- Efficient-market hypothesis

-

Financial markets

Exchange

SecuritiesBond market Fixed income

Corporate bond

Government bond

Municipal bond

Bond valuation

High-yield debtStock market Stock

Preferred stock

Common stock

Registered share

Voting share

Stock exchangeDerivatives market Securitization

Hybrid security

Credit derivative

Futures exchangeOTC, non organized Foreign exchange Other markets Money market

Reinsurance market

Commodity market

Real estate marketPractical trading

Finance series

Banks and banking

Corporate finance

Personal finance

Public financeIn finance, the efficient-market hypothesis (EMH) asserts that financial markets are "informationally efficient". That is, one cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis, given the information available at the time the investment is made.

There are three major versions of the hypothesis: "weak", "semi-strong", and "strong". The weak-form EMH claims that prices on traded assets (e.g., stocks, bonds, or property) already reflect all past publicly available information. The semi-strong-form EMH claims both that prices reflect all publicly available information and that prices instantly change to reflect new public information. The strong-form EMH additionally claims that prices instantly reflect even hidden or "insider" information. Critics have blamed the belief in rational markets for much of the late-2000s financial crisis.[1][2][3] In response, proponents of the hypothesis have stated that market efficiency does not mean having no uncertainty about the future, that market efficiency is a simplification of the world which may not always hold true, and that the market is practically efficient for investment purposes for most individuals.[4]

Contents

Historical background

Historically, there was a very close link between EMH and the random-walk model and then the Martingale model. The random character of stock market prices was first modelled by Jules Regnault, a French broker, in 1863 and then by Louis Bachelier, a French mathematician, in his 1900 PhD thesis, "The Theory of Speculation".[5] His work was largely ignored until the 1950s; however beginning in the 30s scattered, independent work corroborated his thesis. A small number of studies indicated that US stock prices and related financial series followed a random walk model.[6] Research by Alfred Cowles in the ’30s and ’40s suggested that professional investors were in general unable to outperform the market.

The efficient-market hypothesis was developed by Professor Eugene Fama at the University of Chicago Booth School of Business as an academic concept of study through his published Ph.D. thesis in the early 1960s at the same school. It was widely accepted up until the 1990s, when behavioral finance economists, who had been a fringe element, became mainstream.[7] Empirical analyses have consistently found problems with the efficient-market hypothesis, the most consistent being that stocks with low price to earnings (and similarly, low price to cash-flow or book value) outperform other stocks.[8][9] Alternative theories have proposed that cognitive biases cause these inefficiencies, leading investors to purchase overpriced growth stocks rather than value stocks.[7] Although the efficient-market hypothesis has become controversial because substantial and lasting inefficiencies are observed, Beechey et al. (2000) consider that it remains a worthwhile starting point.[10]

The efficient-market hypothesis emerged as a prominent theory in the mid-1960s. Paul Samuelson had begun to circulate Bachelier's work among economists. In 1964 Bachelier's dissertation along with the empirical studies mentioned above were published in an anthology edited by Paul Cootner.[11] In 1965 Eugene Fama published his dissertation arguing for the random walk hypothesis,[12] and Samuelson published a proof for a version of the efficient-market hypothesis.[13] In 1970 Fama published a review of both the theory and the evidence for the hypothesis. The paper extended and refined the theory, included the definitions for three forms of financial market efficiency: weak, semi-strong and strong (see below).[14]

It has been argued that the stock market is “micro efficient” but “macro inefficient”. The main proponent of this view was Samuelson, who asserted that the EMH is much better suited for individual stocks than it is for the aggregate stock market. Research based on regression and scatter diagrams has strongly supported Samuelson's dictum.[15]

Further to this evidence that the UK stock market is weak-form efficient, other studies of capital markets have pointed toward their being semi-strong-form efficient. A study by Khan of the grain futures market indicated semi-strong form efficiency following the release of large trader position information (Khan, 1986). Studies by Firth (1976, 1979, and 1980) in the United Kingdom have compared the share prices existing after a takeover announcement with the bid offer. Firth found that the share prices were fully and instantaneously adjusted to their correct levels, thus concluding that the UK stock market was semi-strong-form efficient. However, the market's ability to efficiently respond to a short term, widely publicized event such as a takeover announcement does not necessarily prove market efficiency related to other more long term, amorphous factors. David Dreman has criticized the evidence provided by this instant "efficient" response, pointing out that an immediate response is not necessarily efficient, and that the long-term performance of the stock in response to certain movements are better indications. A study on stocks' response to dividend cuts or increases over three years found that after an announcement of a dividend cut, stocks underperformed the market by 15.3% for the three-year period, while stocks outperformed the market by 24.8% for the three years following the announcement of a dividend increase.[16]

