- Oligopoly

-

An oligopoly is a market form in which a market or industry is dominated by a small number of sellers (oligopolists). The word is derived, by analogy with "monopoly", from the Greek ὀλίγοι (oligoi) "few" + πόλειν (pólein) "to sell". Because there are few sellers, each oligopolist is likely to be aware of the actions of the others. The decisions of one firm influence, and are influenced by, the decisions of other firms. Strategic planning by oligopolists needs to take into account the likely responses of the other market participants.

Contents

Description

Oligopoly is a common market form. As a quantitative description of oligopoly, the four-firm concentration ratio is often utilized. This measure expresses the market share of the four largest firms in an industry as a percentage. For example, as of fourth quarter 2008, Verizon, AT&T, Sprint, Nextel, and T-Mobile together control 89% of the US cellular phone market.

Oligopolistic competition can give rise to a wide range of different outcomes. In some situations, the firms may employ restrictive trade practices (collusion, market sharing etc.) to raise prices and restrict production in much the same way as a monopoly. Where there is a formal agreement for such collusion, this is known as a cartel. A primary example of such a cartel is OPEC which has a profound influence on the international price of oil.

Firms often collude in an attempt to stabilize unstable markets, so as to reduce the risks inherent in these markets for investment and product development.[citation needed] There are legal restrictions on such collusion in most countries. There does not have to be a formal agreement for collusion to take place (although for the act to be illegal there must be actual communication between companies)–for example, in some industries there may be an acknowledged market leader which informally sets prices to which other producers respond, known as price leadership.

In other situations, competition between sellers in an oligopoly can be fierce, with relatively low prices and high production. This could lead to an efficient outcome approaching perfect competition. The competition in an oligopoly can be greater than when there are more firms in an industry if, for example, the firms were only regionally based and did not compete directly with each other.

Thus the welfare analysis of oligopolies is sensitive to the parameter values used to define the market's structure. In particular, the level of dead weight loss is hard to measure. The study of product differentiation indicates that oligopolies might also create excessive levels of differentiation in order to stifle competition.

Oligopoly theory makes heavy use of game theory to model the behavior of oligopolies:

- Stackelberg's duopoly. In this model the firms move sequentially (see Stackelberg competition).

- Cournot's duopoly. In this model the firms simultaneously choose quantities (see Cournot competition).

- Bertrand's oligopoly. In this model the firms simultaneously choose prices (see Bertrand competition).

Characteristics

Profit maximisation conditions: An oligopoly maximises profits by producing where marginal revenue equals marginal costs.[1]

Ability to set price: Oligopolies are price setters rather than price takers.[1]

Entry and exit: Barriers to entry are high.[2] The most important barriers are economies of scale, patents, access to expensive and complex technology, and strategic actions by incumbent firms designed to discourage or destroy nascent firms. Additional sources of barriers to entry often result from government regulation favoring existing firms making it difficult for new firms to enter the market.[3]

Number of firms: "Few" – a "handful" of sellers.[2] There are so few firms that the actions of one firm can influence the actions of the other firms.[4]

Long run profits: Oligopolies can retain long run abnormal profits. High barriers of entry prevent sideline firms from entering market to capture excess profits.

Product differentiation: Product may be homogeneous (steel) or differentiated (automobiles).[3]

Perfect knowledge: Assumptions about perfect knowledge vary but the knowledge of various economic actors can be generally described as selective. Oligopolies have perfect knowledge of their own cost and demand functions but their inter-firm information may be incomplete. Buyers have only imperfect knowledge as to price,[2] cost and product quality.

Interdependence: The distinctive feature of an oligopoly is interdependence.[5] Oligopolies are typically composed of a few large firms. Each firm is so large that its actions affect market conditions. Therefore the competing firms will be aware of a firm's market actions and will respond appropriately. This means that in contemplating a market action, a firm must take into consideration the possible reactions of all competing firms and the firm's countermoves.[6] It is very much like a game of chess or pool in which a player must anticipate a whole sequence of moves and countermoves in determining how to achieve his objectives. For example, an oligopoly considering a price reduction may wish to estimate the likelihood that competing firms would also lower their prices and possibly trigger a ruinous price war. Or if the firm is considering a price increase, it may want to know whether other firms will also increase prices or hold existing prices constant. This high degree of interdependence and need to be aware of what the other guy is doing or might do is to be contrasted with lack of interdependence in other market structures. In a PC market there is zero interdependence because no firm is large enough to affect market price. All firms in a PC market are price takers, information which they robotically follow in maximizing profits. In a monopoly there are no competitors to be concerned about. In a monopolistically competitive market each firm's effects on market conditions is so negligible as to be safely ignored by competitors.

