- Mathematical economics

-

Economics  Economies by region

Economies by regionGeneral categories Microeconomics · Macroeconomics

History of economic thought

Methodology · Mainstream & heterodoxTechnical methods Mathematical economics

Game theory · Optimization

Computational · Econometrics

Experimental · National accountingFields and subfields Behavioral · Cultural · Evolutionary

Growth · Development · History

International · Economic systems

Monetary and Financial economics

Public and Welfare economics

Health · Education · Welfare

Population · Labour · Managerial

Business · Information

Industrial organization · Law

Agricultural · Natural resource

Environmental · Ecological

Urban · Rural · Regional · GeographyLists Business and Economics Portal Mathematical economics is the application of mathematical methods to represent economic theories and analyze problems posed in economics. It allows formulation and derivation of key relationships in a theory with clarity, generality, rigor, and simplicity. By convention, the methods refer to those beyond simple geometry, such as differential and integral calculus, difference and differential equations, matrix algebra, and mathematical programming[1][2] and other computational methods.[3]

Mathematics allows economists to form meaningful, testable propositions about many wide-ranging and complex subjects which could not be adequately expressed informally. Further, the language of mathematics allows economists to make clear, specific, positive claims about controversial or contentious subjects that would be impossible without mathematics.[4] Much of economic theory is currently presented in terms of mathematical economic models, a set of stylized and simplified mathematical relationships that clarify assumptions and implications.[5]

Broad applications include:

• optimization problems as to goal equilibrium, whether of a household, business firm, or policy maker

• static (or equilibrium) analysis in which the economic unit (such as a household) or economic system (such as a market or the economy) is modeled as not changing

• comparative statics as to a change from one equilibrium to another induced by a change in one or more factors

• dynamic analysis, tracing changes in an economic system over time, for example from economic growth.[1][6][7]Formal economic modeling began in the 19th century with the use of differential calculus to represent and explain economic behavior, such as utility maximization, an early economic application of mathematical optimization. Economics became more mathematical as a discipline throughout the first half of the 20th century, but introduction of new and generalized techniques in the period around the Second World War, as in game theory, would greatly broaden the use of mathematical formulations in economics.[8][7]

This rapid systematizing of economics alarmed critics of the discipline as well as some noted economists. John Maynard Keynes, Robert Heilbroner, Friedrich Hayek and others have criticized the broad use of mathematical models for human behavior, arguing that some human choices are irreducible to mathematics.

Contents

- 1 History

- 2 Modern mathematical economics

- 3 The mathematicization of economics

- 4 Econometrics

- 5 Application

- 6 Criticisms and defences

- 7 Mathematical economists

- 8 Notes

- 9 External links

History

Main article: History of economic thoughtThe use of mathematics in the service of social and economic analysis dates back to the 17th century. Then, mainly in German universities, a style of instruction emerged which dealt specifically with detailed presentation of data as it related to public administration. Gottfried Achenwall lectured in this fashion, coining the term statistics. At the same time, a small group of professors in England established a method of "reasoning by figures upon things relating to government" and referred to this practice as Political Arithmetick.[9] Sir William Petty wrote at length on issues that would later concern economists, such as taxation, Velocity of money and national income, but while his analysis was numerical, he rejected abstract mathematical methodology. Petty's use of detailed numerical data (along with John Graunt) would influence statisticians and economists for some time, even though Petty's works were largely ignored by English scholars.[10]

The mathematization of economics began in earnest in the 19th century. Most of the economic analysis of the time was what would later be called classical economics. Subjects were discussed and dispensed with through algebraic means, but calculus was not used. More importantly, until Johann Heinrich von Thünen's The Isolated State in 1826, economists did not develop explicit and abstract models for behavior in order to apply the tools of mathematics. Thünen's model of farmland use represents the first example of marginal analysis.[11] Thünen's work was largely theoretical, but he also mined empirical data in order to attempt to support his generalizations. In comparison to his contemporaries, Thünen built economic models and tools, rather than applying previous tools to new problems.[12]

Meanwhile a new cohort of scholars trained in the mathematical methods of the physical sciences gravitated to economics, advocating and applying those methods to their subject.[13] These included W.S. Jevons who presented paper on a "general mathematical theory of political economy" in 1862, providing an outline for use of the theory of marginal utility in political economy.[14] In 1871, he published The Principles of Political Economy, declaring that the subject as science "must be mathematical simply because it deals with quantities." Jevons expected the only collection of statistics for price and quantities would permit the subject as presented to become an exact science.[15] Others preceded and followed in expanding mathematical representations of economic problems.

Marginalists and the roots of neoclassical economics

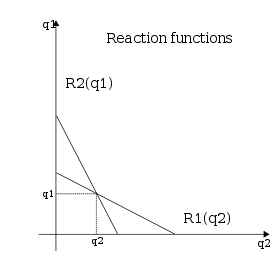

Main article: Marginalism Equilibrium quantities as a solution to two reaction functions in Cournot duopoly. Each reaction function is expressed as a linear equation dependent upon quantity demanded.

Equilibrium quantities as a solution to two reaction functions in Cournot duopoly. Each reaction function is expressed as a linear equation dependent upon quantity demanded.

Augustin Cournot and Léon Walras built the tools of the discipline axiomatically around utility, arguing that individuals sought to maximize their utility across choices in a way that could be described mathematically.[16] At the time, it was thought that utility was quantifiable, in units known as utils.[17] Cournot, Walras and Francis Ysidro Edgeworth are considered the precursors to modern mathematical economics.[18]

Augustin Cournot

Cournot, a professor of Mathematics, developed a mathematical treatment in 1838 for duopoly—a market condition defined by competition between two sellers.[18] This treatment of competition, first published in Researches into the Mathematical Principles of Wealth,[19] is referred to as Cournot duopoly. It is assumed that both sellers had equal access to the market and could produce their goods without cost. Further, it assumed that both goods were homogeneous. Each seller would vary her output based on the output of the other and the market price would be determined by the total quantity supplied. The profit for each firm would be determined by multiplying their output and the per unit Market price. Differentiating the profit function with respect to quantity supplied for each firm left a system of linear equations, the simultaneous solution of which gave the equilibrium quantity, price and profits.[20] Cournot's contributions to the mathematization of economics would be neglected for decades, but eventually influenced many of the marginalists.[20][21] Cournot's models of duopoly and Oligopoly also represent one of the first formulations of non-cooperative games. Today the solution can be given as a Nash equilibrium but Cournot's work preceded modern Game theory by over 100 years.[22]

Léon Walras

While Cournot provided a solution for what would later be called partial equilibrium, Léon Walras attempted to formalize discussion of the economy as a whole through a theory of general competitive equilibrium. The behavior of every economic actor would be considered on both the production and consumption side. Walras originally presented four separate models of exchange, each recursively included in the next. The solution of the resulting system of equations (both linear and non-linear) is the general equilibrium.[23] At the time, no general solution could be expressed for a system of arbitrarily many equations, but Walras's attempts produced two famous results in economics. The first is Walras' law and the second is the principle of tâtonnement. Walras' method was considered highly mathematical for the time and Edgeworth commented at length about this fact in his review of Éléments d'économie politique pure (Elements of Pure Economics).[24]

Walras' law was introduced as a theoretical answer to the problem of determining the solutions in general equilibrium. His notation is different from modern notation but can be constructed using more modern summation notation. Walras assumed that in equilibrium, all money would be spent on all goods: every good would be sold at the market price for that good and every buyer would expend their last dollar on a basket of goods. Starting from this assumption, Walras could then show that if there were n markets and n-1 markets cleared (reached equilibrium conditions) that the nth market would clear as well. This is easiest to visualize with two markets (considered in most texts as a market for goods and a market for money). If one of two markets has reached an equilibrium state, no additional goods (or conversely, money) can enter or exit the second market, so it must be in a state of equilibrium as well. Walras used this statement to move toward a proof of existence of solutions to general equilibrium but it is commonly used today to illustrate market clearing in money markets at the undergraduate level.[25]