Theoretical background

Beyond the normal utility maximizing agents, the efficient-market hypothesis requires that agents have rational expectations; that on average the population is correct (even if no one person is) and whenever new relevant information appears, the agents update their expectations appropriately. Note that it is not required that the agents be rational. EMH allows that when faced with new information, some investors may overreact and some may underreact. All that is required by the EMH is that investors' reactions be random and follow a normal distribution pattern so that the net effect on market prices cannot be reliably exploited to make an abnormal profit, especially when considering transaction costs (including commissions and spreads). Thus, any one person can be wrong about the market—indeed, everyone can be—but the market as a whole is always right. There are three common forms in which the efficient-market hypothesis is commonly stated—weak-form efficiency, semi-strong-form efficiency and strong-form efficiency, each of which has different implications for how markets work.

In weak-form efficiency, future prices cannot be predicted by analyzing prices from the past. Excess returns cannot be earned in the long run by using investment strategies based on historical share prices or other historical data. Technical analysis techniques will not be able to consistently produce excess returns, though some forms of fundamental analysis may still provide excess returns. Share prices exhibit no serial dependencies, meaning that there are no "patterns" to asset prices. This implies that future price movements are determined entirely by information not contained in the price series. Hence, prices must follow a random walk. This 'soft' EMH does not require that prices remain at or near equilibrium, but only that market participants not be able to systematically profit from market 'inefficiencies'. However, while EMH predicts that all price movement (in the absence of change in fundamental information) is random (i.e., non-trending), many studies have shown a marked tendency for the stock markets to trend over time periods of weeks or longer[17] and that, moreover, there is a positive correlation between degree of trending and length of time period studied[18] (but note that over long time periods, the trending is sinusoidal in appearance). Various explanations for such large and apparently non-random price movements have been promulgated.

The problem of algorithmically constructing prices which reflect all available information has been studied extensively in the field of computer science.[19][20] For example, the complexity of finding the arbitrage opportunities in pair betting markets has been shown to be NP-hard.[21]

In semi-strong-form efficiency, it is implied that share prices adjust to publicly available new information very rapidly and in an unbiased fashion, such that no excess returns can be earned by trading on that information. Semi-strong-form efficiency implies that neither fundamental analysis nor technical analysis techniques will be able to reliably produce excess returns. To test for semi-strong-form efficiency, the adjustments to previously unknown news must be of a reasonable size and must be instantaneous. To test for this, consistent upward or downward adjustments after the initial change must be looked for. If there are any such adjustments it would suggest that investors had interpreted the information in a biased fashion and hence in an inefficient manner.

In strong-form efficiency, share prices reflect all information, public and private, and no one can earn excess returns. If there are legal barriers to private information becoming public, as with insider trading laws, strong-form efficiency is impossible, except in the case where the laws are universally ignored. To test for strong-form efficiency, a market needs to exist where investors cannot consistently earn excess returns over a long period of time. Even if some money managers are consistently observed to beat the market, no refutation even of strong-form efficiency follows: with hundreds of thousands of fund managers worldwide, even a normal distribution of returns (as efficiency predicts) should be expected to produce a few dozen "star" performers.

