- Taxation in the United Kingdom

-

Taxation in the United Kingdom

This article is part of the series:

Politics and government of

the United KingdomCentral government HM Treasury

HM Revenue and Customs

Income tax · PAYE

VAT · National Insurance

Corporation tax

Inheritance tax · Stamp duty

Capital gains tax · Excise tax

Motoring taxesLocal government Council Tax · Rates · Business rates Taxation by country- Australia

British Virgin Islands

Canada · China

Colombia · France

Germany · Hong Kong

India · Indonesia

Ireland · Netherlands

New Zealand · Peru

Russia · Singapore

Switzerland · Tanzania

United Kingdom

United States

European Union -

Tax rates around the world

Tax revenue as % of GDP -

• project Taxation in the United Kingdom may involve payments to a minimum of two different levels of government: The central government (HM Revenue and Customs) and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England and Wales, Council Tax and increasingly from fees and charges such as those from on-street parking. In the fiscal year 2007-08, total government revenue was 39.2 per cent of GDP, with net taxes and National Insurance contributions standing at 36.9 per cent of GDP[1]—approximately £600 billion (using 2008 nominal GDP measured in dollars, and converting using 2009 conversion rate).

Contents

History

Main article: History of taxation in the United KingdomA uniform Land tax was introduced in England during the late 17th century. This formed the main source of government revenue throughout the rest of the 17th century, the 18th century and the early 19th century.

Income tax was first implemented in Britain by William Pitt the Younger in his budget of December 1798 to pay for weapons and equipment in preparation for the Napoleonic Wars. Pitt's new graduated (progressive) income tax began at a levy of 2 old pence in the pound (1/120) on incomes over £60 (£5,077 as of 2011),[2] and increased up to a maximum of 2 shillings (10%) on incomes of over £200. Pitt hoped that the new income tax would raise £10 million, but actual receipts for 1799 totalled just over £6 million.[3]

Income tax was levied under five schedules. Income not falling within those schedules was not taxed. The schedules were:

- Schedule A (tax on income from UK land)

- Schedule B (tax on commercial occupation of land)

- Schedule C (tax on income from public securities)

- Schedule D (tax on trading income, income from professions and vocations, interest, overseas income and casual income)

- Schedule E (tax on employment income)

Later a sixth Schedule, Schedule F (tax on UK dividend income) was added.

Pitt's income tax was levied from 1799 to 1802, when it was abolished by Henry Addington during the Peace of Amiens. Addington had taken over as prime minister in 1801, after Pitt's resignation over Catholic Emancipation. The income tax was reintroduced by Addington in 1803 when hostilities recommenced, but it was again abolished in 1816, one year after the Battle of Waterloo. The UK income tax was reintroduced by Sir Robert Peel in the Income Tax Act 1842. Peel, as a Conservative, had opposed income tax in the 1841 general election, but a growing budget deficit required a new source of funds. The new income tax, based on Addington's model, was imposed on incomes above £150 (£11,468 as of 2011),[2].

UK income tax has changed over the years. Originally it taxed a person's income regardless of who was beneficially entitled[clarification needed] to that income, but now a person owes tax only on income to which he or she is beneficially entitled. Most companies were taken out of the income tax net in 1965 when corporation tax was introduced. These changes were consolidated by the Income and Corporation Taxes Act 1970. Also the schedules under which tax is levied have changed. Schedule B was abolished in 1988, Schedule C in 1996 and Schedule E in 2003. For income tax purposes, the remaining schedules were superseded by the Income Tax (Trading and Other Income) Act 2005, which also repealed Schedule F completely. The Schedular system and Schedules A and D still remain in force for corporation tax. The highest rate peaked in the Second World War at 99.25% and remained at about 95% till the late 1970s.[citation needed]

Tax revenues as a percentage of GDP for the U.K. in comparison to the OECD and the EU 15.

Tax revenues as a percentage of GDP for the U.K. in comparison to the OECD and the EU 15.