Tâtonnement (roughly, French for groping toward) was meant to serve as the practical expression of Walrasian general equilibrium. Walras abstracted the marketplace as an auction of goods where the auctioneer would call out prices and market participants would wait until they could each satisfy their personal reservation prices for the quantity desired (remembering here that this is an auction on all goods, so everyone has a reservation price for their desired basket of goods).[26]

Only when all buyers are satisfied with the given market price would transactions occur. The market would "clear" at that price—no surplus or shortage would exist. The word tâtonnement is used to describe the directions the market takes in groping toward equilibrium, settling high or low prices on different goods until a price is agreed upon for all goods. While the process appears dynamic, Walras only presented a static model, as no transactions would occur until all markets were in equilibrium. In practice very few markets operate in this manner.[27]

Francis Ysidro Edgeworth

Edgeworth introduced mathematical elements to Economics explicitly in Mathematical Psychics: An Essay on the Application of Mathematics to the Moral Sciences, published in 1881.[28] He adopted Jeremy Bentham's felicific calculus to economic behavior, allowing the outcome of each decision to be converted into a change in utility.[29] Using this assumption, Edgeworth built a model of exchange on three assumptions: individuals are self interested, individuals act to maximize utility, and individuals are "free to recontract with another independently of...any third party."[30]

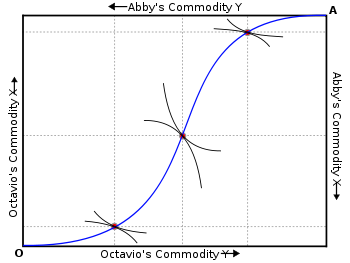

An Edgeworth box displaying the contract curve an economy with two participants. Referred to as the "core" of the economy in modern parlance, there are infinitely many solutions along the curve for economies with two participants[31]

An Edgeworth box displaying the contract curve an economy with two participants. Referred to as the "core" of the economy in modern parlance, there are infinitely many solutions along the curve for economies with two participants[31]Given two individuals, the set of solutions where the both individuals can maximize utility is described by the contract curve on what is now known as an Edgeworth Box. Technically, the construction of the two-person solution to Edgeworth's problem was not developed graphically until 1924 by Arthur Lyon Bowley.[32] The contract curve of the Edgeworth box (or more generally on any set of solutions to Edgeworth's problem for more actors) is referred to as the core of an economy.[33]

Edgeworth devoted considerable effort to insisting that mathematical proofs were appropriate for all schools of thought in economics. While at the helm of The Economic Journal, he published several articles criticizing the mathematical rigor of rival researchers, including Edwin Robert Anderson Seligman, a noted skeptic of mathematical economics.[34] The articles focused on a back and forth over tax incidence and responses by producers. Edgeworth noticed that a monopoly producing a good that had jointness of supply but not jointness of demand (such as first class and economy on an airplane, if the plane flies, both sets of seats fly with it) might actually lower the price seen by the consumer for one of the two commodities if a tax were applied. Common sense and more traditional, numerical analysis seemed to indicate that this was preposterous. Seligman insisted that the results Edgeworth achieved were a quirk of his mathematical formulation. He suggested that the assumption of a continuous demand function and an infinitesimal change in the tax resulted in the paradoxical predictions. Harold Hotelling later showed that Edgeworth was correct and that the same result (a "diminution of price as a result of the tax") could occur with a discontinuous demand function and large changes in the tax rate).[35]

Modern mathematical economics

In the late 1930s, economists saw the wider use of a broad array of mathematical tools, including convex sets and graph theory. Mathematicians began to discuss economic problems as a means to advance the state of pure mathematics in the same sense that solutions to problems in physics led to advancement in the underlying mathematics.[36]

Differential calculus

Main articles: Foundations of Economic Analysis and Differential calculusSee also: Pareto efficiency and Walrasian auctionVilfredo Pareto analyzed microeconomics by treating decisions by economic actors as attempts to change a given allotment of goods to another, more preferred allotment. Sets of allocations could then be treated as Pareto efficient (Pareto optimal is an equivalent term) when no exchanges could occur between actors that could make at least one individual better off without making any other individual worse off.[37] Pareto's proof is commonly conflated with Walrassian equilibrium or informally ascribed to Adam Smith's Invisible hand hypothesis.[38] Rather, Pareto's statement was the first formal assertion of what would be known as the first fundamental theorem of welfare economics.[39] These models lacked the inequalities of the next generation of mathematical economics.

In the landmark treatise Foundations of Economic Analysis (1947), Paul Samuelson identified a common paradigm and mathematical structure across multiple fields in the subject, building on previous work by Alfred Marshall. Foundations took mathematical concepts from physics and applied them to economic problems. This broad view (for example, comparing Le Chatelier's principle to tâtonnement) drives the fundamental premise of mathematical economics: systems of economic actors may be modeled and their behavior described much like any other system. This extension followed on the work of the marginalists in the previous century and extended it significantly. Samuelson approached the problems of applying individual utility maximization over aggregate groups with comparative statics, which compares two different equilibrium states after an exogenous change in a variable. This and other methods in the book provided the foundation for mathematical economics in the 20th century.[7][40]

Linear models

Restricted models of general equilibrium were formulated by John von Neumann in 1938: Unlike earlier versions, the models of von Neumann had inequality constraints. For his model of an expanding economy, von Neumann proved the existence and uniqueness of an equilibrium using his generalization of Brouwer's fixed point theorem. Von Neumann's model of an expanding economy considered the matrix pencil A - λ B with nonnegative matrices A and B; von Neumann sought probability vectors p and q and a positive number λ that would solve the complementarity equation

- pT (A - λ B) q = 0,

along with two inequality systems expressing economic efficiency. In this model, the (transposed) probability vector p represents the prices of the goods while the probability vector q represents the "intensity" at which the production process would run. The unique solution λ represents the rate of growth of the economy, which equals the interest rate. Proving the existence of a positive growth rate and proving that the growth rate equals the interest rate were remarkable achievements, even for von Neumann.[41][42][43] Von Neumann's results have been viewed as a special case of linear programming, where von Neumann's model uses only nonnegative matrices.[44] The study of von Neumann's model of an expanding economy continues to interest mathematical economists with interests in computational economics.[45][46][47]

Input-output economics

Main article: Input-output modelIn 1936, the Russian–born economist Wassily Leontief built his model of input-output analysis from the 'material balance' tables constructed by Soviet economists, which themselves followed earlier work by Austrian economists and the physiocrats. With his model, which described a system of production and demand processes, Leontief described how changes in demand in one economic sector would influence production in another.[48] In practice, Leontief estimated the coefficients of his simple models, to address economically interesting questions. In production economics, "Leontief technologies" produce outputs using constant proportions of inputs, regardless of the price of inputs, reducing the value of Leontief models for understanding economies but allowing their parameters to be estimated relatively easily. In contrast, the von Neumann model of an expanding economy allows for choice of techniques, but the coefficients must be estimated for each technology.[49][50]

Mathematical optimization

Main articles: Mathematical optimization and Dual problemSee also: Convexity in economics and Non-convexity (economics)Optimization problems run through modern economics, many with explicit economic or technical constraints. Optimality properties for an entire market system may be stated in mathematical terms, such as for the Arrow–Debreu model of general equilibrium (also discussed below).[51] More concretely, many problems are amenable to analytical (formulaic) solution. Many others may be sufficiently complex to require numerical methods of solution, aided by softwares.[52] Still others are complex but tractable enough to allow computable methods of solution, in particular computable general equilibrium models.[53]

Linear and nonlinear programming profoundly enriched microeconomics, which had earlier considered only equality constraints.[54] Many of the mathematical economists who received Nobel Prizes in Economics had conducted notable research using linear programming: Leonid Kantorovich, Leonid Hurwicz, Tjalling Koopmans, Kenneth J. Arrow, and Robert Dorfman, Paul Samuelson, and Robert Solow.[55] Both Kantorovich and Koopmans acknowledged that George B. Dantzig deserved to share their Nobel Prize for linear programming. Economists who conducted research in nonlinear programming also have won the Nobel prize, notably Ragnar Frisch in addition to Kantorovich, Hurwicz, Koopmans, Arrow, and Samuelson.