Modeling

There is no single model describing the operation of an oligopolistic market.[6] The variety and complexity of the models is because you can have two to 102 firms competing on the basis of price, quantity, technological innovations, marketing, advertising and reputation. Fortunately, there are a series of simplified models that attempt to describe market behavior under certain circumstances. Some of the better-known models are the dominant firm model, the Cournot-Nash model, the Bertrand model and the kinked demand model

Dominant firm model

In some markets there is a single firm that controls a dominant share of the market and a group of smaller firms. The dominant firm sets prices which are simply taken by the smaller firms in determining their profit maximizing levels of production. This type of market is practically a monopoly and an attached perfectly competitive market in which price is set by the dominant firm rather than the market. The demand curve for the dominant firm is determined by subtracting the supply curves of all the small firms from the industry demand curve.[7] After estimating its net demand curve (market demand less the supply curve of the small firms) the dominant firm maximizes profits by following the normal p-max rule of producing where marginal revenue equals marginal costs. The small firms maximize profits by acting as PC firms–equating price to marginal costs.

Cournot-Nash model

Main article: Cournot competitionThe Cournot-Nash model is the simplest oligopoly model. The model assumes that there are two “equally positioned firms”; the firms compete on the basis of quantity rather than price and each firm makes an “output decision assuming that the other firm’s behavior is fixed.”[8] The market demand curve is assumed to be linear and marginal costs are constant. To find the Cournot-Nash equilibrium one determines how each firm reacts to a change in the output of the other firm. The path to equilibrium is a series of actions and reactions. The pattern continues until a point is reached where neither firm desires “to change what it is doing, given how it believes the other firm will react to any change.”[9] The equilibrium is the intersection of the two firm’s reaction functions. The reaction function shows how one firm reacts to the quantity choice of the other firm.[10] For example, assume that the firm 1’s demand function is P = (M - Q2) - Q1 where Q2 is the quantity produced by the other firm and Q1 is the amount produced by firm 1,[11] and M=60 is the market. Assume that marginal cost is CM=12. Firm 1 wants to know its maximizing quantity and price. Firm 1 begins the process by following the profit maximization rule of equating marginal revenue to marginal costs. Firm 1’s total revenue function is RT = Q1 P= Q1(M - Q2 - Q1) = M Q1- Q1 Q2 - Q12. The marginal revenue function is

.[12]

.[12]- RM = CM

- M - Q2 - 2Q1 = CM

- 2Q1 = (M-CM) - Q2

- Q1 = (M-CM)/2 - Q2/2 = 24 - 0,5 Q_2 [1.1]

- Q2 = 2(M-CM) - 2Q2 = 96 - 2 Q_1 [1.2]

Equation 1.1 is the reaction function for firm 1. Equation 1.2 is the reaction function for firm 2.

To determine the Cournot-Nash equilibrium you can solve the equations simultaneously. The equilibrium quantities can also be determined graphically. The equilibrium solution would be at the intersection of the two reaction functions. Note that if you graph the functions the axes represent quantities.[13] The reaction functions are not necessarily symmetric.[14] The firms may face differing cost functions in which case the reaction functions would not be identical nor would the equilibrium quantities.

Bertrand model

Main article: Bertrand competitionThe Bertrand model is essentially the Cournot-Nash model except the strategic variable is price rather than quantity.[15]

The model assumptions are:

- There are two firms in the market

- They produce a homogeneous product

- They produce at a constant marginal cost

- Firms choose prices PA and PB simultaneously

- Firms outputs are perfect substitutes

- Sales are split evenly if PA = PB[16]

The only Nash equilibrium is PA = PB = MC.

Neither firm has any reason to change strategy. If the firm raises prices it will lose all its customers. If the firm lowers price P < MC then it will be losing money on every unit sold.[17]

The Bertrand equilibrium is the same as the competitive result.[18] Each firm will produce where P = marginal costs and there will be zero profits.[15]

Kinked demand curve model

According to this model, each firm faces a demand curve kinked at the existing price.[19] The conjectural assumptions of the model are; if the firm raises its price above the current existing price, competitors will not follow and the acting firm will lose market share and second if a firm lowers prices below the existing price then their competitors will follow to retain their market share and the firm's output will increase only marginally.[20]

If the assumptions hold then:

- The firm's marginal revenue curve is discontinuous, and has a gap at the kink[19]

- For prices above the prevailing price the curve is relatively elastic [21]

- For prices below the point the curve is relatively inelastic [21]

The gap in the marginal revenue curve means that marginal costs can fluctuate without changing equilibrium price and quantity.[19] Thus prices tend to be rigid.