In 1974 the top-rate of income tax increased to its highest rate since the war, 83%. This applied to incomes over £20,000 (£155,247 as of 2011),[2], and combined with a 15% surcharge on 'un-earned' income (investments and dividends) could add to a 98% marginal rate of personal income tax. In 1974, as many as 750,000 people were liable to pay the top-rate of income tax.[4] Margaret Thatcher, who favoured indirect taxation, reduced personal income tax rates during the 1980s.[5] In the first budget after her election victory in 1979, the top rate was reduced from 83% to 60% and the basic rate from 33% to 30%.[6] The basic rate was also cut for three successive budgets - to 29% in the 1986 budget, 27% in 1987 and to 25% in 1988.[7] The top rate of income tax was cut to 40% in the 1988 budget.

Business rates were introduced in England and Wales in 1990, and are a modernised version of a system of rating that dates back to the Elizabethan Poor Law of 1601. As such, business rates retain many previous features from, and follow some case law of, older forms of rating. The Finance Act 2004 introduced an income tax regime known as "pre-owned asset tax" which aims to reduce the use of common methods of inheritance tax avoidance.[8]

Overview

Income tax forms the bulk of revenues collected by the government. The second largest source of government revenue is National Insurance Contributions. The third largest source of government revenues is value added tax (VAT), and the fourth-largest is corporation tax.

Residence and domicile

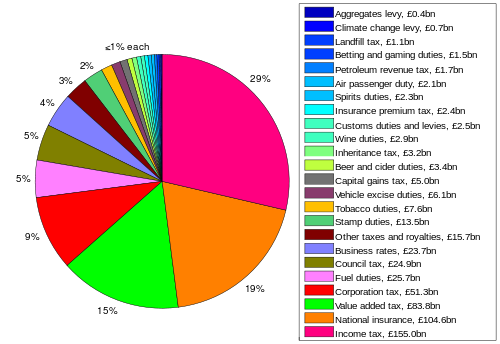

A pie chart showing the projected constituents of UK taxation receipts for the tax year 2008-2009, according to the 2008 Budget.

A pie chart showing the projected constituents of UK taxation receipts for the tax year 2008-2009, according to the 2008 Budget.UK source income is generally subject to UK taxation no matter the citizenship nor the place of residence of the individual nor the place of registration of the company.

For individuals this means the UK income tax liability of one who is neither resident nor ordinarily resident in the UK is limited to any tax deducted at source on UK income, together with tax on income from a trade or profession carried on through a permanent establishment in the UK and tax on rental income from UK real estate.

Individuals who are both resident and domiciled in the UK are additionally liable to taxation on their worldwide income and gains. For individuals resident but not domiciled in the UK (a "non-dom"), foreign income and gains have historically been taxed on the remittance basis, that is to say, only income and gains remitted to the UK are taxed (for such people the UK is sometimes called a tax haven). However from 6 April 2008, a (long term [resident 7 of previous 9 years]) non-dom wishing to retain the remittance basis is required to pay an annual tax of £30,000.[9]

UK domiciled inviduals who are not resident for three consecutive tax years are not liable for UK taxation on their worldwide income, and those who are not resident for five consecutive tax years are not liable for UK taxation on their worldwide capital gains. Anyone who stays in the UK for 183 or more days per year is resident.

Domicile here is a term with a technical meaning. Very roughly (and this is a considerable simplification) an individual is domiciled in the UK if he was born in the UK or if the UK is his permanent home, and is not a UK domicile if he was born outside of the UK and does not intend to remain permanently.

A company is resident in the UK if it is UK-incorporated or if its central management and control are in the UK (although in the former case a company could be resident in another jurisdiction in certain circumstances where a tax treaty applies).

Double taxation of income and gains may be avoided by an applicable double tax treaty - the UK has one of the largest networks of treaties of any country.[10][11]

Examples of non-dom status

Most migrant workers (including those from within the EEA) would classify as non-doms. However, since the non-dom exemption applies only to income sourced from outside of the UK, the majority of people making use of the tax exemption are wealthy individuals with substantial income from outside of the UK (e.g. from foreign savings). Typical such individuals include senior company executives, bankers, lawyers, business owners and international recording artists.

