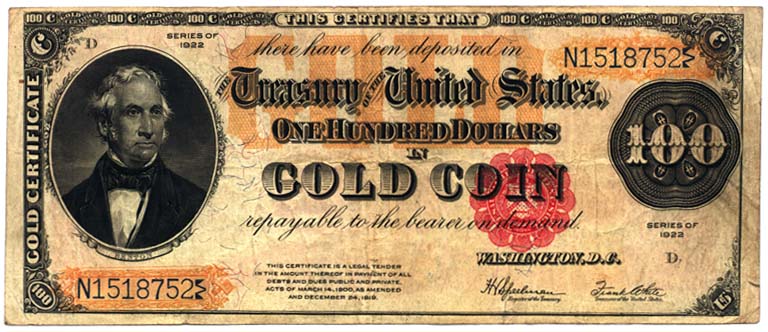

Gold certificates were used as paper currency in the United States from 1882 to 1933. These certificates were freely convertible into gold coins.

Gold certificates were used as paper currency in the United States from 1882 to 1933. These certificates were freely convertible into gold coins.History

Beginnings

The gold specie standard was not designed, but rather arose out of a general acceptance that gold was useful as a universal currency.[1] When commodities compete for the role of money, the one that over time loses the least value, takes on the role.[2] The use of gold as money dates back thousands of years and the first known gold coins were minted in the kingdom of Lydia in Asia Minor around 610 BC. The first coins minted in China are thought to date around 600 BC.[3] During the Middle Ages, the Byzantine gold Solidus, commonly known as the Bezant, circulated throughout Europe and the Mediterranean. But as the Byzantine Empire's economic influence declined, the European world tended to see silver, rather than gold, as the currency of choice, leading to the development of a silver standard. Silver pennies, based on the Roman Denarius, became the staple coin of Britain around the time of King Offa, circa AD 796, and similar coins, including Italian denari, French deniers, and Spanish dineros circulated throughout Europe. Following the Spanish discovery of great silver deposits at Potosí and in Mexico during the 16th century, international trade came to depend on coins such as the Spanish dollar, Maria Theresa thaler, and, in the 1870s, the United States Trade dollar.

In modern times the British West Indies was one of the first regions to adopt a gold specie standard. Following Queen Anne's proclamation of 1704, the British West Indies gold standard was a de facto gold standard based on the Spanish gold doubloon coin. In the year 1717, master of the Royal Mint Sir Isaac Newton established a new mint ratio between silver and gold that had the effect of driving silver out of circulation and putting Britain on a gold standard. However, only in 1821, following the introduction of the gold sovereign coin by the new Royal Mint at Tower Hill in the year 1816, was the United Kingdom formally put on a gold specie standard, the first of the great industrial powers. Soon to follow was Canada in 1853, Newfoundland in 1865, and the USA and Germany de jure in 1873. The USA used the Eagle as their unit, and Germany introduced the new gold mark, while Canada adopted a dual system based on both the American Gold Eagle and the British Gold Sovereign.

Australia and New Zealand adopted the British gold standard, as did the British West Indies, while Newfoundland was the only British Empire territory to introduce its own gold coin as a standard. Royal Mint branches were established in Sydney, New South Wales, Melbourne, Victoria, and Perth, Western Australia for the purpose of minting gold sovereigns from Australia's rich gold deposits.

The crisis of silver currency and bank notes (1750–1870)

In the late 18th century, wars and trade with China, which sold to Europe but had little use for European goods, drained silver from the economies of Western Europe and the United States. Coins were struck in smaller and smaller numbers, and there was a proliferation of bank and stock notes used as money.

England

In the 1790s, England, suffering a massive shortage of silver coinage, ceased to mint larger silver coins and issued "token" silver coins and overstruck foreign coins. With the end of the Napoleonic Wars, England began a massive recoinage programme that created standard gold sovereigns and circulating crowns and half-crowns, and eventually copper farthings in 1821. The recoinage of silver in England after a long drought produced a burst of coins: England struck nearly 40 million shillings between 1816 and 1820, 17 million half crowns and 1.3 million silver crowns. The 1819 Act for the Resumption of Cash Payments set 1823 as the date for resumption of convertibility, reached instead by 1821. Throughout the 1820s, small notes were issued by regional banks, which were finally restricted in 1826, while the Bank of England was allowed to set up regional branches. In 1833, however, the Bank of England notes were made legal tender, and redemption by other banks was discouraged. In 1844 the Bank Charter Act established that Bank of England Notes, fully backed by gold, were the legal standard. According to the strict interpretation of the gold standard, this 1844 act marks the establishment of a full gold standard for British money.

US

The US adopted a silver standard based on the Spanish milled dollar in 1785. This was codified in the 1792 Mint and Coinage Act, and by the Federal Government's use of the "Bank of the United States" to hold its reserves, as well as establishing a fixed ratio of gold to the US dollar. This was, in effect, a derivative silver standard, since the bank was not required to keep silver to back all of its currency. This began a long series of attempts for America to create a bi-metallic standard for the US Dollar, which would continue until the 1920s. Gold and silver coins were legal tender, including the Spanish real, a silver coin struck in the Western Hemisphere. Because of the huge debt taken on by the US Federal Government to finance the Revolutionary War, silver coins struck by the government left circulation, and in 1806 President Jefferson suspended the minting of silver coins. The US Treasury was put on a strict hard-money standard, doing business only in gold or silver coin as part of the Independent Treasury Act of 1848, which legally separated the accounts of the Federal Government from the banking system. However the fixed rate of gold to silver overvalued silver in relation to the demand for gold to trade or borrow from England. The drain of gold in favor of silver led to the search for gold, including the California Gold Rush of 1849. Following Gresham's law, silver poured into the US, which traded with other silver nations, and gold moved out. In 1853, the US reduced the silver weight of coins, to keep them in circulation, and in 1857 removed legal tender status from foreign coinage.