Linear optimization

Main articles: Linear programming and Simplex algorithmLinear programming was developed to aid the allocation of resources in firms and in industries during the 1930s in Russia and during the 1940s in the United States. During the Berlin airlift (1948), linear programming was used to plan the shipment of supplies to prevent Berlin from starving after the Soviet blockade.[56][57]

Nonlinear programming

See also: Nonlinear programming, Lagrangian multiplier, Karush–Kuhn–Tucker conditions, and Shadow priceExtensions to nonlinear optimization with inequality constraints were achieved in 1951 by Albert W. Tucker and Harold Kuhn, who considered the nonlinear optimization problem:

- Minimize f(x) subject to gi(x) ≤ 0 and hj(x) = 0 where

- f(.) is the function to be minimized

- gi(.) (j = 1, ..., m) are the functions of the m inequality constraints

- hj(.) (j = 1, ..., l) are the functions of the l equality constraints.

In allowing inequality constraints, the Kuhn–Tucker approach generalized the classic method of Lagrange multipliers, which (until then) had allowed only equality constraints.[58] The Kuhn–Tucker approach inspired further research on Lagrangian duality, including the treatment of inequality constraints.[59][60][61][62][63] The duality theory of nonlinear programming is particularly satisfactory when applied to convex minimization problems, which enjoy the convex-analytic duality theory of Fenchel and Rockafellar; this convex duality is particularly strong for polyhedral convex functions, such as those arising in linear programming. Lagrangian duality and convex analysis are used daily in operations research, in the scheduling of power plants, the planning of production schedules for factories, and the routing of airlines (routes, flights, planes, crews).[63][64]

Game theory

Main article: Game TheorySee also: Cooperative game, Noncooperative game, John von Neumann, Theory of Games and Economic Behavior, and John Forbes Nash, Jr.Working with Oskar Morgenstern on the theory of games, von Neumann declared that economic theory needed to use functional analytic methods, especially convex sets and topological fixed point theorem, rather than the traditional differential calculus, because the maximum–operator did not preserve differentiable functions. Continuing von Neumann's work in cooperative game theory, game theorists Lloyd S. Shapley, Martin Shubik, Hervé Moulin, Nimrod Megiddo, Bezalel Peleg influenced economic research in politics and economics. For example, research on the fair prices in cooperative games and fair values for voting games led to changed rules for voting in legislatures and for accounting for the costs in public–works projects. For example, cooperative game theory was used in designing the water distribution system of Southern Sweden and for setting rates for dedicated telephone lines in the USA.

Earlier neoclassical theory had bounded only the range of bargaining outcomes and in special cases, for example bilateral monopoly or along the contract curve of the Edgeworth box.[65] Von Neumann and Morgenstern's results were similarly weak. Following von Neumann's program, however, John Nash used fixed–point theory to prove conditions under which the bargaining problem and noncooperative games can generate a unique equilibrium solution.[66] Noncooperative game theory has been adopted as a fundamental aspect of industrial organization,[67] political economy,[68] experimental economics,[69] behavioral economics,[70] and information economics.[71] It has also given rise to the subject of mechanism design (sometimes called reverse game theory), which has private and public-policy applications as to ways of improving economic efficiency through incentives for information sharing.[72]

In 1994, Nash, John Harsanyi, and Reinhard Selten received the Nobel Memorial Prize in Economic Sciences their work on non–cooperative games. Harsanyi and Selten were awarded for their work on repeated games. Later work extended their results to computational methods of modeling.[73]

Agent-based computational economics

Agent-based computational economics is a recent approach that builds on game theory and advances in analytical and computational techniques to model economic systems as resulting from "purposeful agents who interact in space and time and whose micro-level interactions create emergent patterns."[74]

Functional analysis

See also: Functional analysis, Convex set, Supporting hyperplane, Hahn–Banach theorem, Fixed point theorem, and Dual spaceFollowing von Neumann's program, Kenneth Arrow and Gérard Debreu formulated abstract models of economic equilibria using convex sets and fixed–point theory. Introduced the Arrow-Debreu model in 1954, they proved the existence (but not the uniqueness) of an equilibrium and also proved that every Walras equilibrium is Pareto efficient; in general, equilibria need not be unique.[75] In their models, the ("primal") vector space represented quantitites while the "dual" vector space represented prices.[76]

In Russia, the mathematician Leonid Kantorovich developed economic models in partially ordered vector spaces, that emphasized the duality between quantities and prices.[77] Oppressed by communism, Kantorovich renamed prices as "objectively determined valuations" which were abbreviated in Russian as "o. o. o.", alluding to the difficulty of discussing prices in the Soviet Union.[76][78][79]

Even in finite dimensions, the concepts of functional analysis have illuminated economic theory, particularly in clarifying the role of prices as normal vectors to a hyperplane supporting a convex set, representing production or consumption possibilities. However, problems of describing optimization over time or under uncertainty require the use of infinite–dimensional function spaces, because agents are chosing among functions or stochastic processes.[76][80][81][82]

Variational calculus and optimal control

The problem of finding optimal functions is studied in variational calculus and in optimal control theory. Before the Second World War, Frank Ramsey and Harold Hotelling used the calculus of variations to find optimal solutions to dynamic economics problems.

Optimal control theory began to be used in addressing dynamic problems in economics, especially the economic growth models, soon after Richard Bellman's work on dynamic programming and after the publication of the English translation of the book by Pontryagin et al.[83] Applications of optimal control theory include those in economic growth, finance, inventories, and production for example.,[84] for example.

Differential renaissance

See also: Global analysis, Baire category, and Sard's lemmaAs discussed below, following John von Neumann's break-throughs in economics, and particularly after his introduction of functional analysis and topology in economic theory, advanced mathematical economics had fewer applications of differential calculus. In particular, general equilibrium theorists used general topology, convex geometry, and optimization theory more than differential calculus, because the approach of differential calculus had failed to establish the existence of an equilibrium.

However, the decline of differential calculus should not be exaggerated, because differential calculus has always been used in graduate training and in applications. Moreover, differential calculus has returned to the highest levels of mathematical economics, general equilibrium theory (GET), as practiced by the "GET-set" (the humorous designation due to Jacques H. Drèze). In the 1960s and 1970s, however, Gérard Debreu and Stephen Smale led a revival of the use of differential calculus in mathematical economics. In particular, they were able to prove the existence of a general equilibrium, where earlier writers had failed, because of their novel mathematics: Baire category from general topology and Sard's lemma from differential topology. Other economists asssociated with the use of differential analysis include Egbert Dierker, Andreu Mas-Colell, and Yves Balasko.[85][86] These advances have changed the traditional narrative of the history of mathematical economics, following von Neumann, which celebrated the abandonment of differential calculus.