Criticism and behavioral finance

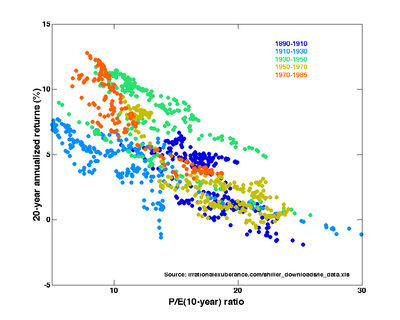

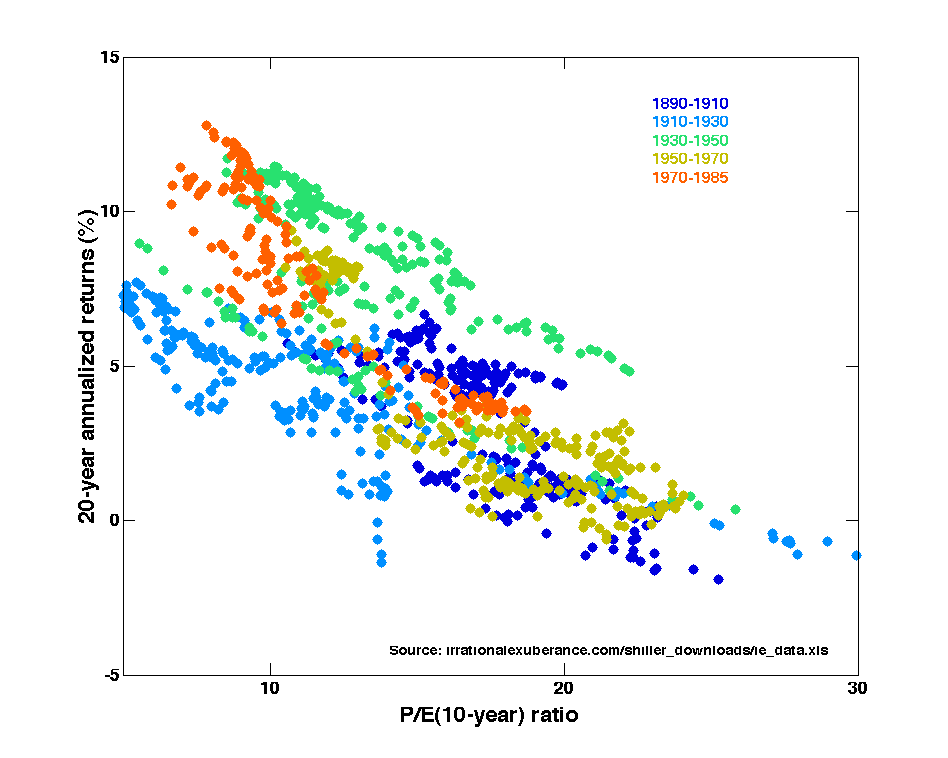

Price-Earnings ratios as a predictor of twenty-year returns based upon the plot by Robert Shiller (Figure 10.1,[22] source). The horizontal axis shows the real price-earnings ratio of the S&P Composite Stock Price Index as computed in Irrational Exuberance (inflation adjusted price divided by the prior ten-year mean of inflation-adjusted earnings). The vertical axis shows the geometric average real annual return on investing in the S&P Composite Stock Price Index, reinvesting dividends, and selling twenty years later. Data from different twenty-year periods is color-coded as shown in the key. See also ten-year returns. Shiller states that this plot "confirms that long-term investors—investors who commit their money to an investment for ten full years—did do well when prices were low relative to earnings at the beginning of the ten years. Long-term investors would be well advised, individually, to lower their exposure to the stock market when it is high, as it has been recently, and get into the market when it is low."[22] Burton Malkiel stated that this correlation may be consistent with an efficient market due to differences in interest rates.[23]

Price-Earnings ratios as a predictor of twenty-year returns based upon the plot by Robert Shiller (Figure 10.1,[22] source). The horizontal axis shows the real price-earnings ratio of the S&P Composite Stock Price Index as computed in Irrational Exuberance (inflation adjusted price divided by the prior ten-year mean of inflation-adjusted earnings). The vertical axis shows the geometric average real annual return on investing in the S&P Composite Stock Price Index, reinvesting dividends, and selling twenty years later. Data from different twenty-year periods is color-coded as shown in the key. See also ten-year returns. Shiller states that this plot "confirms that long-term investors—investors who commit their money to an investment for ten full years—did do well when prices were low relative to earnings at the beginning of the ten years. Long-term investors would be well advised, individually, to lower their exposure to the stock market when it is high, as it has been recently, and get into the market when it is low."[22] Burton Malkiel stated that this correlation may be consistent with an efficient market due to differences in interest rates.[23]

Investors and researchers have disputed the efficient-market hypothesis both empirically and theoretically. Behavioral economists attribute the imperfections in financial markets to a combination of cognitive biases such as overconfidence, overreaction, representative bias, information bias, and various other predictable human errors in reasoning and information processing. These have been researched by psychologists such as Daniel Kahneman, Amos Tversky, Richard Thaler, and Paul Slovic. These errors in reasoning lead most investors to avoid value stocks and buy growth stocks at expensive prices, which allow those who reason correctly to profit from bargains in neglected value stocks and the overreacted selling of growth stocks.