In 1857 the final crisis of the free banking era of international finance began, as American banks suspended payment in silver, rippling through the very young international financial system of central banks. In the United States this collapse was a contributory factor[citation needed] in the American Civil War (1861–1865), and in 1861 the US government suspended payment in gold and silver, effectively ending the attempts to form a silver standard basis for the dollar.

International

Through the 1860–1871 period, various attempts to resurrect bi-metallic standards were made, including one based on the gold and silver franc; however, with the rapid influx of silver from new deposits, the expectation of scarcity of silver ended.

The interaction between central banking and currency basis formed the primary source of monetary instability during this period. The combination that produced economic stability was a restriction of supply of new notes, a government monopoly on the issuance of notes directly and, indirectly, a central bank and a single unit of value. Attempts to avoid these conditions produced periodic monetary crises: as notes devalued; or silver ceased to circulate as a store of value; or there was a depression as governments, demanding specie as payment, drained the circulating medium out of the economy. At the same time, there was a dramatically expanded need for credit, and large banks were being chartered in various states, including, by 1872, Japan. The need for a solid basis in monetary affairs would produce a rapid acceptance of the gold standard in the period that followed.

Japan

By way of example, and following Germany's decision after the Franco-Prussian War (1870-1871) to extract reparations to facilitate a move to the gold standard, Japan gained the needed reserves after the Sino-Japanese War of 1894–1895. Whether the gold standard provided a government sufficient bona fides when it sought to borrow abroad is debated. For Japan, moving to gold was considered vital to gain access to Western capital markets.[4]

The gold exchange standard (1870–1914)

Towards the end of the 19th century, some of the remaining silver standard countries began to peg their silver coin units to the gold standards of the United Kingdom or the USA. In 1898, British India pegged the silver rupee to the pound sterling at a fixed rate of 1s 4d, while in 1906, the Straits Settlements adopted a gold exchange standard against the pound sterling with the silver Straits dollar being fixed at 2s 4d.

At the turn of the century, the Philippines pegged the silver Peso/dollar to the US dollar at 50 cents. A similar pegging at 50 cents occurred at around the same time with the silver Peso of Mexico and the silver Yen of Japan. When Siam adopted a gold exchange standard in 1908, this left only China and Hong Kong on the silver standard.

Adopting the gold standard many European nations changed the name of their currency from Rixdaler (Sweden and Danemark) or Gulden (Austria-Hungary) to Crown, since the former ones were traditionally associated with silver coins and the latter with gold coins.

Impact of World War I (1914–25)

Governments faced with the need to fund high levels of expenditure, but with limited sources of tax revenue, suspended convertibility of currency into gold on a number of occasions in the 19th century. The British government suspended convertibility (that is to say, it went off the gold standard) during the Napoleonic wars and the US government during the US Civil War. In both cases, convertibility was resumed after the war.[citation needed] The real test, however, came in the form of World War I, a test "it failed utterly" according to economist Richard Lipsey.[1]

In order to finance the costs of war, most belligerent countries went off the gold standard during the war, and suffered significant inflation. Because inflation levels varied between states, when they returned to the standard after the war at price determined by themselves (some, for example, chose to enter at pre-war prices), some countries' goods were undervalued and some overvalued.[1] Ultimately, the system as it stood could not deal quickly enough with the large deficits and surpluses created in the balance of payments; this has previously been attributed to increasing rigidity of wages (particularly in terms of wage cuts) brought about by the advent of unionized labor, but is now more likely to be thought of as an inherent fault with the system which came to light under the pressures of war and rapid technological change. In any case, prices had not reached equilibrium by the time of the Great Depression, which served only to kill it off completely.[1] For example, Germany had gone off the gold standard in 1914, and could not effectively return to it as Germany had lost much of its remaining gold reserves in reparations. The German central bank issued unbacked marks virtually without limit to buy foreign currency for further reparations and to support workers during the Occupation of the Ruhr finally leading to hyperinflation in the 1920s.

The gold bullion standard and the decline of the gold standard (1925–31)

William McKinley ran for president on the basis of the gold standard.

William McKinley ran for president on the basis of the gold standard.The gold specie standard ended in the United Kingdom and the rest of the British Empire at the outbreak of World War I. Treasury notes replaced the circulation of the gold sovereigns and gold half sovereigns. However, legally, the gold specie standard was not repealed. The end of the gold standard was successfully effected by appeals to patriotism when somebody would request the Bank of England to redeem their paper money for gold specie. It was only in the year 1925 when Britain returned to the gold standard in conjunction with Australia and South Africa that the gold specie standard was officially ended.

The British Gold Standard Act 1925 both introduced the gold bullion standard and simultaneously repealed the gold specie standard. The new gold bullion standard did not envisage any return to the circulation of gold specie coins. Instead, the law compelled the authorities to sell gold bullion on demand at a fixed price. This gold bullion standard lasted until 1931.[citation needed] On September 19, 1931, the United Kingdom left the revised gold standard,[5] forced to suspend the gold bullion standard due to large outflows of gold across the Atlantic Ocean. The British benefited from the departure. They could now use monetary policy to stimulate the economy through the lowering of interest rates. Australia and New Zealand had already been forced off the gold standard by the same pressures connected with the Great Depression, and Canada quickly followed suit with the United Kingdom.