The mathematicization of economics

The surface of the Volatility smile is a 3-D surface whereby the current market implied volatility (Z-axis) for all options on the underlier is plotted against strike price and time to maturity (X & Y-axes).[87]

The surface of the Volatility smile is a 3-D surface whereby the current market implied volatility (Z-axis) for all options on the underlier is plotted against strike price and time to maturity (X & Y-axes).[87]Over the course of the 20th century, articles in "core journals"[88] in economics have been almost exclusively written by economists in academia. As a result, much of the material transmitted in those journals relates to economic theory, and "economic theory itself has been continuously more abstract and mathematical."[89] A subjective assessment of mathematical techniques[90] employed in these core journals showed a decrease in articles that use neither geometric representations nor mathematical notation from 95% in 1892 to 5.3% in 1990.[91] A 2007 survey of ten of the top economic journals finds that only 5.8% of the articles published in 2003 and 2004 both lacked statistical analysis of data and lacked displayed mathematical expressions that were indexed with numbers at the margin of the page.[92]

Econometrics

Main article: EconometricsBetween the world wars, advances in mathematical statistics and a cadre of mathematically trained economists led to econometrics, which was the name proposed for the discipline of advancing economics by using mathematics and statistics. Within economics, "econometrics" has often been used for statistical methods in economics, rather than mathematical economics. Statistical econometrics features the application of linear regression and time series analysis to economic data.

Ragnar Frisch coined the word "econometrics" and helped to found both the Econometric Society in 1930 and the journal Econometrica in 1933.[93][94] A student of Frisch's, Trygve Haavelmo published The Probability Approach in Econometrics in 1944, where he asserted that precise statistical analysis could be used as a tool to validate mathematical theories about economic actors with data from complex sources.[95] This linking of statistical analysis of systems to economic theory was also promulgated by the Cowles Commission (now the Cowles Foundation) throughout the 1930s and 1940s.[96]

Earlier work in econometrics

The roots of modern econometrics can be traced to the American economist Henry L. Moore. Moore studied agricultural productivity and attempted to fit changing values of productivity for plots of corn and other crops to a curve using different values of elasticity. Moore made several errors in his work, some from his choice of models and some from limitations in his use of mathematics. The accuracy of Moore's models also was limited by the poor data for national accounts in the United States at the time. While his first models of production were static, in 1925 he published a dynamic "moving equilibrium" model designed to explain business cycles—this periodic variation from overcorrection in supply and demand curves is now known as the cobweb model. A more formal derivation of this model was made later by Nicholas Kaldor, who is largely credited for its exposition.[97]

Application

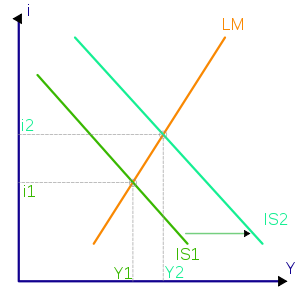

The IS/LM model is a Keynesian macroeconomic model designed to make predictions about the intersection of "real" economic activity (e.g. spending, income, savings rates) and decisions made in the financial markets (Money supply and Liquidity preference). The model is no longer widely taught at the graduate level but is common in undergraduate macroeconomics courses.[98]

The IS/LM model is a Keynesian macroeconomic model designed to make predictions about the intersection of "real" economic activity (e.g. spending, income, savings rates) and decisions made in the financial markets (Money supply and Liquidity preference). The model is no longer widely taught at the graduate level but is common in undergraduate macroeconomics courses.[98]Much of classical economics can be presented in simple geometric terms or elementary mathematical notation. Mathematical economics, however, conventionally makes use of calculus and matrix algebra in economic analysis in order to make powerful claims that would be more difficult without such mathematical tools. These tools are prerequisites for formal study, not only in mathematical economics but in contemporary economic theory in general. Economic problems often involve so many variables that mathematics is the only practical way of attacking and solving them. Alfred Marshall argued that every economic problem which can be quantified, analytically expressed and solved, should be treated by means of mathematical work.[99]

Economics has become increasingly dependent upon mathematical methods and the mathematical tools it employs have become more sophisticated. As a result, mathematics has become considerably more important to professionals in economics and finance. Graduate programs in both economics and finance require strong undergraduate preparation in mathematics for admission and, for this reason, attract an increasingly high number of mathematicians. Applied mathematicians apply mathematical principles to practical problems, such as economic analysis and other economics-related issues, and many economic problems are often defined as integrated into the scope of applied mathematics.[16]

This integration results from the formulation of economic problems as stylized models with clear assumptions and falsifiable predictions. This modeling may be informal or prosaic, as it was in Adam Smith's The Wealth of Nations, or it may be formal, rigorous and mathematical.

Broadly speaking, formal economic models may be classified as stochastic or deterministic and as discrete or continuous. At a practical level, quantitative modeling is applied to many areas of economics and several methodologies have evolved more or less independently of each other.[100]

- Stochastic models are formulated using stochastic processes. They model economically observable values over time. Most of econometrics is based on statistics to formulate and test hypotheses about these processes or estimate parameters for them. Between the World Wars, Herman Wold developed a representation of stationary stochastic processes in terms of autoregressive models and a determinist trend. Wold and Jan Tinbergen applied time-series analysis to economic data. Contemporary research on time series statistics consider additional formulations of stationary processes, such as autoregressive moving average models. More general models include autoregressive conditional heteroskedasticity (ARCH) models and generalized ARCH (GARCH) models.

- Non-stochastic mathematical models may be purely qualitative (for example, models involved in some aspect of social choice theory) or quantitative (involving rationalization of financial variables, for example with hyperbolic coordinates, and/or specific forms of functional relationships between variables). In some cases economic predictions of a model merely assert the direction of movement of economic variables, and so the functional relationships are used only in a qualitative sense: for example, if the price of an item increases, then the demand for that item will decrease. For such models, economists often use two-dimensional graphs instead of functions.

- Qualitative models are occasionally used. One example is qualitative scenario planning in which possible future events are played out. Another example is non-numerical decision tree analysis. Qualitative models often suffer from lack of precision.

Criticisms and defences

Adequacy of mathematics for qualitative and complicated economics

Friedrich Hayek contended that the use of formal techniques projects a scientific exactness that does not appropriately account for informational limitations faced by real economic agents. [101]

In an interview, the economic historian Robert Heilbroner stated:[102]

I guess the scientific approach began to penetrate and soon dominate the profession in the past twenty to thirty years. This came about in part because of the "invention" of mathematical analysis of various kinds and, indeed, considerable improvements in it. This is the age in which we have not only more data but more sophisticated use of data. So there is a strong feeling that this is a data-laden science and a data-laden undertaking, which, by virtue of the sheer numerics, the sheer equations, and the sheer look of a journal page, bears a certain resemblance to science . . . That one central activity looks scientific. I understand that. I think that is genuine. It approaches being a universal law. But resembling a science is different from being a science.Heilbroner stated that "some/much of economics is not naturally quantitative and therefore does not lend itself to mathematical exposition."[103]

Testing predictions of mathematical economics

Philosopher Karl Popper discussed the scientific standing of economics in the 1940s and 1950s. He argued that mathematical economics suffered from being tautological. In other words, insofar that economics became a mathematical theory, mathematical economics ceased to rely on empirical refutation but rather relied on mathematical proofs and disproof.[104] According to Popper, falsifiable assumptions can be tested by experiment and observation while unfalsifiable assumptions can be explored mathematically for their consequences and for their consistency with other assumptions.[105]

Sharing Popper's concerns about assumptions in economics generally, and not just mathematical economics, Milton Friedman declared that "all assumptions are unrealistic". Friedman proposed judging economic models by their predictive performance rather than by the match between their assumptions and reality.[106]

Mathematical economics as a form of pure mathematics

Considering mathematical economics, J.M. Keynes wrote in The General Theory:[107]