The tax year

The tax year in the UK, which applies to income tax and other personal taxes, runs from 6 April in one year to 5 April the next (for income tax purposes). Hence the 2010-11 tax year ran from 6 April 2010 to 5 April 2011.

The odd dates are due to events in the mid-18th century. The English quarter days are traditionally used as the dates for collecting rents (on, for example, agricultural properties). The tax system was also based on a tax year ending on Lady Day (25 March). When the Gregorian calendar was adopted in the UK in September 1752 in place of the Julian calendar, the two were out of step by 11 days. However, it was felt unacceptable for the tax authorities to lose out on 11 days' tax revenues, so the start of the tax year was moved, firstly to 5 April and then, in 1800, to 6 April.

The tax year is sometimes also called the Fiscal Year. The Financial Year, used mainly for corporation tax purposes, runs from 1 April to 31 March. Financial Year 2011 runs from 1 April 2010 to 31 March 2011, as Financial Years are named according to the calendar year in which they end.

Personal taxes

Income tax

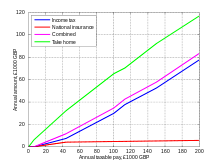

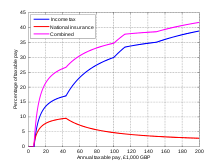

UK income tax and National Insurance charges (2010-11).

UK income tax and National Insurance charges (2010-11). UK income tax and National Insurance as a percentage of taxable pay (2010-11).

UK income tax and National Insurance as a percentage of taxable pay (2010-11).Income tax forms the single largest source of revenues collected by the government (followed by national insurance contributions, an additional levy on incomes at around 20%[12]). Each person has an income tax personal allowance, and income up to this amount in each tax year is free of tax for everyone. For 2010-11 the tax allowance for under 65s is £6,475. This reduces by £1 for every £2 of taxable income above £100,000.[13] On 22 June 2010, the Chancellor (George Osborne) increased the personal allowance by £1000 in his emergency budget, bringing it to £7,475 for the tax year 2011-12.[14]

Above this amount there are a number of tax bands — each taxed at a different rate (as of 2010-11):[13]

Rate Dividend income Savings income Other income (inc employment) Band (above any personal allowance) Lower rate N/A 10% N/A £0 - £2440

applies only if total income falls in this bandBasic rate 10% 20% 20% £7,445 - £37,400 Higher rate 32.5% 40% 40% over £37,400 Additional rate 42.5% 50% 50% over £150,000 This table reflects the removal of the 10% starting rate from April 2008, which also saw the 22% income tax rate drop to 20%. Alistair Darling announced in the 2009 budget (22 April 2009) that, from April 2010 there would be a new 50% income tax rate for those earning more than £150,000.

After consideration of employer and employee National Insurance contributions, the effective marginal top rate for 2011-12 is 58%: that is, to pay an employee £1,000 gross costs the employer £1,138 and the employee receives £480 after deductions.

The taxpayer's income is assessed for tax according to a prescribed order, with income from employment using up the personal allowance and being taxed first, followed by savings income (from interest or otherwise unearned) and then dividends.

Foreign income of UK residents is taxed as UK income, but to prevent double taxation the UK has agreements with many countries to allow offset against UK tax what is deemed paid abroad. These deemed amounts paid abroad are not necessarily as much as actually paid.[15] Sometimes it is necessary to inform foreign authorities that tax should be withheld at the deemed rate.[16][unreliable source?]

Rental income on a property investment business (such as a buy to let property) is taxed as other savings income, after allowing deductions including mortgage interest. The mortgage does not need to be secured against the property receiving the rent, subject to a maximum of the purchase prices of the property investment business properties (or the market value at the time they transferred into the business). Joint owners can decide how they divide income and expenses[17], as long as one does not make a profit and the other a loss. Losses can be brought forward to subsequent years.

Exemptions on Investment

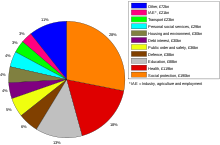

UK central government expenditure projection for tax year 2009-2010, according to the 2009 Pre-Budget Report.