Depression and World War II (1932–46)

Prolongation of the Great Depression

Some economic historians, such as American professor Barry Eichengreen, blame the gold standard of the 1920s for prolonging the Great Depression.[6] Others including Federal Reserve Chairman Ben Bernanke and Nobel Prize winning economist Milton Friedman place some blame at the feet of the Federal Reserve.[7][8] The gold standard limited the flexibility of central banks' monetary policy by limiting their ability to expand the money supply, and thus their ability to lower interest rates. In the US, the Federal Reserve was required by law to have 40% gold backing of its Federal Reserve demand notes, and thus, could not expand the money supply beyond what was allowed by the gold reserves held in their vaults.[9]

In the early 1930s, the Federal Reserve defended the fixed price of dollars in respect to the gold standard by raising interest rates, trying to increase the demand for dollars. Its commitment and adherence to the gold standard explain why the U.S. did not engage in expansionary monetary policy. To compete in the international economy, the U.S. maintained high interest rates. This helped attract international investors who bought foreign assets with gold. Higher interest rates intensified the deflationary pressure on the dollar and reduced investment in U.S. banks. Commercial banks also converted Federal Reserve Notes to gold in 1931, reducing the Federal Reserve's gold reserves, and forcing a corresponding reduction in the amount of Federal Reserve Notes in circulation.[10] This speculative attack on the dollar created a panic in the U.S. banking system. Fearing imminent devaluation of the dollar, many foreign and domestic depositors withdrew funds from U.S. banks to convert them into gold or other assets.[10]

The forced contraction of the money supply caused by people removing funds from the banking system during the bank panics resulted in deflation; and even as nominal interest rates dropped, inflation-adjusted real interest rates remained high, rewarding those that held onto money instead of spending it, causing a further slowdown in the economy.[11] Recovery in the United States was slower than in Britain, in part due to Congressional reluctance to abandon the gold standard and float the U.S. currency as Britain had done.[12]

Congress passed the Gold Reserve Act on 30 January 1934; the measure nationalized all gold by ordering the Federal Reserve banks to turn over their supply to the U.S. Treasury. In return the banks received gold certificates to be used as reserves against deposits and Federal Reserve notes. The act also authorized the president to devalue the gold dollar so that it would have no more than 60 percent of its existing weight. Under this authority the president, on 31 January 1934, fixed the value of the gold dollar at 59.06 cents.

British hesitate to return to gold standard

During the 1939–1942 period, the UK depleted much of its gold stock in purchases of munitions and weaponry on a "cash-and-carry" basis from the U.S. and other nations.[citation needed] This depletion of the UK's reserve convinced Winston Churchill of the impracticality of returning to a pre-war style gold standard.

John Maynard Keynes, who had argued against such a gold standard, proposed to put the power to print money in the hands of the privately owned Bank of England. Keynes, in warning about the menaces of inflation, said "By a continuous process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method, they not only confiscate, but they confiscate arbitrarily; and while the process impoverishes many, it actually enriches some".[13]

Quite possibly because of this, the 1944 Bretton Woods Agreement established the International Monetary Fund and an international monetary system based on convertibility of the various national currencies into a U.S. dollar that was in turn convertible into gold.

Post-war international gold-dollar standard (1946–1971)

Main article: Bretton Woods systemAfter the Second World War, a system similar to a Gold Standard and sometimes described as a "gold exchange standard" was established by the Bretton Woods Agreements. Under this system, many countries fixed their exchange rates relative to the U.S. dollar. The U.S. promised to fix the price of gold at approximately $35 per ounce. Implicitly, then, all currencies pegged to the dollar also had a fixed value in terms of gold.[1] Under the administration of the French President Charles de Gaulle up to 1970, France reduced its dollar reserves, trading them for gold from the U.S. government, thereby reducing U.S. economic influence abroad. This, along with the fiscal strain of federal expenditures for the Vietnam War and persistent balance of payments deficits, led President Richard Nixon to end the direct convertibility of the dollar to gold on August 15, 1971, resulting in the system's breakdown (the "Nixon Shock").

Theory

Commodity money is inconvenient to store and transport. Further, it does not allow a government to manipulate or restrict the flow of commerce within its dominion with the same ease that a fiat currency does. As such, commodity money gave way to representative money, and gold and other specie were retained as its backing.

Gold was a common form of money due to its rarity, durability, divisibility, fungibility, and ease of identification,[4] often in conjunction with silver. Silver was typically the main circulating medium, with gold as the metal of monetary reserve.

The gold standard variously specified how the gold backing would be implemented, including the amount of specie per currency unit. The currency itself is just paper and so has no intrinsic value, but is accepted by traders because it can be redeemed any time for the equivalent specie. A U.S. silver certificate, for example, could be redeemed for an actual piece of silver.

Representative money and the gold standard protect citizens from hyperinflation and other abuses of monetary policy, as were seen in some countries during the Great Depression. However, they were not without their problems and critics, and so were partially abandoned via the international adoption of the Bretton Woods System. That system eventually collapsed in 1971, at which time nearly all nations had switched to full fiat money.

According to Keynesian analysis, the earliness with which a country left the gold standard reliably predicted its economic recovery from the great depression. For example, Great Britain and Scandinavia, which left the gold standard in 1931, recovered much earlier than France and Belgium, which remained on gold much longer. Countries such as China, which had a silver standard, almost avoided the depression entirely. The connection between leaving the gold standard as a strong predictor of that country's severity of its depression and the length of time of its recovery has been shown to be consistent for dozens of countries, including developing countries. This may explain why the experience and length of the depression differed between national economies.[14]

Differing definitions

A 100%-reserve gold standard, or a full gold standard, exists when a monetary authority holds sufficient gold to convert all of the representative money it has issued into gold at the promised exchange rate. It is sometimes referred to as the gold specie standard to more easily identify it from other forms of the gold standard that have existed at various times. Opponents of a 100%-reserve standard consider a 100%-reserve standard difficult to implement, saying that the quantity of gold in the world is too small to sustain current worldwide economic activity at current gold prices; implementation would entail a many-fold increase in the price of gold.[citation needed] However, proponents of the gold standard have said that any amount of gold can serve as the reserve: "Once a money is established, any stock of money becomes compatible with any amount of employment and real income."[15] According to them the prices of goods and services will adjust to the supply of gold.[16]

In an international gold-standard system (which is necessarily based on an internal gold standard in the countries concerned),[17] gold or a currency that is convertible into gold at a fixed price is used as a means of making international payments. Under such a system, when exchange rates rise above or fall below the fixed mint rate by more than the cost of shipping gold from one country to another, large inflows or outflows occur until the rates return to the official level. International gold standards often limit which entities have the right to redeem currency for gold. Under the Bretton Woods system, these were called "SDRs" for Special Drawing Rights.[citation needed]