It is a great fault of symbolic pseudo-mathematical methods of formalising a system of economic analysis ... that they expressly assume strict independence between the factors involved and lose their cogency and authority if this hypothesis is disallowed; whereas, in ordinary discourse, where we are not blindly manipulating and know all the time what we are doing and what the words mean, we can keep ‘at the back of our heads’ the necessary reserves and qualifications and the adjustments which we shall have to make later on, in a way in which we cannot keep complicated partial differentials ‘at the back’ of several pages of algebra which assume they all vanish. Too large a proportion of recent ‘mathematical’ economics are merely concoctions, as imprecise as the initial assumptions they rest on, which allow the author to lose sight of the complexities and interdependencies of the real world in a maze of pretentious and unhelpful symbols.Defense of mathematical economics

In response to these criticisms, Paul Samuelson argued that mathematics is a language, repeating a thesis of Josiah Willard Gibbs. In economics, the language of mathematics is sometimes necessary for representing substantive problems. Moreover, mathematical economics has led to conceptual advances in economics.[108] In particular, Samuelson gave the example of microeconomics, writing that "few people are ingenious enough to grasp [its] more complex parts... without resorting to the language of mathematics, while most ordinary individuals can do so fairly easily with the aid of mathematics."[109]

Some economists state that mathematical economics deserves support just like other forms of mathematics, particularly its neighbors in mathematical optimization and mathematical statistics and increasingly in theoretical computer science. Mathematical economics and other mathematical sciences have a history in which theoretical advances have regularly contributed to the reform of the more applied branches of economics. In particular, following the program of John von Neumann, game theory now provides the foundations for describing much of applied economics, from statistical decision theory (as "games against nature") and econometrics to general equilibrium theory and industrial organization. In the last decade, with the rise of the internet, mathematical economicists and optimization experts and computer scientists have worked on problems of pricing for on-line services --- their contributions using mathematics from cooperative game theory, nondifferentiable optimization, and combinatorial games.

Robert M. Solow concluded that mathematical economics was the core "infrastructure" of contemporary economics:

Economics is no longer a fit conversation piece for ladies and gentlemen. It has become a technical subject. Like any technical subject it attracts some people who are more interested in the technique than the subject. That is too bad, but it may be inevitable. In any case, do not kid yourself: the technical core of economics is indispensable infrastructure for the political economy. That is why, if you consult [a reference in contemporary economics] looking for enlightenment about the world today, you will be led to technical economics, or history, or nothing at all.[110]

Mathematical economists

Prominent mathematical economists include, but are not limited to, the following (by century of birth).

19th century

20th century

- Charalambos D. Aliprantis

- R. G. D. Allen

- Maurice Allais

- Kenneth J. Arrow

- Robert J. Aumann

- Yves Balasko

- David Blackwell

- Lawrence E. Blume

- Graciela Chichilnisky

- George B. Dantzig

- Gérard Debreu

- Jacques H. Drèze

- David Gale

- Nicholas Georgescu-Roegen

- Roger Guesnerie

- Frank Hahn

- John C. Harsanyi

- John R. Hicks

- Werner Hildenbrand

- Harold Hotelling

- Leonid Hurwicz

- Leonid Kantorovich

- Tjalling Koopmans

- David M. Kreps

- Harold W. Kuhn

- Edmond Malinvaud

- Leonard J. Savage

- Herbert Scarf

- Reinhard Selten

- Amartya Sen

- Lloyd S. Shapley

- Stephen Smale

- Robert Solow

- Hugo F. Sonnenschein

- Albert W. Tucker

- Hirofumi Uzawa

- Robert B. Wilson

- Hermann Wold

- Nicholas C. Yannelis

Notes

- ^ a b Chiang, Alpha C.; and Kevin Wainwright (2005). Fundamental Methods of Mathematical Economics. McGraw-Hill Irwin. pp. 3–4. ISBN 0-07-010910-9. TOC.

- ^ Elaborated at JEL classification codes#Mathematical and quantitative methods JEL: C Subcategories.

- ^ Search of The New Palgrave Dictionary of Economics Online, "mathematical economics" "computational".

- ^ Varian, Hal (1997). "What Use Is Economic Theory?" in A. D'Autume and J. Cartelier, ed., Is Economics Becoming a Hard Science?, Edward Elgar. Pre-publication PDF. Retrieved 2008-04-01.

- ^ • As in Handbook of Mathematical Economics, 1st-page chapter links:

Arrow, Kenneth J., and Michael D. Intriligator, ed., (1981), v. 1

_____ (1982). v. 2

_____ (1986). v. 3

Hildenbrand, Werner, and Hugo Sonnenschein, ed. (1991). v. 4.

• Debreu, Gérard (1983). Mathematical Economics: Twenty Papers of Gerard Debreu, Contents.

• Glaister, Stephen (1984). Mathematical Methods for Economists, 3rd ed., Blackwell. Contents.

• Takayama, Akira (1985). Mathematical Economics, 2nd ed. Cambridge. Description and Contents.

• Michael Carter (2001). Foundations of Mathematical Economics, MIT Press. Description and Contents. - ^ Chiang, Alpha C. (1992). Elements of Dynamic Optimization, Waveland. TOC & Amazon.com link to inside, first pp.

- ^ a b c Samuelson, Paul ((1947) [1983]). Foundations of Economic Analysis. Harvard University Press. ISBN 0-674-31301-1.

- ^ • Debreu, Gérard ([1987] 2008). "mathematical economics," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract. (First published with revisions from 1986, "Theoretic Models: Mathematical Form and Economic Content," Econometrica, 54(6), pp. 1259-1270.)

• von Neumann, John, and Oskar Morgenstern (1944). Theory of Games and Economic Behavior. Princeton University Press. - ^ Schumpeter, J.A. (1954). Elizabeth B. Schumpeter. ed. History of Economic Analysis. New York, NY: Oxford University Press. pp. 209–212. ISBN 9780043300862. OCLC 13498913. http://books.google.com/?id=xjWiAAAACAAJ.

- ^ Schumpeter (1954) p. 212-215

- ^ Schnieder, Erich (1934). "Johann Heinrich von Thünen". Econometrica (The Econometric Society) 2 (1): 1–12. doi:10.2307/1907947. ISSN 0012-9682. JSTOR 1907947. OCLC 35705710.

- ^ Schumpeter (1954) p. 465-468

- ^ Philip Mirowski, 1991. "The When, the How and the Why of Mathematical Expression in the History of Economics Analysis," Journal of Economic Perspectives, 5(1) pp. 145-157.

- ^ Jevons, W.S. (1866). "Brief Account of a General Mathematical Theory of Political Economy," Journal of the Royal Statistical Society, XXIX (June) pp. 282-87. Read in Section F of the British Association, 1862. PDF.

- ^ Jevons, W. Stanley (1871). The Principles of Political Economy, pp. 4, 25.. http://books.google.com/books?id=Sw8ZAAAAYAAJ&printsec=frontcover&dq=%22The+Theory+of+Political+Economy,%22+jevons+1871#v=onepage&q=%22The%20Theory%20of%20Political%20Economy%2C%22%20jevons%201871&f=false.

- ^ a b Sheila C., Dow (1999-05-21). "The Use of Mathematics in Economics". ESRC Public Understanding of Mathematics Seminar. Birmingham: Economic and Social Research Council. http://www.ioe.ac.uk/esrcmaths/sheila1.html. Retrieved 2008-07-06.

- ^ While the concept of cardinality has fallen out of favor in neoclassical economics, the differences between cardinal utility and ordinal utility are minor for most applications.

- ^ a b Nicola, PierCarlo (2000). Mainstream Mathermatical Economics in the 20th Century. Springer. pp. 4. ISBN 9783540670841. http://books.google.com/?id=KR0Rbi8o4QQC. Retrieved 2008-08-21.

- ^ Augustin Cournot (1838, tr. 1897) Researches nto the Mathematical Principles of Wealth. Links to description and chapters.