Empirical evidence has been mixed, but has generally not supported strong forms of the efficient-market hypothesis[8][9][24] According to Dreman and Berry, in a 1995 paper, low P/E stocks have greater returns.[25] In an earlier paper Dreman also refuted the assertion by Ray Ball that these higher returns could be attributed to higher beta,[26] whose research had been accepted by efficient market theorists as explaining the anomaly[27] in neat accordance with modern portfolio theory.

One can identify "losers" as stocks that have had poor returns over some number of past years. "Winners" would be those stocks that had high returns over a similar period. The main result of one such study is that losers have much higher average returns than winners over the following period of the same number of years.[28] A later study showed that beta (β) cannot account for this difference in average returns.[29] This tendency of returns to reverse over long horizons (i.e., losers become winners) is yet another contradiction of EMH. Losers would have to have much higher betas than winners in order to justify the return difference. The study showed that the beta difference required to save the EMH is just not there.

Speculative economic bubbles are an obvious anomaly, in that the market often appears to be driven by buyers operating on irrational exuberance, who take little notice of underlying value. These bubbles are typically followed by an overreaction of frantic selling, allowing shrewd investors to buy stocks at bargain prices. Rational investors have difficulty profiting by shorting irrational bubbles because, as John Maynard Keynes commented, "Markets can remain irrational far longer than you or I can remain solvent."[citation needed] Sudden market crashes as happened on Black Monday in 1987 are mysterious from the perspective of efficient markets, but allowed as a rare statistical event under the Weak-form of EMH.

Burton Malkiel, a well-known proponent of the general validity of EMH, has warned that certain emerging markets such as China are not empirically efficient; that the Shanghai and Shenzhen markets, unlike markets in United States, exhibit considerable serial correlation (price trends), non-random walk, and evidence of manipulation.[30]

Behavioral psychology approaches to stock market trading are among some of the more promising alternatives to EMH (and some investment strategies seek to exploit exactly such inefficiencies). But Nobel Laureate co-founder of the programme—Daniel Kahneman—announced his skepticism of investors beating the market: "They're [investors] just not going to do it [beat the market]. It's just not going to happen."[31] Indeed defenders of EMH maintain that Behavioral Finance strengthens the case for EMH in that BF highlights biases in individuals and committees and not competitive markets. For example, one prominent finding in Behaviorial Finance is that individuals employ hyperbolic discounting. It is palpably true that bonds, mortgages, annuities and other similar financial instruments subject to competitive market forces do not. Any manifestation of hyperbolic discounting in the pricing of these obligations would invite arbitrage thereby quickly eliminating any vestige of individual biases. Similarly, diversification, derivative securities and other hedging strategies assuage if not eliminate potential mispricings from the severe risk-intolerance (loss aversion) of individuals underscored by behavioral finance. On the other hand, economists, behaviorial psychologists and mutual fund managers are drawn from the human population and are therefore subject to the biases that behavioralists showcase. By contrast, the price signals in markets are far less subject to individual biases highlighted by the Behavioral Finance programme. Richard Thaler has started a fund based on his research on cognitive biases. In a 2008 report he identified complexity and herd behavior as central to the global financial crisis of 2008.[32]

Further empirical work has highlighted the impact transaction costs have on the concept of market efficiency, with much evidence suggesting that any anomalies pertaining to market inefficiencies are the result of a cost benefit analysis made by those willing to incur the cost of acquiring the valuable information in order to trade on it. Additionally the concept of liquidity is a critical component to capturing "inefficiencies" in tests for abnormal returns. Any test of this proposition faces the joint hypothesis problem, where it is impossible to ever test for market efficiency, since to do so requires the use of a measuring stick against which abnormal returns are compared - one cannot know if the market is efficient if one does not know if a model correctly stipulates the required rate of return. Consequently, a situation arises where either the asset pricing model is incorrect or the market is inefficient, but one has no way of knowing which is the case.[citation needed]

A key work on random walk was done in the late 1980s by Profs. Andrew Lo and Craig MacKinlay; they effectively argue that a random walk does not exist, nor ever has.[33] Their paper took almost two years to be accepted by academia and in 1999 they published "A Non-random Walk Down Wall St." which collects their research papers on the topic up to that time.