Advantages

- Long-term price stability has been described as the great virtue of the gold standard.[18] Under the gold standard, high levels of inflation are rare, and hyperinflation is nearly impossible as the money supply can only grow at the rate that the gold supply increases.[19] Economy-wide price increases caused by ever-increasing amounts of currency chasing a constant supply of goods are rare,[19] as gold supply for monetary use is limited by the available gold that can be minted into coin.[19] High levels of inflation under a gold standard are usually seen only when warfare destroys a large part of the economy, reducing the production of goods, or when a major new source of gold becomes available.[19] In the U.S. one of those periods of warfare was the Civil War, which destroyed the economy of the South,[20] while the California Gold Rush made large amounts of gold available for minting.[21]

- The gold standard limits the power of governments to inflate prices through excessive issuance of paper currency.[19] It provides fixed international exchange rates between those countries that have adopted it, and thus reduces uncertainty in international trade.[19] Historically, imbalances between price levels in different countries would be partly or wholly offset by an automatic balance-of-payment adjustment mechanism called the "price specie flow mechanism."[19]

- The gold standard makes chronic deficit spending by governments more difficult, as it prevents governments from inflating away the real value of their debts.[22] A central bank cannot be an unlimited buyer of last resort of government debt. A central bank could not create unlimited quantities of money at will, as there is a limited supply of gold.[19]

- Deflation rewards savers.[23][24]

Disadvantages

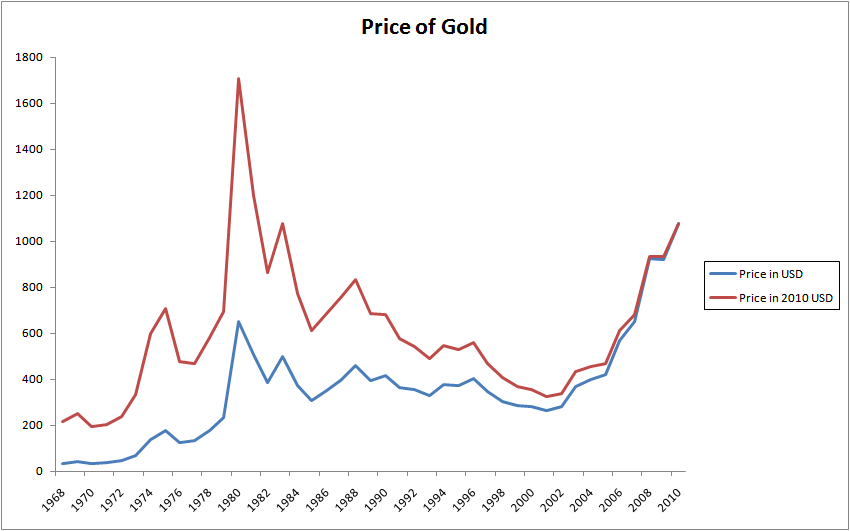

Gold prices (US$ per ounce) from 1968 to 2010, in nominal US$ and inflation adjusted US$.

Gold prices (US$ per ounce) from 1968 to 2010, in nominal US$ and inflation adjusted US$.- The total amount of gold that has ever been mined has been estimated at around 142,000 metric tons.[25] This is less than the value of circulating money in the U.S. alone, where more than $8.3 trillion is in circulation or in deposit (M2).[26] Therefore, a return to the gold standard, if also combined with a mandated end to fractional reserve banking, would result in a significant increase in the current value of gold, which may limit its use in current applications.[27]

- Deflation punishes debtors.[28][29] Real debt burdens therefore rise, causing borrowers to cut spending to service their debts or to default. Lenders become wealthier, but may choose to save some of their additional wealth rather than spending it all.[30] The overall amount of expenditure is therefore likely to fall.[30]

- Mainstream economists believe that economic recessions can be largely mitigated by increasing money supply during economic downturns.[31] Following a gold standard would mean that the amount of money would be determined by the supply of gold, and hence monetary policy could no longer be used to stabilize the economy in times of economic recession.[32] Such reason is often employed to partially blame the gold standard for the Great Depression, citing that the Federal Reserve couldn't expand credit enough to offset the deflationary forces at work in the market.[33]

- Monetary policy would essentially be determined by the rate of gold production.[34] Fluctuations in the amount of gold that is mined could cause inflation if there is an increase, or deflation if there is a decrease.[34][35] Some hold the view that this contributed to the severity and length of the Great Depression as the gold standard forced the central banks to keep monetary policy too tight, creating deflation.[27][36]

- The unequal distribution of gold as a natural resource makes the gold standard much more advantageous in terms of cost and international economic empowerment for some countries[37] (such as the Republic of South Africa which possess an estimated half of all un-mined reserves[38]), than for others (countries with no reserves of gold ore).

- Although the gold standard gives long-run price stability, it does in the short run bring high price volatility.[35][39] It has been argued by, among others, Anna Schwartz that this kind of instability in short-term price levels can lead to financial instability as lenders and borrowers become uncertain about the value of debt.[40]

- James Hamilton contended that the gold standard may be susceptible to speculative attacks when a government's financial position appears weak, although others contend that this very threat discourages governments' engaging in risky policy (see Moral Hazard).[36] For example, some believe that the United States was forced to raise its interest rates in the middle of the Great Depression to defend the credibility of its currency after unusually easy credit policies in the 1920s.[36]

- If a country wanted to devalue its currency, a gold standard would generally produce sharper changes than the smooth declines seen in fiat currencies, depending on the method of devaluation.[41]

- Most economists favor a low, positive rate of inflation. Partly this reflects fear of deflationary shocks, but primarily because they believe that central banks still have some role to play in dampening fluctuations in output and unemployment. Central banks can more safely play that role when a positive rate of inflation gives them room to tighten money growth without inducing price declines.[42]