- ^ a b Hotelling, Harold (1990). "Stability in Competition". In Darnell, Adrian C.. The Collected Economics Articles of Harold Hotelling. Springer. pp. 51, 52. ISBN 3540970118. OCLC 20217006. http://books.google.com/?id=dYbbHQAACAAJ. Retrieved 2008-08-21.

- ^ "Antoine Augustin Cournot, 1801-1877". The History of Economic Thought Website. The New School for Social Research. http://cepa.newschool.edu/het/profiles/cournot.htm. Retrieved 2008-08-21.

- ^ Gibbons, Robert (1992). Game Theory for Applied Economists. Princeton, New Jersey: Princeton University Press. pp. 14, 15. ISBN 0691003955. http://books.google.com/?id=_6qgHgAACAAJ.

- ^ Nicola, p. 9-12

- ^ Edgeworth, Francis Ysidro (September 5, 1889). "The Mathematical Theory of Political Economy: Review of Léon Walras, Éléments d'économie politique pure" (PDF). Nature 40 (1036): 434–436. doi:10.1038/040434a0. ISSN 0028-0836. http://cepa.newschool.edu/het/texts/edgeworth/edgewalras89.pdf. Retrieved 2008-08-21.

- ^ Nicholson, Walter; Snyder, Christopher, p. 350-353.

- ^ Dixon, Robert. "Walras Law and Macroeconomics". Walras Law Guide. Department of Economics, University of Melbourne. Archived from the original on April 17, 2008. http://web.archive.org/web/20080417102559/http://www.economics.unimelb.edu.au/rdixon/wlaw.html. Retrieved 2008-09-28.

- ^ Dixon, Robert. "A Formal Proof of Walras Law". Walras Law Guide. Department of Economics, University of Melbourne. Archived from the original on April 30, 2008. http://web.archive.org/web/20080430033548/http://www.economics.unimelb.edu.au/rdixon/walproof.html. Retrieved 2008-09-28.

- ^ Rima, Ingrid H. (1977). "Neoclassicism and Dissent 1890-1930". In Weintraub, Sidney. Modern Economic Thought. University of Pennsylvania Press. pp. 10, 11. ISBN 0812277120. http://books.google.com/?id=s7cJAAAAIAAJ&printsec=find&pg=PR5=onepage&q#v=onepage&q&f=false.

- ^ Heilbroner, Robert L. (1953 [1999]). The Worldly Philosophers (Seventh ed.). New York, NY: Simon and Schuster. pp. 172–175, 313. ISBN 9780684862149. http://books.google.com/?id=N_3cj4urgJcC.

- ^ Edgeworth, Francis Ysidro (1881 [1961]). Mathematical Psychics. London: Kegan Paul [A. M. Kelley]. pp. 15–19. http://books.google.com/?id=Q4WCGAAACAAJ.

- ^ Nicola, p. 14, 15, 258-261

- ^ Bowley, Arthur Lyon (1924 [1960]). The Mathematical Groundwork of Economics: an Introductory Treatise. Oxford: Clarendon Press [Kelly]. http://books.google.com/?id=_cgkAAAAMAAJ.

- ^ Gillies, D. B. (1969). "Solutions to general non-zero-sum games". In Tucker, A. W. & Luce, R. D.. Contributions to the Theory of Games. Annals of Mathematics. 40. Princeton, New Jersey: Princeton University Press. pp. 47–85. ISBN 9780691079370. http://books.google.com/?id=9lSVFzsTGWsC.

- ^ Moss, Lawrence S. (2003). "The Seligman-Edgeworth Debate about the Analysis of Tax Incidence: The Advent of Mathematical Economics, 1892–1910". History of Political Economy (Duke University Press) 35 (2): 207, 212, 219, 234–237. doi:10.1215/00182702-35-2-205. ISSN 0018-2702.

- ^ Hotelling, Harold (1990). "Note on Edgeworth's Taxation Phenomenon and Professor Garver's Additional Condition on Demand Functions". In Darnell, Adrian C.. The Collected Economics Articles of Harold Hotelling. Springer. pp. 94–122. ISBN 3540970118. OCLC 20217006. http://books.google.com/?id=dYbbHQAACAAJ. Retrieved 2008-08-26.

- ^ Herstein, I.N. (October 1953). "Some Mathematical Methods and Techniques in Economics". Quarterly of Applied Mathematics (American Mathematical Society) 11 (3): 249, 252, 260. ISSN 1552-4485.

- ^ Nicholson, Walter; Snyder, Christopher (2007). "General Equilibrium and Welfare". Intermediate Microeconomics and Its Applications (10th ed.). Thompson. pp. 364, 365. ISBN 0324319681.

- ^ Jolink, Albert (2006). "What Went Wrong with Walras?". In Backhaus, Juergen G.; Maks, J.A. Hans. From Walras to Pareto. The European Heritage in Economics and the Social Sciences. IV. Springer. doi:10.1007/978-0-387-33757-9_6. ISBN 978-0-387-33756-2.

• Blaug, Mark (2007). "The Fundamental Theorems of Modern Welfare Economics, Historically Contemplated". History of Political Economy (Duke University Press) 39 (2): 186–188. doi:10.1215/00182702-2007-001. ISSN 0018-2702. - ^ Blaug (2007), p. 185, 187

- ^ Metzler, Lloyd (1948). "Review of Foundations of Economic Analysis". American Economic Review (The American Economic Review, Vol. 38, No. 5) 38 (5): 905–910. ISSN 0002-8282. JSTOR 1811704.

- ^ For this problem to have a unique solution, it suffices that the nonnegative matrices A and B satisfy an irreducibility condition, generalizing that of the Perron–Frobenius theorem of nonnegative matrices, which considers the (simplified) eigenvalue problem

- A - λ I q = 0,

- ^ David Gale. The theory of linear economic models. McGraw-Hill, New York, 1960.

- ^ Morgenstern, Oskar; Thompson, Gerald L. (1976). Mathematical theory of expanding and contracting economies. Lexington Books. Lexington, Massachusetts: D. C. Heath and Company. pp. xviii+277.

- ^ Alexander Schrijver, Theory of Linear and Integer Programming. John Wiley & sons, 1998, ISBN 0-471-98232-6.

- ^ •Rockafellar, R. Tyrrell (1967). Monotone processes of convex and concave type. Memoirs of the American Mathematical Society. Providence, R.I.: American Mathematical Society. pp. i+74.

• Rockafellar, R. T. (1974). "Convex algebra and duality in dynamic models of production". In Josef Loz and Maria Loz. Mathematical models in economics (Proc. Sympos. and Conf. von Neumann Models, Warsaw, 1972). Amsterdam: North-Holland and Polish Adademy of Sciences (PAN). pp. 351–378.

•Rockafellar, R. T.]] (1970 (Reprint 1997 as a Princeton classic in mathematics)). Convex analysis. Princeton, NJ: Princeton University Press. - ^ Kenneth Arrow, Paul Samuelson, John Harsanyi, Sidney Afriat, Gerald L. Thompson, and Nicholas Kaldor. (1989). Mohammed Dore, Sukhamoy Chakravarty, Richard Goodwin. ed. John Von Neumann and modern economics. Oxford:Clarendon. pp. 261.

- ^ Chapter 9.1 "The von Neumann growth model" (pages 277–299): Yinyu Ye. Interior point algorithms: Theory and analysis. Wiley. 1997.

- ^ Screpanti, Ernesto; Zamagni, Stefano (1993). An Outline of the History of Economic Thought. New York, NY: Oxford University Press. pp. 288–290. ISBN 0198283709. OCLC 57281275.

- ^ David Gale. The theory of linear economic models. McGraw-Hill, New York, 1960.

- ^ Morgenstern, Oskar; Thompson, Gerald L. (1976). Mathematical theory of expanding and contracting economies. Lexington Books. Lexington, Massachusetts: D. C. Heath and Company. pp. xviii+277.