Examples

In industrialized economies, barriers to entry have resulted in oligopolies forming in many sectors, with unprecedented levels of competition fueled by increasing globalization. Market shares in an oligopoly are typically determined by product development and advertising. For example, there are now only a small number of manufacturers of civil passenger aircraft, though Brazil (Embraer) and Canada (Bombardier) have participated in the small passenger aircraft market sector. Oligopolies have also arisen in heavily-regulated markets such as wireless communications: in some areas only two or three providers are licensed to operate.

Australia

- Most media outlets are owned either by News Corporation, Time Warner, or by Fairfax Media[22]

- Grocery retailing is dominated by Coles Group and Woolworths.[citation needed]

- Banking is dominated by ANZ, Westpac, NAB, and Commonwealth Bank. To an extent this oligopoly is enshrined in law in what is known as the "Four pillars policy", in order to ensure the stability of Australia's banking system.

Canada

- Six companies (Royal Bank of Canada, Toronto Dominion Bank, Bank of Nova Scotia, Bank of Montreal, Canadian Imperial Bank of Commerce and National Bank of Canada) control the banking industry.

- As of 2008[update], three companies (Rogers Wireless, Bell Mobility and Telus Mobility) share over 94% of Canada's wireless market.[23][24]

- 2 companies control the internet service provider market, (Rogers), (Bell)

United Kingdom

- Five banks dominate the UK banking sector, they were accused of being an oligopoly by the relative newcomer Virgin bank.[25]

- Four companies (Tesco, Sainsbury's, Asda and Morrisons) share 74.4% of the grocery market.[26]

- The detergent market is dominated by two players, Unilever and Procter & Gamble.[27]

United States

- Many media industries today are essentially oligopolies.

- Six movie studios receive 90% of American film revenues.[citation needed]

- The television industry is mostly an oligopoly of seven companies: The Walt Disney Company, CBS Corporation, Viacom, Comcast, Hearst Corporation, Time Warner, and News Corporation.[28] See Concentration of media ownership.

- Four wireless providers (AT&T, Verizon Wireless, T-Mobile, Sprint Nextel) control 89% of the cellular telephone service market.[29] This is not to be confused with cellular telephone manufacturing, an integral portion of the cellular telephone market as a whole.

- Healthcare insurance in the United States consists of very few insurance companies controlling major market share in most states. For example, California's insured population of 20 million is the most competitive in the nation and 44% of that market is dominated by two insurance companies, Anthem and Kaiser Permanente.[30]

- Anheuser-Busch and MillerCoors control about 80% of the beer industry.[31]

Worldwide

- The accountancy market is controlled by PriceWaterhouseCoopers, KPMG, Deloitte Touche Tohmatsu, and Ernst & Young (commonly known as the Big Four)[32]

- Three leading food processing companies, Kraft Foods, PepsiCo and Nestle, together achieve a large proportion[vague] of global processed food sales. These three companies are often used as an example of "Rule of three",[33] which states that markets often become an oligopoly of three large firms.

- Boeing and Airbus have a duopoly over the airliner market.[34]

- General Electric, Pratt and Whitney and Rolls-Royce plc own more than 50% of the marketshare in the airliner engine market.[citation needed]