- It is difficult to manipulate a gold standard to tailor to an economy’s demand for money, providing practical constraints against the measures that central banks might otherwise use to respond to economic crises.[43]

Advocates of a renewed gold standard

The return to the gold standard is supported by many followers of the Austrian School of Economics, Objectivists, free-market libertarians[44] and, in the United States, by strict constitutionalists largely because they object to the role of the government in issuing fiat currency through central banks. A significant number of gold-standard advocates also call for a mandated end to fractional-reserve banking.[citation needed]

Few politicians[45] today advocate a return to the gold standard, other than adherents of the Austrian school and some supply-siders. However, some prominent economists have expressed sympathy with a hard-currency basis, and have argued against politically-controlled fiat money, including former U.S. Federal Reserve Chairman Alan Greenspan (himself a former Objectivist), and macro-economist Robert Barro.[46] Greenspan famously argued the case for returning to a 'pure' gold standard in his 1966 paper "Gold and Economic Freedom", in which he described supporters of fiat currencies as "welfare statists" intent on using monetary policies to finance deficit spending.[47] Barro argues in favor of adopting some form of "monetary constitution" that will provide stability to monetary policy rather than allowing decisions about monetary policy to be made on the basis of politics, but suggests that what form this constitution takes—for example, a gold standard, some other commodity-based standard, or a fiat currency with fixed rules for determining the quantity of money—is considerably less important.[46] U.S. Congressman Ron Paul has continually argued for the reinstatement of the gold standard, but is no longer a strict advocate, instead supporting a basket of commodities that emerges on the free markets.[48]

For the time being, the global monetary system continues to rely on the U.S. dollar as a reserve currency by which major transactions, such as the price of gold itself, are measured.[49] A host of alternatives has been suggested, including energy-based currencies, and market baskets of currencies or commodities, gold being one of the alternatives.

In 2001, Malaysian Prime Minister Mahathir bin Mohamad proposed a new currency that would be used initially for international trade among Muslim nations. The currency he proposed was called the Islamic gold dinar and it was defined as 4.25 grams of pure (24-carat) gold. Mahathir Mohamad promoted the concept on the basis of its economic merits as a stable unit of account and also as a political symbol to create greater unity between Islamic nations. The purported purpose of this move would be to reduce dependence on the United States dollar as a reserve currency, and to establish a non-debt-backed currency in accord with Islamic law against the charging of interest.[50] However, to date, Mahathir's proposed gold-dinar currency has failed to take hold.

In 2011, the legislature of the state of Utah passed a bill to accept federally-issued gold and silver coins as legal tender to pay taxes.[51][52] Similar legislation is under consideration in a number of other US states.

Gold as a reserve today

Main article: Gold reserveThe Swiss Franc was based on a 40% legal gold-reserve requirement from 1936, when it ended gold convertibility,[53] until 2000. Gold reserves are held in significant quantity by many nations as a means of defending their currency, and hedging against the U.S. Dollar, which forms the bulk of liquid currency reserves.

Both gold coins and gold bars are widely traded in liquid markets, and therefore still serve as a private store of wealth. Some privately issued currencies, such as digital gold currency, are backed by gold reserves.[citation needed]

In 1999, to protect the value of gold as a reserve, European Central Bankers signed the Washington Agreement on Gold, which stated that they would not allow gold leasing for speculative purposes, nor would they enter the market as sellers except for sales that had already been agreed upon.[citation needed]

See also

- A Program for Monetary Reform (1939) – The Gold Standard

- Bimetallism

- Coinage Act of 1792

- Coinage Act of 1873

- Federal Reserve System

- Full-reserve banking

- Gold as an investment

- Gold bug

- Gold Points

- Gold Reserve Act

- Representative money

- Silver standard

- Store of value

- The Great Deflation

- Latin Monetary Union

- International institutions

- Bank for International Settlements

- International Monetary Fund

- United Nations Monetary and Financial Conference

- World Bank

References

- ^ a b c d e Lipsey, Richard G. (1975). An introduction to positive economics (fourth ed.). Weidenfeld & Nicolson. pp. 683–702. ISBN 0297768999.

- ^ "the one with the lower depreciation rate emerges as commodity money"

- ^ 610 BC Lydians of Asia Minor invent coinage; shortly afterward it spreads to Greek cities in Asia Minor, then Greek islands, then Greek mainland, then rest of world

- ^ a b Metzler, Mark (2006). Lever of Empire: The International Gold Standard and the Crisis of Liberalism in Prewar Japan.. Berkeley: University of California Press. p. [1]. ISBN 0-520-24420-6.

- ^ Barry J. Eichengreen (15 September 2008). Globalizing capital: a history of the international monetary system. Princeton University Press. pp. 61–. ISBN 9780691139371. http://books.google.com/books?id=_iNqESd-9R0C&pg=PA61. Retrieved 23 November 2010.

- ^ Eichengreen, Barry (1992) Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. Preface.

- ^ Speech by Ben Bernanke to the Conference to Honor Milton Friedman at University of Chicago, November 8 2002.

- ^ WorldNetDaily, March 19 2008.

- ^ The original Federal Reserve Act provided for a note issue which was to be secured ... by a 40% reserve in gold

- ^ a b "FRB: Speech, Bernanke-Money, Gold, and the Great Depression -March 2, 2004". Federalreserve.gov. 2004-03-02. http://www.federalreserve.gov/boarddocs/speeches/2004/200403022/default.htm. Retrieved 2010-07-24.

- ^ "In the 1930s, the United States was in a situation that satisfied the conditions for a liquidity trap. Over 1929–1933 overnight rates fell to zero, and they remained on the floor through the 1930's."

- ^ The European Economy between Wars; Feinstein, Temin, and Toniolo

- ^ John Maynard Keynes Economic Consequences of the Peace, 1920.

- ^ Bernanke, Ben (March 2, 2004), "Remarks by Governor Ben S. Bernanke: Money, Gold and the Great Depression", At the H. Parker Willis Lecture in Economic Policy, Washington and Lee University, Lexington, Virginia.