- ^ • John Geanakoplos ((1987] 2008). "Arrow–Debreu model of general equilibrium," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

• Arrow, Kenneth J., and Gerard Debreu (1954). "Existence of an Equilibrium for a Competitive Economy," Econometrica 22(3), pp. 265-290. - ^ Schmedders, Karl (2008). "numerical optimization methods in economics," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

- ^ • Scarf, Herbert E. (2008). "computation of general equilibria," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

• Kubler, Felix (2008). "computation of general equilibria (new developments)," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract. - ^ Nicola, p. 133

- ^ Dorfman, Robert, Paul A. Samuelson, and Robert M. Solow (1958). Linear Programming and Economic Analysis. McGraw–Hill. Chapter-preview links.

- ^ M. Padberg, Linear Optimization and Extensions, Second Edition, Springer-Verlag, 1999.

- ^ Dantzig, George B. ([1987] 2008). "linear programming," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

- ^ Kuhn, H. W.; Tucker, A. W. (1951). "Nonlinear programming". Proceedings of 2nd Berkeley Symposium. Berkeley: University of California Press. pp. 481–492.

- ^ Bertsekas, Dimitri P. (1999). Nonlinear Programming (Second ed.). Cambridge, MA.: Athena Scientific. ISBN 1-886529-00-0.

- ^ Vapnyarskii, I.B. (2001), "Lagrange multipliers", in Hazewinkel, Michiel, Encyclopaedia of Mathematics, Springer, ISBN 978-1556080104, http://eom.springer.de/L/l057190.htm.

- ^ • Lasdon, Leon S. (1970). Optimization theory for large systems. Macmillan series in operations research. New York: The Macmillan Company. pp. xi+523. MR337317.

• Lasdon, Leon S. (2002). Optimization theory for large systems (reprint of the 1970 Macmillan ed.). Mineola, New York: Dover Publications, Inc.. pp. xiii+523. MR1888251. - ^ Hiriart-Urruty, Jean-Baptiste; Lemaréchal, Claude (1993). "XII Abstract duality for practitioners". Convex analysis and minimization algorithms, Volume II: Advanced theory and bundle methods. Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. 306. Berlin: Springer-Verlag. pp. 136–193 (and Bibliographical comments on pp. 334–335). ISBN 3-540-56852-2.

- ^ a b Lemaréchal, Claude (2001). "Lagrangian relaxation". In Michael Jünger and Denis Naddef. Computational combinatorial optimization: Papers from the Spring School held in Schloß Dagstuhl, May 15–19, 2000. Lecture Notes in Computer Science. 2241. Berlin: Springer-Verlag. pp. 112–156. doi:10.1007/3-540-45586-8_4. ISBN 3-540-42877-1. MRdoi:[http://dx.doi.org/10.1007%2F3-540-45586-8_4 10.1007/3-540-45586-8_4 1900016.[[Digital object identifier|doi]]:[http://dx.doi.org/10.1007%2F3-540-45586-8_4 10.1007/3-540-45586-8_4]].

- ^ Intriligator, Michael D. (2008). "nonlinear programming," The New Palgrave Dictionary of Economics, 2nd Edition. TOC.

- ^ Creedy, John (2008). "Francis Ysidro (1845–1926)," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

- ^ • Nash, John F., Jr. (1950). "The Bargaining Problem," Econometrica, 18(2), pp. 155-162.

• Serrano, Roberto (2008). "bargaining," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract. - ^ • Tirole, Jean (1988). The Theory of Industrial Organization, MIT Press. Description and chapter-preview links, pp. vii-ix, "General Organization," pp. 5-6, and "Non-Cooperative Game Theory: A User's Guide Manual,' " ch. 11, pp. 423-59.

• Bagwell, Kyle, and Asher Wolinsky (2002). "Game theory and Industrial Organization," ch. 49, Handbook of Game Theory with Economic Applications, v. 3, pp. 1851-1895. - ^ • Martin Shubik (1981). "Game Theory Models and Methods in Political Economy," in Handbook of Mathematical Economics, , v. 1, pp. 285-330.

- ^ • Smith, Vernon L., 1992. "Game Theory and Experimental Economics: Beginnings and Early Influences," in E. R. Weintraub, ed., Towards a History of Game Theory, pp. 241-282.

• Plott, Charles R. and Vernon L. Smith, 2008. Handbook of Experimental Economics Results, v. 1, Elsevier, ch. 45-66 links. - ^ From The New Palgrave Dictionary of Economics (2008), 2nd Edition:

• Faruk Gul. "behavioural economics and game theory." Abstract.

• Colin F. Camerer. "behavioral game theory." Abstract. - ^ • Eric Rasmusen (2007). Games and Information, 4th ed. Description and chapter-preview links.

• R. Aumann and S. Hart, ed. (1992, 2002). Handbook of Game Theory with Economic Applications v. 1, links at ch. 3-6 and v. 3, ch. 43. - ^ From The New Palgrave Dictionary of Economics (2008), 2nd Edition:

• Roger B. Myerson. "mechanism design." Abstract.

• _____. "revelation principle." Abstract. - ^ Halpernby, Joseph Y. (2008). "computer science and game theory," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.]

- ^ • In Scott E. Page (2008), "agent-based models," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

• Alan Kirman (2008). "economy as a complex system," The New Palgrave Dictionary of Economics , 2nd Edition. Abstract.

• Leigh Tesfatsion (2006), "Agent-Based Computational Economics: A Constructive Approach to Economic Theory," pp. 831-880, in Leigh Tesfatsion and Kenneth Judd, ed., Handbook of Computational Economics, ch. 16, v. 2. Description & and chapter-preview links. - ^ Weintraub, E. Roy (1977). "General Equilibrium Theory". In Weintraub, Sidney. Modern Economic Thought. University of Pennsylvania Press. pp. 107–109. ISBN 0812277120. http://books.google.com/?id=JDqAAAAAIAAJ.

• Arrow, Kenneth J.; Debreu, Gérard (1954). "Existence of an equilibrium for a competitive economy". Econometrica (The Econometric Society) 22 (3): 265–290. doi:10.2307/1907353. ISSN 0012-9682. JSTOR 1907353. - ^ a b c Kantorovich, Leonid and Victor Polterovich. "Functional analysis." The New Palgrave Dictionary of Economics. Second Edition. Eds. Steven N. Durlauf and Lawrence E. Blume. Palgrave Macmillan, 2008. The New Palgrave Dictionary of Economics Online. Palgrave Macmillan. 15 February 2011 <http://www.dictionaryofeconomics.com/article?id=pde2008_F000236> doi:10.1057/9780230226203.0608

- ^ Kantorovich, L. V (1990). ""My journey in science (supposed report to the Moscow Mathematical Society)" [expanding Russian Math. Surveys 42 (1987), no. 2, pp. 233–270]". In Lev J. Leifman. Functional analysis, optimization, and mathematical economics: A collection of papers dedicated to the memory of Leonid Vitalʹevich Kantorovich. New York: The Clarendon Press, Oxford University Press. pp. 8–45. ISBN 0-19-505729-5. MR898626.

- ^ Page 406: Polyak, B. T. (2002). "History of mathematical programming in the USSR: Analyzing the phenomenon (Chapter 3 The pioneer: L. V. Kantorovich, 1912–1986, pp. 405–407)". Mathematical Programming 91 (ISMP 2000, Part 1 (Atlanta, GA)): pp. 401–416. doi:10.1007/s101070100258. MR1888984.

- ^ "Leonid Vitaliyevich Kantorovich — Prize Lecture ("Mathematics in economics: Achievements, difficulties, perspectives")". Nobelprize.org. http://nobelprize.org/nobel_prizes/economics/laureates/1975/kantorovich-lecture.html. Retrieved 12 Dec 2010.