UK central government expenditure projection for tax year 2009-2010, according to the 2009 Pre-Budget Report.Certain investments carry a tax favoured status including:

While all income is taxable, gains are exempt for income tax purposes.

Certain investments via the state owned National Savings scheme are not subject to tax including Index linked Certificates (up to £15,000 per issue) and Premium Bonds, a scheme that issues monthly prizes in place of interest on individual holdings up to £30,000.

Interest is paid tax-free, while dividends are paid along with a tax credit to the investor which can then be offset against dividend tax due. For a basic rate tax payer this means they have no tax to pay on a dividend. There is no overall limit on how much a person can have invested in ISA accounts, but additional investments are currently limited to £10,680 per person per year: a maximum of £5,340 in cash funds, with the balance being allocated either to mutual funds (Units Trusts and OEICs) or individual self-selected shares.[18]

- Pension funds

These have the same tax treatment as ISAs in terms of growth. Full tax relief is also given at the individual's marginal rate on contributions or, in the case of an employer contributions, it is treated as an expense and is not taxed on the employee as a benefit in kind. Aside from a tax free lump sum of 25% of the fund, benefits taken from pension funds are taxable.

These are investments in smaller companies or funds of holdings in such companies over a minimum term of five years. These are not taxable and qualify for 30% tax relief against an individual's income.

A non taxable investment into smaller company shares over three years that qualifies for 20% tax relief. The facility also allows an indiviudal to defer capital gains liabilities (these gains can be stripped out in future years using the annual CGT allowance.)

These include offshore and onshore investment bonds issued by insurance companies. The main difference between the two is that corporation tax paid by the onshore bond means that gains in the onshore bond are treated as if basic rate tax has been paid (this cannot be reclaimed by zero or starting rate tax payers). With both versions up to 5% for each complete year of investment can be taken without an immediate tax liability (subject to a maximum total of 100% of the original investment). On this basis, investors can plan an income stream while deferring any chargeable withdrawals until they are on a lower rate of tax, are no longer a UK resident, or their death.

- Offshore trusts and companies

Trusts can be offshore if all trustees are non-resident. Such trusts can own foreign-operated companies. Corporation tax rates can be lower in some countries and where we still have double taxation treaties. However, since anti-avoidance rules have been introduced for taxation of trusts, these structures are not advantageous for someone who will remain resident.

Exceptions

Many holdings and income from them are exempt for "historical reasons". These include

- Special, low tax arrangements for the monarchy, such as the arrangement used by the British Royal Family[19] to avoid inheritance taxation.

- Reduced income tax for special classes of person, such as non-doms, who claim to be resident in the UK but not "domiciled".[20]

- An Act of Parliament to protect the Earl of Abingdon and his “heirs and assignees” from paying income tax on the tolls on the Swinford Toll Bridge.

- The income of charities is usually exempt from UK income tax.[21]

Inheritance tax

Inheritance tax is levied on "transfers of value", meaning:

- the estates of deceased persons;

- gifts made within seven years of death (known as Potentially Exempt Transfers or "PETs");

- "lifetime chargeable transfers", meaning transfers into certain types of trust. See Taxation of trusts (United Kingdom).

The first slice of cumulative transfers of value (known as the "nil rate band") is free of tax. This threshold is currently set at £325,000 (tax year 2009-10)[22] and, although it is raised annually, it has recently failed to keep up with house price inflation with the result that some 6 million households currently fall within the scope of inheritance tax. Over this threshold the rate is 40% on death. Any inheritance tax must be paid by the executors or administrators of the estate (the burden falling upon the beneficiaries) before probate is granted.

Transfers of value between UK-domiciled spouses are exempt from tax. Recent changes to the tax brought in by the Finance Act 2008 mean that nil-rate bands are transferable between spouses to reduce this burden - something which previously could only be done by setting up complex trusts.