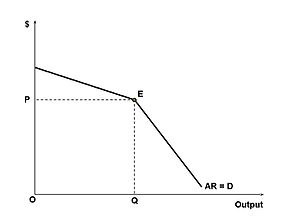

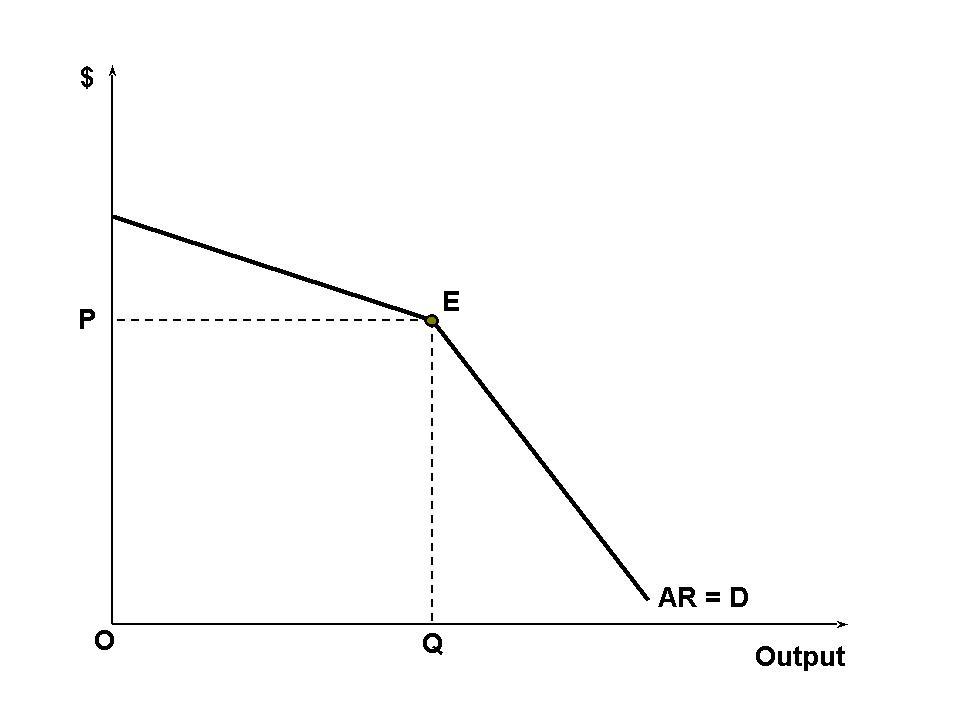

Demand curve

Above the kink, demand is relatively elastic because all other firms' prices remain unchanged. Below the kink, demand is relatively inelastic because all other firms will introduce a similar price cut, eventually leading to a price war. Therefore, the best option for the oligopolist is to produce at point E which is the equilibrium point and the kink point. This is a theoretical model proposed in 1947, which has failed to receive conclusive evidence for support.

Above the kink, demand is relatively elastic because all other firms' prices remain unchanged. Below the kink, demand is relatively inelastic because all other firms will introduce a similar price cut, eventually leading to a price war. Therefore, the best option for the oligopolist is to produce at point E which is the equilibrium point and the kink point. This is a theoretical model proposed in 1947, which has failed to receive conclusive evidence for support.

In an oligopoly, firms operate under imperfect competition. With the fierce price competitiveness created by this sticky-upward demand curve, firms use non-price competition in order to accrue greater revenue and market share.

"Kinked" demand curves are similar to traditional demand curves, as they are downward-sloping. They are distinguished by a hypothesized convex bend with a discontinuity at the bend–"kink". Thus the first derivative at that point is undefined and leads to a jump discontinuity in the marginal revenue curve.

Classical economic theory assumes that a profit-maximizing producer with some market power (either due to oligopoly or monopolistic competition) will set marginal costs equal to marginal revenue. This idea can be envisioned graphically by the intersection of an upward-sloping marginal cost curve and a downward-sloping marginal revenue curve (because the more one sells, the lower the price must be, so the less a producer earns per unit). In classical theory, any change in the marginal cost structure (how much it costs to make each additional unit) or the marginal revenue structure (how much people will pay for each additional unit) will be immediately reflected in a new price and/or quantity sold of the item. This result does not occur if a "kink" exists. Because of this jump discontinuity in the marginal revenue curve, marginal costs could change without necessarily changing the price or quantity.

The motivation behind this kink is the idea that in an oligopolistic or monopolistically competitive market, firms will not raise their prices because even a small price increase will lose many customers. This is because competitors will generally ignore price increases, with the hope of gaining a larger market share as a result of now having comparatively lower prices. However, even a large price decrease will gain only a few customers because such an action will begin a price war with other firms. The curve is therefore more price-elastic for price increases and less so for price decreases. Firms will often enter the industry in the long run.

See also

- Big Business

- Monopsony

- Oligopolistic reaction

- Oligopsony

- Perfect competition

- Prisoner's Dilemma

- Simulations and games in economics education

- Swing producer

Notes

- ^ a b Perloff, J. Microeconomics Theory & Applications with Calculus. page 445. Pearson 2008.

- ^ a b c Hirschey, M. Managerial Economics. Rev. Ed, page 451. Dryden 2000.

- ^ a b Negbennebor, A: Microeconomics, The Freedom to Choose CAT 2001[page needed]

- ^ Negbennebor, A: Microeconomics, The Freedom to Choose page 291. CAT 2001

- ^ Melvin & Boyes, Microeconomics 5th ed. page 267. Houghton Mifflin 2002

- ^ a b Colander, David C. Microeconomics 7th ed. Page 288 McGraw-Hill 2008.

- ^ Samuelson, W & Marks, S: 100. Managerial Economics page 403. 4th ed. Wiley 2003.

- ^ This statement is the Cournot conjectures. Kreps, D.: A Course in Microeconomic Theory page 326. Princeton 1990.