Economists Matthew Bishop and Michael Green claim that full acceptance of the hypothesis goes against the thinking of Adam Smith and John Maynard Keynes, who both believed irrational behavior had a real impact on the markets.[34]

Warren Buffett has also argued against EMH, saying the preponderance of value investors among the world's best money managers rebuts the claim of EMH proponents that luck is the reason some investors appear more successful than others.[35]

Late 2000s financial crisis

The financial crisis of 2007–2010 has led to renewed scrutiny and criticism of the hypothesis.[36] Market strategist Jeremy Grantham has stated flatly that the EMH is responsible for the current financial crisis, claiming that belief in the hypothesis caused financial leaders to have a "chronic underestimation of the dangers of asset bubbles breaking".[2] Noted financial journalist Roger Lowenstein blasted the theory, declaring "The upside of the current Great Recession is that it could drive a stake through the heart of the academic nostrum known as the efficient-market hypothesis."[3]

At the International Organization of Securities Commissions annual conference, held in June 2009, the hypothesis took center stage. Martin Wolf, the chief economics commentator for the Financial Times, dismissed the hypothesis as being a useless way to examine how markets function in reality. Paul McCulley, managing director of PIMCO, was less extreme in his criticism, saying that the hypothesis had not failed, but was "seriously flawed" in its neglect of human nature.[37]

The financial crisis has led Richard Posner, a prominent judge, University of Chicago law professor, and innovator in the field of Law and Economics, to back away from the hypothesis and express some degree of belief in Keynesian economics. Posner accused some of his Chicago School colleagues of being "asleep at the switch", saying that "the movement to deregulate the financial industry went too far by exaggerating the resilience - the self healing powers - of laissez-faire capitalism."[38] Others, such as Fama himself, said that the hypothesis held up well during the crisis and that the markets were a casualty of the recession, not the cause of it. Despite this, Fama has conceded that "poorly informed investors could theoretically lead the market astray" and that stock prices could become "somewhat irrational" as a result.[39]

Critics have suggested that financial institutions and corporations have been able to reduce the efficiency of financial markets by creating private information and reducing the accuracy of conventional disclosures, and by developing new and complex products which are challenging for most market participants to evaluate and correctly price.[40][41]

See also

Notes

- ^ Fox, Justin (2009). Myth of the Rational Market. Harper Business. ISBN 0-06-059899-9.

- ^ a b Nocera, Joe (5 June 2009). "Poking Holes in a Theory on Markets". New York Times. http://www.nytimes.com/2009/06/06/business/06nocera.html?scp=1&sq=efficient%20market&st=cse. Retrieved 8 June 2009.

- ^ a b Lowenstein, Roger (7 June 2009). "Book Review: 'The Myth of the Rational Market' by Justin Fox". Washington Post. http://www.washingtonpost.com/wp-dyn/content/article/2009/06/05/AR2009060502053.html. Retrieved 5 August 2011.

- ^ Desai, Sameer (27 March 2011). "Efficient Market Hypothesis". http://www.indexingblog.com/2011/03/27/efficient-market-hypothesis/. Retrieved 2 June 2011.

- ^ Kirman, Alan. "Economic theory and the crisis." Voxeu. 14 November 2009. http://www.voxeu.org/index.php?q=node/4208

- ^ See Working (1934), Cowles and Jones (1937), and Kendall (1953), and later Brealey, Dryden and Cunningham.

- ^ a b Fox J. (2002). Is The Market Rational? No, say the experts. But neither are you--so don't go thinking you can outsmart it. Fortune.

- ^ a b Empirical papers questioning EMH:

- Francis Nicholson. Price-Earnings Ratios in Relation to Investment Results. Financial Analysts Journal. Jan/Feb 1968:105-109.

- Sanjoy Basu. (1977). Investment Performance of Common Stocks in Relation to Their Price-Earnings Ratios: A test of the Efficient Markets Hypothesis. Journal of Finance 32:663-682.

- Rosenberg B, Reid K, Lanstein R. (1985). Persuasive Evidence of Market Inefficiency. Journal of Portfolio Management 13:9-17.

- ^ a b Fama E, French K. (1992). The Cross-Section of Expected Stock Returns. Journal of Finance 47:427-465

- ^ Beechey M, Gruen D, Vickrey J. (2000). The Efficient Markets Hypothesis: A Survey. Reserve Bank of Australia.