Gifts made more than seven years prior to death are not taxed; if they are made between three and seven years before death a tapered inheritance tax rate applies. There are some important exceptions to this treatment: the most important is the "reservation of benefit rule", which says that a gift is ineffective for inheritance tax purposes if the giver benefits from the asset in any way after the gift (for example, by gifting a house but continuing to live in it).

Council Tax

Council tax is the system of local taxation used in England,[23] Scotland[24] and Wales[25] to part fund the services provided by local government in each country. It was introduced in 1993 by the Local Government Finance Act 1992, as a successor to the unpopular Community Charge ("poll tax"), which had (briefly) replaced the Rates system. The basis for the tax is residential property, with discounts for single people. As of 2008, the average annual levy on a property in England was £1,146.[26] In 2006/2007 council tax in England amounted to £22.4 billion[27] and an additional £10.8 billion in sales, fees and charges,[28]

Sales taxes and duties

Value added tax

The third largest source of government revenues is value added tax (VAT), charged at 20% on supplies of goods and services. It is therefore a tax on consumer expenditure.

Certain goods and services are exempt from VAT, and others are subject to VAT at a lower rate of 5% (the reduced rate, such as domestic gas supplies) or 0% ("zero-rated", such as most food and children's clothing).[29] Exemptions are intended to relieve the tax burden on essentials while placing the full tax on luxuries, but disputes based on fine distinctions arise, such as the notorious "Jaffa Cake Case" which hinged on whether Jaffa Cakes were classed as (zero-rated) cakes—as was eventually decided—or (fully taxed) chocolate-covered biscuits. Until 2001, VAT was charged at the full rate on sanitary towels. [4]

It was introduced in 1973, in consequence of Britain's entry to the European Economic Community, at a standard rate of 10%. In July 1974, the standard rate became 8%, and from October that year petrol was taxed at a new higher rate of 25% (reduced to 12.5% in 1976). In 1979, the higher rate was scrapped and VAT consolidated to a single rate of 15%. In 1991 this became 17.5%, though when domestic fuel and power was added to the scheme in 1994, it was charged at a new, lower rate of 8%.[30]. In September 1997 this lower rate was reduced to 5%, and was extended to cover various energy-saving materials (from 1st July 1998), Sanitary Protection (from 1st January 2001), children's car seats (from 1st April 2001), conversion and renovation of certain residential properties (from 12th May 2001), contraceptives (from 1st July 2006) and smoking cessation products (from 1st July 2007).

On 1 December 2008, VAT was reduced to 15%, as a reaction to the late-2000s recession, by Labour Chancellor Alistair Darling.

On 1 January 2010 VAT returned to 17.5%, again by Labour.

On 4 January 2011 VAT was raised to 20% by Conservative Chancellor George Osborne, where it remains.

Excise duties

Excise duties are charged on, amongst other things, motor fuel, alcohol, tobacco, betting and vehicles.

Stamp duty

Stamp duty is charged on the transfer of shares and certain securities at a rate of 0.5%. Modernised versions of stamp duty, stamp duty land tax and stamp duty reserve tax, are charged respectively on the transfer of real property and shares and securities, at rates of up to 4% and 0.5% respectively.[31]

Motoring taxation

Motoring taxes include: fuel duty (which itself also attracts VAT), and vehicle excise duty. Other fees and charges include the London congestion charge, various statutory fees including that for the compulsory vehicle test and that for vehicle registration, and in some areas on-street parking (as well as associated charges for violations).

Business taxes

Corporate Tax

U.K. corporate tax revenue as a percentage of GDP compared to the OECD and the EU 15.

U.K. corporate tax revenue as a percentage of GDP compared to the OECD and the EU 15.Corporation tax is a tax levied in the United Kingdom on the profits made by companies and on the profits of permanent establishments of non-UK resident companies and associations that trade in the EU.

Corporation tax forms the fourth-largest source of government revenue (after income, NIC, and VAT). Prior to the tax's enactment on 1 April 1965, companies and individuals paid the same income tax, with an additional profits tax levied on companies. The Finance Act 1965[32] replaced this structure for companies and associations with a single corporate tax, which borrowed its basic structure and rules from the income tax system. Since 1997, the UK's Tax Law Rewrite Project[33] has been modernising the UK's tax legislation, starting with income tax, while the legislation imposing corporation tax has itself been amended; the rules governing income tax and corporation tax have thus diverged.