- ^ Hoppe, Hans-Herman (1992). Mark Skousen. ed. Dissent on Keynes, A Critical Appraisal of Economics. pp. 199–223. http://mises.org/daily/2492#i2.

- ^ "Gold as Money: FAQ". Mises.org. Ludwig von Mises Institute. http://mises.org/Community/wikis/economics/gold-as-money-faq.aspx. Retrieved 12 August 2011.

- ^ The New Palgrave Dictionary of Economics, 2nd edition (2008), Vol.3, S.695

- ^ Bordo, Michael D. (2008). "Gold Standard". http://www.econlib.org/library/Enc/GoldStandard.html. The great virtue of the gold standard was that it assured long-term price stability.

- ^ a b c d e f g h "Advantages of the Gold Standard". The Gold Standard: Perspectives in the Austrian School. The Ludwig von Mises Institute. http://mises.org/books/goldstandard.pdf. Retrieved 9 January 2011.

- ^ The Economics of the Civil War the Union also experienced inflation as a result of deficit finance during the war; the consumer price index rose from 100 at the outset of the war to 175 by the end of 1865.

- ^ California Gold Rush from 1792 until 1847 cumulative U.S. production of gold was only about 37 tons. California’s production in 1849 alone exceeded this figure, and annual production from 1848 to 1857 averaged 76 tons. ... Soaring gold output from the California and Australia gold rushes is linked with a 30 percent increase in wholesale prices from 1850 through 1855.

- ^ "Gold and Economic Freedom" by Alan Greenspan

- ^ deflation rewards savers who hoard cash

- ^ http://208.106.154.79/story.aspx?82504cb2-de36-4934-bd4f-6912fbca58cc Deflation rewarded those who saved

- ^ Butterman, W.C.; Earle B. Amey III (2005) (PDF). Mineral Commodity Profiles—Gold. Reston, Virginia: United States Geological Survey. OCLC 62034878. http://pubs.usgs.gov/of/2002/of02-303/OFR_02-303.pdf. Retrieved 2008-11-12.[page needed]

- ^ "Money Stock and Debt Measures". Federal Reserve Board. 2008-03-13. http://www.federalreserve.gov/releases/h6/current/default.htm. Retrieved 2008-03-16.

- ^ a b Warburton, Clark (1966). "The Monetary Disequilibrium Hypothesis". Depression, Inflation, and Monetary Policy: Selected Papers, 1945–1953. Baltimore: Johns Hopkins University Press. pp. 25–35. OCLC 736401.

- ^ “Deflation hurts borrowers and rewards savers,” said Drew Matus, senior economist at Banc of America Securities-Merrill Lynch in New York, in a telephone interview. “If you do borrow right now, and we go through a period of deflation, your cost of borrowing just went through the roof.”

- ^ which in contrast rewards savers and penalizes debtors, and governments most of all, they being the largest debtors in the modern era.

- ^ a b http://www.economist.com/node/13610845 Inflation is bad, but deflation is worse

- ^ Mankiw, N. Gregory (2002). Macroeconomics (5th ed.). Worth. pp. 238–255. ISBN 0324171900.

- ^ Krugman, Paul. "The Gold Bug Variations". Slate.com. http://www.slate.com/id/1912/. Retrieved 2009-02-13.

- ^ Timberlake, Richard H. 2005. "Gold Standards and the Real Bills Doctrine in US Monetary Policy". Econ Journal Watch 2(2): 196–233. [2]

- ^ a b DeLong, Brad (1996-08-10). "Why Not the Gold Standard?". Berkeley, California: University of California, Berkeley. http://www.j-bradford-delong.net/Politics/whynotthegoldstandard.html. Retrieved 2008-09-25.

- ^ a b Bordo, Michael D. (2008). "Gold Standard". In David R. Henderson. Concise Encyclopedia of Economics. Indianapolis: Liberty Fund. ISBN 0-86597-666-X. OCLC 123350134. http://www.econlib.org/library/Enc/GoldStandard.html. Retrieved 2010-08-28.

- ^ a b c Hamilton, James D. (2005-12-12). "The gold standard and the Great Depression". Econbrowser. http://www.econbrowser.com/archives/2005/12/the_gold_standa.html. Retrieved 2008-11-12. See also Hamilton, James D. (April 1988). "Role of the International Gold Standard in Propagating the Great Depression". Contemporary Economic Policy 6 (2): 67–89. doi:10.1111/j.1465-7287.1988.tb00286.x. http://www3.interscience.wiley.com/journal/120017201/abstract. Retrieved 2008-11-12.

- ^ Goodman, George J.W., Paper Money, 1981, p.165-6

- ^ Gold. College of Natural Resources. University of California Berkeley

- ^ Michael D. Bordo, Robert Dittmar, and William T. Gavin "Gold, Fiat Money and Price Stability" May 2007 [3]

- ^ Bordo, Michael D.; Robert D. Dittmar, William T. Gavin (May 2007). "Gold, Fiat Money and Price Stability". Working Paper Series. Research Division - Federal Reserve Bank of St. Louis. http://research.stlouisfed.org/wp/2003/2003-014.pdf. Retrieved 27 august 2011.

- ^ McArdle, Megan (2007-09-04). "There's gold in them thar standards!". The Atlantic Monthly. http://meganmcardle.theatlantic.com/archives/2007/09/theres_gold_in_them_thar_stand.php. Retrieved 2008-11-12.

- ^ Hummel, Jeffrey Rogers. "Death and Taxes, Including Inflation: the Public versus Economists" (January 2007).[4] p.56

- ^ Demirgüç-Kunt, Asli; Enrica Detragiache (April 2005). "Cross-Country Empirical Studies of Systemic Bank Distress: A Survey". National Institute Economic Review 192 (1): 68–83. doi:10.1177/002795010519200108. ISSN 0027-9501. OCLC 90233776. http://ner.sagepub.com/cgi/reprint/192/1/68. Retrieved 2008-11-12.