- ^ Aliprantis, Charalambos D.; Brown, Donald J.; Burkinshaw, Owen (1990). Existence and optimality of competitive equilibria. Berlin: Springer–Verlag. pp. xii+284. ISBN 3-540-52866-0. MR1075992.

- ^ Rockafellar, R. Tyrrell. Conjugate duality and optimization. Lectures given at the Johns Hopkins University, Baltimore, Md., June, 1973. Conference Board of the Mathematical Sciences Regional Conference Series in Applied Mathematics, No. 16. Society for Industrial and Applied Mathematics, Philadelphia, Pa., 1974. vi+74 pp.

- ^ Lester G. Telser and Robert L. Graves Functional Analysis in Mathematical Economics: Optimization Over Infinite Horizons 1972. University of Chicago Press, 1972, ISBN 978-0-226-79190-6.

- ^ Pontryagin, L. S.; Boltyanski, V. G., Gamkrelidze, R. V., Mischenko, E. F. (1962). The Mathematical Theory of Optimal Processes. New York, NY: Wiley. ISBN 68981.

- ^ Shell, K., ed. (1967). Essays on the Optimal Economic Growth. Cambridge, MA: The MIT Press. ISBN 0262190362.]

• Arrow, K. J.; Kurz, M. (1970). Public Investment, the Rate of Return, and Optimal Fiscal Policy. Baltimore, MD: The Johns Hopkins Press. ISBN 0801811244. Abstract.

• Sethi, S. P.; Thompson, G. L. (2000). Optimal Control Theory: Applications to Management Science and Economics, Second Edition. New York, NY: Springer. ISBN 0792386086. Scroll to chapter-preview links. - ^ Mas-Colell, Andreu (1985). The Theory of general economic equilibrium: A differentiable approach. Econometric Society monographs. Cambridge UP. ISBN 0-521-26514-2. MR1113262.

- ^ Yves Balasko. Foundations of the Theory of General Equilibrium, 1988, ISBN 0-12-076975-1.

- ^ Brockhaus, Oliver; Farkas, Michael; Ferraris, Andrew; Long, Douglas; Overhaus, Marcus (2000). Equity Derivatives and Market Risk Models. Risk Books. pp. 13–17. ISBN 9781899332878. http://books.google.com/?id=JGZPAAAAMAAJ. Retrieved 2008-08-17.

- ^ Liner, Gaines H. (2002). "Core Journals in Economics". Economic Inquiry (Oxford University Press) 40 (1): 140. doi:10.1093/ei/40.1.138.

- ^ Stigler, George J.; Stigler, Steven J.; Friedland, Claire (April 1995). "The Journals of Economics". The Journal of Political Economy (The University of Chicago Press) 103 (2): 339. doi:10.1086/261986. ISSN 0022-3808. JSTOR 2138643.

- ^ Stigler et al. reviewed journal articles in core economic journals (as defined by the authors but meaning generally non-specialist journals) throughout the 20th century. Journal articles which at any point used geometric representation or mathematical notation were noted as using that level of mathematics as its "highest level of mathematical technique". The authors refer to "verbal techniques" as those which conveyed the subject of the piece without notation from geometry, algebra or calculus.

- ^ Stigler et al., p. 342

- ^ Sutter, Daniel and Rex Pjesky. "Where Would Adam Smith Publish Today?: The Near Absence of Math-free Research in Top Journals" (May 2007). [1]

- ^ Arrow, Kenneth J. (April 1960). "The Work of Ragnar Frisch, Econometrician". Econometrica (Blackwell Publishing) 28 (2): 175–192. doi:10.2307/1907716. ISSN 0012-9682. JSTOR 1907716.

- ^ Bjerkholt, Olav (July 1995). "Ragnar Frisch, Editor of Econometrica 1933-1954". Econometrica (Blackwell Publishing) 63 (4): 755–765. doi:10.2307/2171799. ISSN 0012-9682. JSTOR 1906940.

- ^ Lange, Oskar (1945). "The Scope and Method of Economics". Review of Economic Studies (The Review of Economic Studies Ltd.) 13 (1): 19–32. doi:10.2307/2296113. ISSN 0034-6527. JSTOR 2296113.

- ^ Aldrich, John (January 1989). "Autonomy". Oxford Economic Papers (Oxford University Press) 41 (1, History and Methodology of Econometrics): 15–34. ISSN 0030-7653. JSTOR 2663180.

- ^ Epstein, Roy J. (1987). A History of Econometrics. Contributions to Economic Analysis. North-Holland. pp. 13–19. ISBN 9780444702678. OCLC 230844893.

- ^ Colander, David C. (2004). "The Strange Persistence of the IS-LM Model". History of Political Economy (Duke University Press) 36 (Annual Supplement): 305–322. doi:10.1215/00182702-36-Suppl_1-305. ISSN 0018-2702.

- ^ Brems, Hans (Oct., 1975). "Marshall on Mathematics". Journal of Law and Economics (University of Chicago Press) 18 (2): 583–585. doi:10.1086/466825. ISSN 0022-2186. JSTOR 725308.

- ^ Frigg, R.; Hartman, S. (February 27, 2006). Edward N. Zalta. ed. Models in Science. Stanford Encyclopedia of Philosophy. Stanford, CA: The Metaphysics Research Lab. ISSN 1095-5054. http://plato.stanford.edu/entries/models-science/#OntWhaMod. Retrieved 2008-08-16.

- ^ Hayek, Friedrich (September 1945). "The Use of Knowledge in Society". American Economic Review 35 (4): 519–530. JSTOR 1809376.

- ^ Heilbroner, Robert (May–June 1999). "The end of the Dismal Science?". Challenge Magazine. http://findarticles.com/p/articles/mi_m1093/is_3_42/ai_54682627/print.

- ^ Beed & Owen, 584

- ^ Boland, L. A. (2007). "Seven Decades of Economic Methodology". In I. C. Jarvie, K. Milford, D.W. Miller. Karl Popper:A Centenary Assessment. London: Ashgate Publishing. pp. 219. ISBN 9780754653752. http://books.google.com/?id=w-BEoTj0axoC. Retrieved 2008-06-10.

- ^ Beed, Clive; Kane, Owen (1991). "What Is the Critique of the Mathematization of Economics?". Kyklos 44 (4): 581–612. doi:10.1111/j.1467-6435.1991.tb01798.x.

- ^ Friedman, Milton (1953). Essays in Positive Economics. Chicago: University of Chicago Press. pp. 30, 33, 41. ISBN 9780226264035. http://books.google.com/?id=rSGekjfpf4cC.

- ^ Keynes, John Maynard (1936). The General Theory of Employment, Interest and Money. Cambridge: Macmillan. pp. 297. ISBN 0333107292. http://www.marxists.org/reference/subject/economics/keynes/general-theory/ch21.htm.

- ^ Paul A. Samuelson (1952). "Economic Theory and Mathematics — An Appraisal," American Economic Review, 42(2), pp. 56, 64-65 (press +).

- ^ D.W. Bushaw and R.W. Clower (1957). Introduction to Mathematical Economics, p. vii.

- '^ Solow, Robert M. (20 March 1988). "The Wide, Wide World Of Wealth (The New Palgrave: A Dictionary of Economics. Edited by John Eatwell, Murray Milgate and Peter Newman. Four volumes. 4,103 pp. New York: Stockton Press. $650)". New York Times. http://www.nytimes.com/1988/03/20/books/the-wide-wide-world-of-wealth.html?scp=1.

External links

- Journal of Mathematical Economics Aims & Scope

- Mathematical Economics and Financial Mathematics at the Open Directory Project

Categories:- Applied mathematics

- Mathematical economics

- Mathematical and quantitative methods (economics)

- Economic methodology

Wikimedia Foundation. 2010.