Business rates

Business rates is the commonly used name of non-domestic rates, a United Kingdom rate or tax charged to occupiers of non-domestic property. Business rates form part of the funding for local government, and are collected by them, but rather than receipts being retained directly they are pooled centrally and then redistributed. In 2005/06, £19.9 billion was collected in business rates, representing 4.35% of the total UK tax income.[34]

Business rates are a property tax, where each non-domestic property is assessed with a rateable value, expressed in pounds. The rateable value broadly represents the annual rent the property could have been let for on a particular valuation date according to a set of assumptions. The actual bill payable is then calculated using a multiplier set by central government, and applying any reliefs.[35]

Business and personal taxes

Some taxes are, depending on the circumstances, paid by both individuals and companies and government

National Insurance contributions

The second largest source of government revenues is National Insurance contributions (NIC). NIC is payable by employees, employers and the self-employed and by 2006, it formed 17% of total government receipts (£90 billion), amounting to around 20% of gross income in middle brackets[36].

Employees are taxed according to a classification based on their employment type and income. Class 1 (non self-employed persons) NIC is charged at rates depending on income thresholds. The lower and upper thresholds were £105 and £770 per week in 2008-09.[37] A zero–rate of NIC applies to earnings between the lower earnings limit of £90 per week and the earnings threshold of £105 per week (in 2008-09) to protect employees' contributory benefit entitlements. Above this, NIC is levied at 11%, but can be contracted-out for persons with a qualifying pension scheme with a reduction of 1.6%. NIC was raised by the addition of a 1% rate on income above the upper threshold[when?].

In addition, employers pay tax at 12.8% on employees earnings over the lower earnings threshold, with no upper threshold, so total earnings are taxed at 12.8% per employee. Employers are additionally liable to Class 1A NIC at 12.8% on most benefits-in-kind provided to employees which are subject to income tax in the hands of the employee, and to Class 1B NIC (also at 12.8%) on the value of the tax and on certain benefits paid via a "PAYE Settlement Agreement".

As of 2012, for an individual on an annual income of £40,000 (£3,330/month), NI would be charged at £706 made up of a charge to the employee of £327.72 and to the employer of £ 378.67 per month[38].

There are separate arrangements for self-employed persons (who are normally liable to Class 2 flat rate NIC and Class 4 earnings-related NIC), married women, and voluntary sector workers.

Capital gains tax

Capital gains are subject to tax at 18-28% (for individuals) or at the applicable marginal rate of corporation tax (for companies).

The basic principle is the same for individuals and companies - the tax applies only on the disposal of a capital asset, and the amount of the gain is calculated as the difference between the disposal proceeds and the "base cost", being the original purchase price plus allowable related expenditure. However, from 6 April 2008, the rate and reliefs applicable to the chargeable gain differ between individuals and companies. Companies apply "indexation relief" to the base cost, increasing it in accordance with the Retail Prices Index so that (broadly speaking) the gain is calculated on a post-inflation basis (with different rules apply for gains accrued prior to March 1982). The gain is then subject to tax at the applicable marginal rate of corporation tax.

Individuals are taxed at a flat rate of 18% (or since 22 June 2010, 28% for higher rate taxpayers) with no indexation relief. However, if claiming Entrepreneurs' Relief the rate remains 10%. Capital losses from prior years can be brought forward.

Expenditure on a business (such as a property business) made by an individual can be claimed as an allowance against Capital Gains. Whether expenditure is claimable against income (potentially reducing income tax) or capital (potentially reducing capital gains tax) depends on whether there was improvement of the property: if there was none, it is against income; if there was some, then it is against capital.

Transfers between husband and wife or between civil partners do not crystallise a capital gain, but instead transfer the purchase price and allowances. Otherwise, transfers made as gifts are treated for CGT purposes as being made at the market value at the date of transfer.