- ^ "Time to Think about the Gold Standard? | Cato @ Liberty". Cato-at-liberty.org. 2009-03-12. http://www.cato-at-liberty.org/2009/03/12/time-to-think-about-the-gold-standard/. Retrieved 2010-07-24.

- ^ Paul, Ron; Lewis Lehrman (1982) (PDF). The case for gold: a minority report of the U.S. Gold Commission. Washington, D.C.: Cato Institute. p. 160. ISBN 0-932790-31-3. OCLC 8763972. http://www.mises.org/books/caseforgold.pdf. Retrieved 2008-11-12.

- ^ a b Salerno, Joseph T. (1982-09-09). "The Gold Standard: An Analysis of Some Recent Proposals". Cato Policy Analysis. Cato Institute. http://www.cato.org/pubs/pas/pa016.html. Retrieved 2009-03-23.

- ^ Greenspan, Alan (July 1966). "Gold and Economic Freedom". The Objectivist 5 (7). http://www.constitution.org/mon/greenspan_gold.htm. Retrieved 2008-10-16.

- ^ Channel: CNBC. Show: Squawk Box. Date: 11/13/2009. Interview with Ron Paul

- ^ Richard McGregor:Hu questions future role of US dollar. Financial Times, January 16 2011

- ^ al-'Amraawi, Muhammad; Al-Khammar al-Baqqaali, Ahmad Saabir, Al-Hussayn ibn Haashim, Abu Sayf Kharkhaash, Mubarak Sa'doun al-Mutawwa', Malik Abu Hamza Sezgin, Abdassamad Clarke and Asadullah Yate (2001-07-01). "Declaration of 'Ulama on the Gold Dinar". Islam i Dag. http://www.islamidag.dk/ulamaongold.html. Retrieved 2008-11-14.

- ^ Utah Considers Return to Gold, Silver Coins

- ^ Spillius, Alex (2011-03-18). "Tea Party legislation reveals anxiety at US direction under Barack Obama". The Daily Telegraph (London). http://www.telegraph.co.uk/news/worldnews/us-politics/8391504/Tea-Party-legislation-reveals-anxiety-at-US-direction-under-Barack-Obama.html.

- ^ MacEdo, Jorge Braga de; Eichengreen, Barry J; Reis, Jaime (1996). Currency convertibility: The gold standard and beyond. ISBN 9780415140577. http://books.google.com/?id=IqPMKv1h4uEC&pg=PA33&lpg=PA33&dq=switzerland+gold+convertibility+1926#v=onepage&q=switzerland%20gold%20convertibility%201926&f=false.

Further reading

- Gold Keeps Shining, 40 Years After Nixon Ended Gold Standard, an April 2011 radio and Internet feature story by the Special English service of the Voice of America.

- Bensel, Richard Franklin (2000). The political economy of American industrialization, 1877–1900. Cambridge: Cambridge University Press. ISBN 0-521-77604-X. OCLC 43552761.

- Eichengreen, Barry J.; Marc Flandreau (1997). The gold standard in theory and history. New York City: Routledge. ISBN 0-415-15061-2. OCLC 37743323.

- Bordo, Michael D. (1999). Gold standard and related regimes: collected essays. Cambridge: Cambridge University Press. ISBN 0-521-55006-8. OCLC 59422152.

- Bordo, Michael D; Anna Jacobson Schwartz and National Bureau of Economic Research (1984). A Retrospective on the classical gold standard, 1821–1931. Chicago: University of Chicago Press. ISBN 0-226-06590-1. OCLC 10559587.

- Officer, Lawrence H. (2007). Between the Dollar-Sterling Gold Points: Exchange Rates, Parity and Market Behavior. Chicago: Cambridge University Press. ISBN 0-521-03821-9. OCLC 124025586.

- Eichengreen, Barry J. (1995). Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. New York City: Oxford University Press. ISBN 0-19-510113-8. OCLC 34383450.

- Einaudi, Luca (2001). Money and politics: European monetary unification and the international gold standard (1865–1873). Oxford: Oxford University Press. ISBN 0-19-924366-2. OCLC 45556225.

- Roberts, Mark A (March 1995). "Keynes, the Liquidity Trap and the Gold Standard: A Possible Application of the Rational Expectations Hypothesis". The Manchester School of Economic & Social Studies (Blackwell Publishing) 61 (1): 82–92. doi:10.1111/j.1467-9957.1995.tb00270.x.

- Thompson, Earl A.; Charles Robert Hickson (2001). Ideology and the evolution of vital institutions: guilds, the gold standard, and modern international cooperation. Boston: Kluwer Acad. Publ.. ISBN 0-792-37390-1. OCLC 46836861.

- Pollard, Sidney (1970). The gold standard and employment policies between the Wars. London: Methuen. ISBN 0-416-14250-8. OCLC 137456.

- Hanna, Hugh Henry; Charles Arthur Conant, Jeremiah Jenks (1903). Stability of international exchange: Report on the introduction of the gold-exchange standard into China and other silver-using countries. OCLC 6671835.

- Elks, Ken. "The complete history of British Coinage in 12 parts". Predecimal.com. Chris Perkins. http://www.predecimal.com/p1celtic.php. Retrieved 2008-11-13.

- Banking in modern Japan. Tokyo: Fuji Bank. 1967. ISBN 0333711394. OCLC 254964565.

- Officer, Lawrence H. (2008). "The New Palgrave Dictionary of Economics". In Steven N. Durlauf and Lawrence E. Blume. The New Palgrave Dictionary of Economics, 2nd Edition. Basingstoke: Palgrave Macmillan. pp. 488. doi:10.1057/9780230226203.0136. ISBN 0-333-78676-9. OCLC 181424188. http://www.dictionaryofeconomics.com/article?id=pde2008_B000137&goto=bimetalism&result_number=140. Retrieved 2008-11-13.

- Drummond, Ian M.; The Economic History Society (1987). The gold standard and the international monetary system 1900–1939. Houndmills, Basingstoke, Hampshire: Macmillan Education. ISBN 0-333-37208-5. OCLC 18324084.