- ^ Cootner (ed.), Paul (1964). The Random Character of StockMarket Prices. MIT Press.

- ^ Fama, Eugene (1965). "The Behavior of Stock Market Prices". Journal of Business 38: 34–105. doi:10.1086/294743.

- ^ Samuelson, Paul (1965). "Proof That Properly Anticipated Prices Fluctuate Randomly". Industrial Management Review 6: 41–49.

- ^ Fama, Eugene (1970). "Efficient Capital Markets: A Review of Theory and Empirical Work". Journal of Finance 25 (2): 383–417. doi:10.2307/2325486. JSTOR 2325486.

- ^ Jung, Jeeman; Shiller, Robert (2005). "Samuelson's Dictum And The Stock Market". Economic Inquiry 43 (2): 221–228. doi:10.1093/ei/cbi015.

- ^ Michaely R, Thaler RH, Womack K. (1993). Price Reactions to Dividend Initiatives and Omissions: Overreaction or Drift? Cornell University, Working Paper.

- ^ Saad, Emad W., Student Member, IEEE; Prokhorov, Danil V. Member , IEEE; and Wunsch,II, Donald C. Senior Member, IEEE (November, 1998). "Comparative Study of Stock Trend Prediction Using Time Delay, Recurrent and Probabilistic Neural Networks". IEEE Transactions on Neural Networks 9 (6): 1456–1470. doi:10.1109/72.728395. PMID 18255823.

- ^ Granger, Clive W. J. & Morgenstern, Oskar (5 May 2007). "Spectral Analysis Of New York Stock Market Prices". Kyklos 16 (1): 1–27. doi:10.1111/j.1467-6435.1963.tb00270.x.

- ^ Kleinberg, Jon; Tardos, Eva (2005). Algorithm Design. Addison Wesley. ISBN 0321295358.

- ^ Nisan, Roughgarden, Tardos, Vazirani (2007). Algorithmic Game Theory. Cambridge University Press. ISBN 0521872820.

- ^ Chen, Y; Fortnow, L; Nikolova, E; Pennock, D (2007). "Betting on permutations". Proceedings of the 8th ACM conference on Electronic commerce 8: 326–335. ISBN 978-1-59593-653-0.

- ^ a b Shiller, Robert (2005). Irrational Exuberance (2d ed.). Princeton University Press. ISBN 0-691-12335-7.

- ^ Burton G. Malkiel (2006). A Random Walk Down Wall Street. ISBN 0-393-32535-0. p.254.

- ^ Chan, Kam C.; Gup, Benton E. & Pan, Ming-Shiun (4 Mar 2003). "International Stock Market Efficiency and Integration: A Study of Eighteen Nations". Journal of Business Finance & Accounting 24 (6): 803–813. doi:10.1111/1468-5957.00134.

- ^ Dreman David N. & Berry Michael A. (1995). "Overreaction, Underreaction, and the Low-P/E Effect". Financial Analysts Journal 51 (4): 21–30. doi:10.2469/faj.v51.n4.1917.

- ^ Ball R. (1978). Anomalies in Relationships between Securities' Yields and Yield-Surrogates. Journal of Financial Economics 6:103-126

- ^ Dreman D. (1998). Contrarian Investment Strategy: The Next Generation. Simon and Schuster.

- ^ DeBondt, Werner F.M. & Thaler, Richard H. (1985). "Does the Stock Market Overreact". Journal of Finance 40: 557–558.

- ^ Chopra, Navin; Lakonishok, Josef; & Ritter, Jay R. (1985). "Measuring Abnormal Performance: Do Stocks Overreact". Journal of Financial Economics 31 (2): 235–268. doi:10.1016/0304-405X(92)90005-I.

- ^ Burton Malkiel. Investment Opportunities in China. July 16, 2007. (34:15 mark)

- ^ Hebner, Mark (12 August 2005). "Step 2: Nobel Laureates". Index Funds: The 12-Step Program for Active Investors. Index Funds Advisors, Inc.. http://www.ifa.com/Book/Book_pdf/02_Nobel_Laureates.pdf. Retrieved 12 August 2005.

- ^ Thaler RH. (2008). 3Q2008. Fuller & Thaler Asset Management.

- ^ "A Non-Random Walk Down Wall Street". Princeton University Press. http://press.princeton.edu/titles/6558.html.