See also

- UK related

- HM Revenue & Customs

- Chartered Institute of Taxation

- Government spending in the United Kingdom

- Institute of Indirect Taxation

- Income in the United Kingdom

- Tax credit

- Starting rate of UK income tax

- Local taxation

- Business rates

- Council tax

- Local income tax

- General category

Notes

- ^ _210808.xls "Public Finances Databank". HM Treasury. 2008-08-21. pp. C1. http://www.hm-treasury.gov.uk/media/A/9/pfd_210808.xls. Retrieved 2008-08-23.

- ^ a b c UK CPI inflation numbers based on data available from Lawrence H. Officer (2010) "What Were the UK Earnings and Prices Then?" MeasuringWorth.

- ^ "A tax to beat Napoleon". HM Revenue & Customs. http://www.hmrc.gov.uk/history/taxhis1.htm. Retrieved 2007-01-24.

- ^ IFS: Long-Term trends in British Taxation and Spending

- ^ Thatcher Economics

- ^ 1979 budget

- ^ 1988 budget

- ^ REV BN 40: Tax Treatment Of Pre-Owned Assets

- ^ [1] [2]

- ^ [3]

- ^ See IR20 - Residents and non-residents.

- ^ http://nicecalculator.hmrc.gov.uk/Class1NICs2.aspx HMRC NI calculator

- ^ a b "Rates and Allowances - Income Tax". HM Revenue & Customs. http://www.hmrc.gov.uk/rates/it.htm. Retrieved 2010-05-02.

- ^ "Emergency Budget 22 June 2010". HM Revenue & Customs. http://www.hmrc.gov.uk/budget2010/index.htm. Retrieved 2010-06-25.

- ^ http://www.hmrc.gov.uk/si/double.htm

- ^ http://monevator.com/2010/11/25/withholding-tax-on-dividends/

- ^ http://www.hmrc.gov.uk/bulletins/tb2.htm#anchor44570

- ^ http://www.moneysupermarket.com/c/savings/isas/guide#How-much-invest

- ^ Kay, Richard. "Palace fear over Queen's tax bill". Daily Mail (London). http://www.dailymail.co.uk/news/article-113128/Palace-fear-Queens-tax-bill.html.

- ^ Wintour, Patrick (1 December 2009). "David Cameron tells Zac Goldsmith to end 'non-dom' tax status". The Guardian (London). http://www.guardian.co.uk/politics/2009/dec/01/cameron-goldsmith-non-dom-status. Retrieved 24 May 2010.

- ^ Taxation of Charities and Non-profit Organisations, James Kessler QC and Harriet Brown, 8th edition (2011)

- ^ "Rates and Allowances - Inheritance tax". HM Revenue & Customs. http://www.hmrc.gov.uk/rates/inheritance.htm. Retrieved 2007-01-24.

- ^ Communities and Local Government - Council Tax: The Facts

- ^ Council Tax in Scotland Scottish Government publications

- ^ Council Tax a guide Valuation Office Agency

- ^ Average council tax and % change 1999-00 to 2008-09 Communities and local government - figures released 27th March 2008

- ^ Office of the Deputy Prime Minister, Statistical Release: Levels of council tax set by local authorities in England 2006/07, 2006 cited by.

- ^ Communities and Local Government in Local Government Finance Statistics: Revenue Outturn Service Expenditure Summary 2006/07. cited by

- ^ "Introduction to VAT". HM Revenue & Customs. http://www.hmrc.gov.uk/vat/start/introduction.htm. Retrieved 2008-11-23.

- ^ Peter Victor (30 July 1995). "A brief history of VAT". The Independent (London). http://www.independent.co.uk/news/a-brief-history-of-vat-1593926.html. Retrieved 13 January 2011.

- ^ "Stamp Duty Land Tax Rates From 23/03/06 including archived Budget and Finance Bill information". HM Revenue & Customs. 2006-03-23. http://www.hmrc.gov.uk/so/current_sdlt_rates.htm. Retrieved 2007-01-24.

