- Cobweb model

-

The cobweb model or cobweb theory is an economic model that explains why prices might be subject to periodic fluctuations in certain types of markets. It describes cyclical supply and demand in a market where the amount produced must be chosen before prices are observed. Producers' expectations about prices are assumed to be based on observations of previous prices. Nicholas Kaldor analyzed the model in 1934, coining the term 'cobweb theorem' (see Kaldor, 1938 and Pashigian, 2008), citing previous analyses in German by Henry Schultz and U. Ricci.

Contents

The model

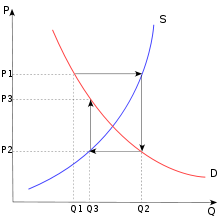

The convergent case: each new outcome is successively closer to the intersection of supply and demand.

The convergent case: each new outcome is successively closer to the intersection of supply and demand.

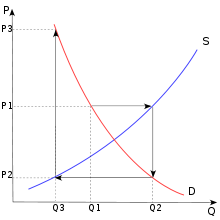

The divergent case: each new outcome is successively further from the intersection of supply and demand.

The divergent case: each new outcome is successively further from the intersection of supply and demand.The cobweb model is based on a time lag between supply and demand decisions. Agricultural markets are a context where the cobweb model might apply, since there is a lag between planting and harvesting (Kaldor, 1934, p. 133-134 gives two agricultural examples: rubber and corn). Suppose for example that as a result of unexpectedly bad weather, farmers go to market with an unusually small crop of strawberries. This shortage, equivalent to a leftward shift in the market's supply curve, results in high prices. If farmers expect these high price conditions to continue, then in the following year, they will raise their production of strawberries relative to other crops. Therefore when they go to market the supply will be high, resulting in low prices. If they then expect low prices to continue, they will decrease their production of strawberries for the next year, resulting in high prices again.

This process is illustrated by the diagrams on the right. The equilibrium price is at the intersection of the supply and demand curves. A poor harvest in period 1 means supply falls to Q1, so that prices rise to P1. If producers plan their period 2 production under the expectation that this high price will continue, then the period 2 supply will be higher, at Q2. Prices therefore fall to P2 when they try to sell all their output. As this process repeats itself, oscillating between periods of low supply with high prices and then high supply with low prices, the price and quantity trace out a spiral. They may spiral inwards, as in the top figure, in which case the economy converges to the equilibrium where supply and demand cross; or they may spiral outwards, with the fluctuations increasing in magnitude.

Simplifying, the cobweb model can have two main types of outcomes:

- If the supply curve is steeper than the demand curve, then the fluctuations decrease in magnitude with each cycle, so a plot of the prices and quantities over time would look like an inward spiral, as shown in the first diagram. This is called the stable or convergent case.

- If the slope of the supply curve is less than the absolute value of the slope of the demand curve, then the fluctuations increase in magnitude with each cycle, so that prices and quantities spiral outwards. This is called the unstable or divergent case.

Two other possibilities are:

- Fluctuations may also remain of constant magnitude, so a plot of the outcomes would produce a simple rectangle, if the supply and demand curves have exactly the same slope (in absolute value).

- If the supply curve is less steep than the demand curve near the point where the two curves cross, but more steep when we move sufficiently far away, then prices and quantities will spiral away from the equilibrium price but will not diverge indefinitely; instead, they may converge to a limit cycle.

In either of the first two scenarios, the combination of the spiral and the supply and demand curves often looks like a cobweb, hence the name of the theory.

Elasticities versus slopes

The outcomes of the cobweb model are stated above in terms of slopes, but they are more commonly described in terms of elasticities. In terms of slopes, the convergent case requires that the slope of the supply curve be greater than the absolute value of the slope of the demand curve:

left|\frac{dP^D}{dQ^D}\right|." border="0">

left|\frac{dP^D}{dQ^D}\right|." border="0">

In standard terminology from microeconomics, define the elasticity of supply as

, and the elasticity of demand as

, and the elasticity of demand as  . If we evaluate these two elasticities at the equilibrium point, that is PS = PD = P > 0 and QS = QD = Q > 0, then we see that the convergent case requires

. If we evaluate these two elasticities at the equilibrium point, that is PS = PD = P > 0 and QS = QD = Q > 0, then we see that the convergent case requireswhereas the divergent case requires

left|\frac{dQ^D/Q}{dP^D/P}\right|." border="0">

left|\frac{dQ^D/Q}{dP^D/P}\right|." border="0">

In words, the convergent case occurs when the demand curve is more elastic than the supply curve, at the equilibrium point. The divergent case occurs when the supply curve is more elastic than the demand curve, at the equilibrium point (see Kaldor, 1934, page 135, propositions (i) and (ii).)