- Hawtrey, Ralph George (1927). The Gold Standard in theory and practice. London: Longman. ISBN 0313221049. OCLC 250855462.

- Flandreau, Marc (2004). The glitter of gold: France, bimetallism, and the emergence of the international gold standard, 1848–1873. Oxford: Oxford University Press. ISBN 0-19-925786-8. OCLC 54826941.

- Lalor, John (2003) [1881]. Cyclopedia of Political Science, Political Economy and the Political History of the United States. London: Thoemmes Continuum. ISBN 1-84371-093-5. OCLC 52565505.

- Bernanke, Ben; Harold James (October 1990). The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison. Working Paper Series. 3488. Cambridge, Massachusetts: National Bureau of Economic Research. OCLC 22840844. http://www.nber.org/papers/w3488. Retrieved 2008-11-13. Also published as: Bernanke, Ben; Harold James (1991). "The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison". In R. Glenn Hubbard. Financial markets and financial crises. Chicago: University of Chicago Press. pp. 33–68. ISBN 0-226-35588-8. OCLC 231281602. http://books.google.com/books?id=MEfUi2H4cqwC&printsec=frontcover&cad=0#PRA1-PA33,M1. Retrieved 2008-11-13.

- Rothbard, Murray Newton (2006). "The World Currency Crisis". Making Economic Sense. Burlingame, California: Ludwig von Mises Institute. pp. 295–299. ISBN 0-945466-46-3. OCLC 78624652. http://books.google.com/books?id=elPzEDHG9ysC&printsec=frontcover&cad=0#PRA2-PA295,M1.

- Cassel, Gustav (1936). The downfall of the gold standard. Oxford: Clarendon Press. OCLC 237252.

- Braga de Macedo, Jorge; Barry J. Eichengreen and Jaime Reis (1996). Currency convertibility: the gold standard and beyond. New York City: Routledge. ISBN 0-415-14057-9. OCLC 33132906.

- Russell, William H. (1982). The Deceit of the Gold Standard and of Gold Monetization. American Classical College Press. ISBN 0-892-66324-3.

- Mitchell, Wesley C. (1908). Gold, prices, and wages under the greenback standard. Berkeley, California: The University Press. OCLC 1088693.

- Mouré, Kenneth (2002). The gold standard illusion: France, the Bank of France, and the International Gold Standard, 1914–1939. Oxford: Oxford University Press. ISBN 0-19-924904-0. OCLC 48544538.

- Bayoumi, Tamim A.; Barry J. Eichengreen and Mark P. Taylor (1996). Modern perspectives on the gold standard. Cambridge: Cambridge University Press. ISBN 0-521-57169-3. OCLC 34245103.

- Keynes, John Maynard (1925). The economic consequences of Mr. Churchill. London: Hogarth Press. OCLC 243857880.

- Keynes, John Maynard (1930). A treatise on money in two volumes. London: MacMillan. OCLC 152413612.

- Ferderer, J. Peter (1994). Credibility of the interwar gold standard, uncertainty, and the Great Depression. Annandale-on-Hudson, New York: Jerome Levy Economics Institute. OCLC 31141890.

- Aceña, Pablo Martín; Jaime Reis (2000). Monetary standards in the periphery: paper, silver and gold, 1854–1933. London: Macmillan Press. ISBN 0-333-67020-5. OCLC 247963508.

- Gallarotti, Giulio M. (1995). The anatomy of an international monetary regime: the classical gold standard, 1880–1914. Oxford: Oxford University Press. ISBN 0-19-508990-1. OCLC 30511110.

- Dick, Trevor J. O.; John E. Floyd (2004). Canada and the Gold Standard: Balance of Payments Adjustment Under Fixed Exchange Rates, 1871–1913. Cambridge: Cambridge University Press. ISBN 0-5216-1706-5. OCLC 59135525.

- Kenwood, A.G.; A. L. Lougheed (1992). The growth of the international economy 1820–1990. London: Routledge. ISBN 91-44-00079-0.

- Hofstadter, Richard (1996). "Free Silver and the Mind of "Coin" Harvey". The Paranoid Style in American Politics and Other Essays. Harvard: Harvard University Press. ISBN 0-674-65461-7. OCLC 34772674.

- Lewis, Nathan K. (2006). Gold: The Once and Future Money. New York: Wiley. ISBN 0-470-04766-6. OCLC 87151964.

- Withers, Hartley (1919). War-Time Financial Problems. London: J. Murray. OCLC 2458983. http://www.gutenberg.org/etext/13045. Retrieved 2008-11-14.

- Metzler, Mark (2006). Lever of Empire: The International Gold Standard and the Crisis of Liberalism in Prewar Japan.. Berkeley, California: University of California Press. p. [5]. ISBN 0-520-24420-6.</ref>

- Pietrusza, David (2011). 'It Shines for All': The Gold Standard Editorials of The New York Sun. New York City, New York: New York Sun Books. ISBN 1461156122.

External links

Listen to this article (info/dl)

This audio file was created from a revision of Gold standard dated 2007-12-04, and does not reflect subsequent edits to the article. (Audio help)More spoken articles

This audio file was created from a revision of Gold standard dated 2007-12-04, and does not reflect subsequent edits to the article. (Audio help)More spoken articles- What is The Gold Standard? University of Iowa Center for International Finance and Development

- History of the Bank of England Bank of England

- 1933 Audio of FDR's Explanation of the Banking Crisis & Gold Confiscation

- Is the Gold Standard Still the Gold Standard among Monetary Systems? by Lawrence H. White Ph.D. Professor of Economic History

- The Case for a 100 Percent Gold Dollar by Murray N. Rothbard Ph.D. Professor Emeritus of Economics

- The Gold Bug Variations by Paul Krugman Ph.D. Professor of Economics

- Timeline: Gold's history as a currency standard

Wikimedia Foundation. 2010.