- ^ "Finance Act 1965 (c. 25), from UK Statute Law Database". UK Statutory Publications Office, Ministry of Justice. http://www.statutelaw.gov.uk/content.aspx?LegType=All+Legislation&title=Finance+Act+1965&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&sortAlpha=0&TYPE=QS&PageNumber=1&NavFrom=0&parentActiveTextDocId=1171400&ActiveTextDocId=1171400&filesize=108865. Retrieved 2007-05-09.

- ^ Tax Law Rewrite, Her Majesty's Revenue and Customs (HMRC), retrieved 17 April 2007

- ^ Public Finances Databank (see section C4), HM Treasury, retrieved 26 March 2007. Percentage based on Net taxes & NICs conts.

- ^ The rates bill - How is it calculated?, mybusinessrates.gov.uk

- ^ http://nicecalculator.hmrc.gov.uk/Class1NICs2.aspx%7CHMRC NI calculator

- ^ "Rates and Allowances - National Insurance Contributions". HM Revenue & Customs. http://www.hmrc.gov.uk/rates/nic.htm. Retrieved 2007-01-24.

- ^ http://nicecalculator.hmrc.gov.uk/Class1NICs2.aspx%7CHMRC NI calculator

References

- James Kessler QC, Taxation of Non-Residents and Foreign Domiciliaries (10th edn Key Haven Publications 2011) - discusses taxation of individuals who are UK resident but not UK domiciled.

- James Kessler QC and Harriet Brown, Taxation of Charities and Non-Profit Organisations (8th edn Key Haven Publications 2011) - discusses taxation of charities and the many exemptions from tax for charities.

External links

- Guide to personal taxation, from UK government site Directgov (Doesn't link to correct file, website redirects to index)

- Yahoo tax, UK tax portal

- TaxationWeb, UK tax portal

- Tax Help and Information, Documents with information about capital allowances and tax in the UK

- Tax Office UK, Business Tax, Property Tax, UK Taxes

- Taxation, weekly news information for UK tax practitioners

- PAYE calculator

- VAT Calculator

- Taxation of Charities online

- Taxation of Non-residents and Foreign Domiciliaries online

- UK VAT calculator

Taxation in Europe Sovereign

states- Albania

- Andorra

- Armenia

- Austria

- Azerbaijan

- Belarus

- Belgium

- Bosnia and Herzegovina

- Bulgaria

- Croatia

- Cyprus

- Czech Republic

- Denmark

- Estonia

- Finland

- France

- Georgia

- Germany

- Greece

- Hungary

- Iceland

- Ireland

- Italy

- Kazakhstan

- Latvia

- Liechtenstein

- Lithuania

- Luxembourg

- Macedonia

- Malta

- Moldova

- Monaco

- Montenegro

- Netherlands

- Norway

- Poland

- Portugal

- Romania

- Russia

- San Marino

- Serbia

- Slovakia

- Slovenia

- Spain

- Sweden

- Switzerland

- Turkey

- Ukraine

- United Kingdom

States with limited

recognition- Abkhazia

- Kosovo

- Nagorno-Karabakh

- Northern Cyprus

- South Ossetia

- Transnistria

Other entities - European Union

United Kingdom topics

United Kingdom topicsGeography Administrative Physical Lakes and lochs · Mountains · Rivers · Volcanoes · Great Britain · Geology of Great Britain · Geology of Northern Ireland

History Maritime · Economic · Military · British Empire · Timeline

Politics · Government Economy Pound sterling · London Stock Exchange · Banks (Bank of England) · Taxation · Transport · Communications · Economic geography · Mining · Energy · Budget

Military Society · Demography Cities · Crime · Ethnic groups · Immigration · Languages · Poverty · Social structure · Towns

Culture Art · Cinema · Cuisine · Identity · Literature · Media · Music · Sport · Television · Theatre · Public holidays

England Northern Ireland Scotland Wales History · Welsh Government · Welsh Assembly · First Minister · Politics · Education · Health care · Religion · Tourism

Category ·

Category ·  Portal ·

Portal ·  WikiProjectCategories:

WikiProjectCategories: - Australia

Wikimedia Foundation. 2010.