Role of expectations

One reason to be skeptical about this model's predictions is that it assumes producers are extremely shortsighted. Assuming that farmers look back at the most recent prices in order to forecast future prices might seem very reasonable, but this backward-looking forecasting (which is called adaptive expectations) turns out to be crucial for the model's fluctuations. When farmers expect high prices to continue, they produce too much and therefore end up with low prices, and vice versa.

In the stable case, this may not be an unbelievable outcome, since the farmers' prediction errors (the difference between the price they expect and the price that actually occurs) become smaller every period. In this case, after several periods prices and quantities will come close to the point where supply and demand cross, and predicted prices will be very close to actual prices. But in the unstable case, the farmers' errors get larger every period. This seems to indicate that adaptive expectations is a misleading assumption: how could farmers fail to notice that last period's price is not a good predictor of this period's price?

The fact that agents with adaptive expectations may make ever-increasing errors over time has led many economists to conclude that it is better to assume rational expectations, that is, expectations consistent with the actual structure of the economy. However, the rational expectations assumption is controversial since it may exaggerate agents' understanding of the economy. The cobweb model serves as one of the best examples to illustrate why understanding expectation formation is so important for understanding economic dynamics, and also why expectations are so controversial in recent economic theory.

Evidence

Livestock herds

The cobweb model has been interpreted as an explanation of fluctuations in various livestock markets, like those documented by Arthur Hanau in German hog markets; see Pork cycle. However, Rosen et al. (1994) proposed an alternative model which showed that because of the three-year life cycle of beef cattle, cattle populations would fluctuate over time even if ranchers had perfectly rational expectations.

Air transport

In the air transport industry, high surplus capacity drives down prices, which causes demand to grow; when capacity utilisation becomes much higher, carriers may have the confidence to order many new aircraft; but there can be a substantial delay until the aircraft enter service, and when they arrive, this creates surplus capacity, pushing down prices again...[1]

Human experimental data

In 1989, Wellford conducted twelve experimental sessions each conducted with five participants over thirty periods simulating the stable and unstable cases. Her results show that the unstable case did not result in the divergent behavior we see with cobweb expectations but rather the participants converged toward the rational expectations equilibrium. However, the price path variance in the unstable case was greater than that in the stable case (and the difference was shown to be statistically significant).

One way of interpreting these results is to say that in the long run, the participants behaved as if they had rational expectations, but that in the short run they made mistakes. These mistakes caused larger fluctuations in the unstable case than in the stable case.

References

- W. Nicholson, Microeconomic Theory, 7th ed., Ch. 17, pp. 524–538. Dryden Press: ISBN 0030244749.

- J. Arifovic, 'Genetic Algorithm Learning and the Cobweb Model ', Journal of Economic Dynamics and Control, vol. 18, Issue 1, (January 1994), 3-28.

- A. Hanau (1928), 'Die Prognose der Schweinepreise'. In: Vierteljahreshefte zur Konjunkturforschung, Verlag Reimar Hobbing, Berlin.

- N. Kaldor, 'The Cobweb Theorem', Quarterly Journal of Economics, Vol. 52, No. 2 (February, 1938), pp. 255–280.

- N. Kaldor, 'A Classificatory Note on the Determination of Equilibrium', Review of Economic Studies, vol I (February, 1934), 122-36. (See especially pages 133-135.)

- M. Nerlove, 'Adaptive Expectations and Cobweb Phenomena', Quarterly Journal of Economics, vol. lxxii (1958), 227-40.

- C.P. Wellford, 'A Laboratory Analysis of Price Dynamics and Expectations in the Cobweb Model', Discussion Paper 89-15 (University of Arizona, Tucson, AZ).

- J.F. Muth, 'Rational Expectations and the Theory of Price Movements', Econometrica, vol. 29 (1961), 315-35.

- B.P. Pashigian (2008), 'Cobweb theorem', The New Palgrave Dictionary of Economics, 2nd edition.

- S. Rosen, K. Murphy, and J. Scheinkman, 'Cattle cycles', Journal of Political Economy, vol. 102 (1994), pp. 468–92.

- U. Ricci (1930), 'Die synthetische Ökonomie von Henry Ludwell Moore', Zeitschrift für Nationalökonomie, page 649.

- H. Schultz, Der Sinn der statistischen Nachfragekurven, page 34.

- ^ "Capacity caution". 2011-05-26. http://www.flightglobal.com/articles/2011/05/26/357129/capacity-caution.html. Retrieved 2011-05-26.

See also

Categories:- Economic theories

- Economics models

Wikimedia Foundation. 2010.