- ^ Hurt III, Harry (19 March 2010). "The Case for Financial Reinvention". The New York Times. http://www.nytimes.com/2010/03/21/business/21shelf.html. Retrieved 29 March 2010.

- ^ Hoffman, Greg (14 July 2010). "Paul the octopus proves Buffett was right". Sydney Morning Herald. http://www.smh.com.au/business/paul-the-octopus-proves-buffett-was-right-20100714-10air.html?autostart=1. Retrieved 4 August 2010.

- ^ "Sun finally sets on notion that markets are rational". The Globe and Mail. 7 July 2009. http://www.theglobeandmail.com/globe-investor/investment-ideas/features/taking-stock/sun-finally-sets-on-notion-that-markets-are-rational/article1206213/. Retrieved 7 July 2009.

- ^ "Has 'guiding model' for global markets gone haywire?". Jerusalem Post. 11 June 2009. http://fr.jpost.com/servlet/Satellite?cid=1244371066953&pagename=JPost/JPArticle/ShowFull. Retrieved 17 June 2009.

- ^ "After the Blowup". The New Yorker. 11 January 2010. http://www.newyorker.com/reporting/2010/01/11/100111fa_fact_cassidy. Retrieved 12 January 2010.

- ^ Jon E. Hilsenrath, Stock Characters: As Two Economists Debate Markets, The Tide Shifts. Wall Street Journal 2004

- ^ Michael Simkovic, "Secret Liens and the Financial Crisis of 2008", American Bankruptcy Law Journal 2009

- ^ Michael Simkovic, "Competition and Crisis in Mortgage Securitization"

References

- Burton G. Malkiel (1987). "efficient market hypothesis," The New Palgrave: A Dictionary of Economics, v. 2, pp. 120–23.

- The Arithmetic of Active Management, by William F. Sharpe

- Burton G. Malkiel, A Random Walk Down Wall Street, W. W. Norton, 1996, ISBN 0-393-03888-2

- John Bogle, Bogle on Mutual Funds: New Perspectives for the Intelligent Investor, Dell, 1994, ISBN 0-440-50682-4

- Mark T. Hebner, Index Funds: The 12-Step Program for Active Investors, IFA Publishing, 2007, ISBN 0-9768023-0-9

- Cowles, Alfred; H. Jones (1937). "Some A Posteriori Probabilities in Stock Market Action". Econometrica 5 (3): 280–294. doi:10.2307/1905515. JSTOR 1905515.

- Kendall, Maurice. "The Analysis of Economic Time Series". Journal of the Royal Statistical Society 96: 11–25.

- Khan, Arshad M (1986) (1986). "Conformity with Large Speculators: A Test of Efficiency in the Grain Futures Market". Atlantic Economic Journal 14 (3): 51–55. doi:10.1007/BF02304624.

- Paul Samuelson, "Proof That Properly Anticipated Prices Fluctuate Randomly." Industrial Management Review, Vol. 6, No. 2, pp. 41–49. Reproduced as Chapter 198 in Samuelson, Collected Scientific Papers, Volume III, Cambridge, M.I.T. Press, 1972.

- Working, Holbrook (1960). "Note on the Correlation of First Differences of Averages in a Random Chain". Econometrica 28 (4): 916–918. doi:10.2307/1907574. JSTOR 1907574.

- Lo, Andrew and MacKinlay, Craig, "A Non-random Walk Down Wall St." Princeton Paperbacks, 2001

External links

- e-m-h.org

- "Earnings Quality and the Equity Risk Premium: A Benchmark Model" abstract from Contemporary Accounting Research

- "As The Index Fund Moves from Heresy to Dogma . . . What More Do We Need To Know?" Remarks by John Bogle on the superior returns of passively managed index funds.

- Proof That Properly Discounted Present Values of Assets Vibrate Randomly Paul Samuelson

- Human Behavior and the Efficiency of the Financial System (1999) by Robert J. Shiller Handbook of Macroeconomics

Investment management Collective investment scheme structures Investment styles Active or Passive management · Value or Growth investing · Hedge fund · Socially responsible investing · Impact investing · Fund of funds · Manager of managers · Index fundTheory and terminology Related topics Categories:- Financial markets

- Economic efficiency

- Economic theories

- Financial economics

- Behavioral finance

- 1900 introductions

Wikimedia Foundation. 2010.