- ^ Kreps, D. A Course in Microeconomic Theory. page 326. Princeton 1990.

- ^ Kreps, D. A Course in Microeconomic Theory. Princeton 1990.[page needed]

- ^ Samuelson, W & Marks, S. Managerial Economics. 4th ed. Wiley 2003[page needed]

- ^ RM = M - Q2 - 2Q1. can be restated as RM = (M − Q2) − 2Q1 RM = (M - Q2) - 2Q1.

- ^ Pindyck, R & Rubinfeld, D: Microeconomics 5th ed. Prentice-Hall 2001[page needed]

- ^ Pindyck, R & Rubinfeld, D: Microeconomics 5th ed. Prentice-Hall 2001

- ^ a b Samuelson, W. & Marks, S. Managerial Economics. 4th ed. page 415 Wiley 2003.

- ^ There is nothing to guarantee an even split. Kreps, D.: A Course in Microeconomic Theory page 331. Princeton 1990.

- ^ This assumes that there are no capacity restriction. Binger, B & Hoffman, E, 284-85. Microeconomics with Calculus, 2nd ed. Addison-Wesley, 1998.

- ^ Pindyck, R & Rubinfeld, D: Microeconomics 5th ed.page 438 Prentice-Hall 2001.

- ^ a b c Pindyck, R. & Rubinfeld, D. Microeconomics 5th ed. page 446. Prentice-Hall 2001.

- ^ Simply stated the rule is that competitors will ignore price increases and follow price decreases. Negbennebor, A: Microeconomics, The Freedom to Choose page 299. CAT 2001

- ^ a b Negbennebor, A. Microeconomics: The Freedom to Choose. page 299. CAT 2001

- ^ Media Industry Profile: Australia, Datamonitor, October 2008[page needed]

- ^ http://cwta.ca/CWTASite/english/facts_figures_downloads/SubscribersStats_en_2008_Q4.pdf

- ^ http://www.crtc.gc.ca/eng/publications/reports/policymonitoring/2008/cmr2008.pdf

- ^ Big banks running an oligopoly, says Virgin Money chief, January 2011\url=http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/8266582/Big-banks-running-an-oligopoly-says-Virgin-Money-chief.html

- ^ Probe says 'too few supermarkets', BBC News, 31 October 2007, http://news.bbc.co.uk/1/hi/business/4785544.stm, retrieved 2009-04-03

- ^ Textile Washing Products Industry Profile: United Kingdom, Datamonitor, November 2008[page needed]

- ^ Rodman, George. Mass Media in a Changing World. New York (2nd ed.), McGraw Hill, 2008[page needed]

- ^ http://www.slideshare.net/chetansharma/us-wireless-market-q4-2008-and-2008-update-mar-2009-chetan-sharma-consulting

- ^ http://www.cnbc.com/id/32918263

- ^ Beer Industry Profile: United States, Datamonitor, Dec. 2008[page needed]

- ^ Accountancy Industry Profile: Global, Datamonitor, September 2008[page needed]

- ^ The Rule of Three, New York: Boston Publishing.[page needed]

- ^ Airlines Industry Profile: United States, Datamonitor, November 2008, pp. 13–14

External links

- Microeconomics by Elmer G. Wiens: Online Interactive Models of Oligopoly, Differentiated Oligopoly, and Monopolistic Competition

- Vives, X. (1999). Oligopoly pricing, MIT Press, Cambridge MA. (A comprehensive work on oligopoly theory)

- Oligopoly Watch A blog on current oligopoly issues from a business and social perspective

- Simulations in Managerial/Business Economics

- Simulations in Principles of Economics

Microeconomics Major topics Aggregation · Budget · Consumer · Convexity and non-convexity · Cost · Cost-benefit analysis · Distribution · Deadweight loss · Income–consumption curve · Duopoly · Equilibria · Economies of scale · Economies of scope · Elasticity · Exchange · Expected utility · Externality · Firms · General equilibria · Household · Information · Indifference curve · Intertemporal choice · Marginal cost · Market failure · Market structure · Monopoly · Monopsony · Oligopoly · Opportunity cost · Preferences · Prices · Production · Profit · Public goods · Returns to scale · Risk · Scarcity · Shortage · Social choice · Sunk costs · Supply & demand · Surplus · Uncertainty · Utility · WelfareRelated Behavioral · Business · Computational · Decision theory · Econometrics · Experimental · Game theory · Industrial organization · Mathematical economics · Microfoundations of Macroeconomics · Managerial · Operations research · OptimizationCategories:- Market structure and pricing

- Economic problems

- Oligopoly

Wikimedia Foundation. 2010.