- Automated teller machine

-

"cash machine" redirects here. For the Hard-Fi song, see Cash Machine.

An NCR Personas 75-Series interior, multi-function ATM in the United States

An NCR Personas 75-Series interior, multi-function ATM in the United States

Smaller indoor ATMs dispense money inside convenience stores and other busy areas, such as this off-premise Wincor Nixdorf mono-function ATM in Sweden

Smaller indoor ATMs dispense money inside convenience stores and other busy areas, such as this off-premise Wincor Nixdorf mono-function ATM in SwedenAn automated teller machine or automatic teller machine(ATM), also known as a Cashpoint (which is a trademark of Lloyds TSB), cash machine or sometimes a hole in the wall in British English, is a computerised telecommunications device that provides the clients of a financial institution with access to financial transactions in a public space without the need for a cashier, human clerk or bank teller. ATMs are known by various other names including ATM machine, automated banking machine, and various regional variants derived from trademarks on ATM systems held by particular banks.

Invented by John Shepherd-Barron, the first ATM was introduced in June 1967 at Barclays Bank in Enfield, UK. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smart card with a chip, that contains a unique card number and some security information such as an expiration date or CVVC (CVV). Authentication is provided by the customer entering a personal identification number (PIN).

Using an ATM, customers can access their bank accounts in order to make cash withdrawals, credit card cash advances, and check their account balances as well as purchase prepaid cellphone credit. If the currency being withdrawn from the ATM is different from that which the bank account is denominated in (e.g.: Withdrawing Japanese Yen from a bank account containing US Dollars), the money will be converted at a wholesale exchange rate. Thus, ATMs often provide the best possible exchange rate for foreign travelers and are heavily used for this purpose as well.[1]

Contents

History

An old Nixdorf ATM

An old Nixdorf ATMThe idea of self-service in retail banking developed through independent and simultaneous efforts in Japan, Sweden, the United Kingdom and the United States. In the USA, Luther George Simjian has been credited with developing and building the first cash dispenser machine.[2] There is strong evidence to suggest that Simjian worked on this device before 1959 while his 132nd patent (US3079603) was first filed on 30 June 1960 (and granted 26 February 1963). The rollout of this machine, called Bankograph, was delayed a couple of years. This was due in part to Simjian's Reflectone Electronics Inc. being acquired by Universal Match Corporation.[3] An experimental Bankograph was installed in New York City in 1961 by the City Bank of New York, but removed after 6 months due to the lack of customer acceptance. The Bankograph was an automated envelope deposit machine (accepting coins, cash and cheques) and it did not have cash dispensing features.[4]

A first cash dispensing device was used in Tokyo in 1966.[5][6] Although little is known of this first device, it seems to have been activated with a credit card rather than accessing current account balances. It was followed in 1967 by a machine in Uppsala.[7]

Reg Varney, first to use a cashpoint in the UK

Reg Varney, first to use a cashpoint in the UK Plaque commemorating installation of world's first bank cash machine

Plaque commemorating installation of world's first bank cash machineIn simultaneous and independent efforts, engineers in Sweden and Britain developed their own cash machines during the early 1960s. The first of these that was put into use was by Barclays Bank in Enfield Town in North London, United Kingdom,[8] on 27 June 1967. This machine was the first in the UK and was used by English comedy actor Reg Varney, at the time so as to ensure maximum publicity for the machines that were to become mainstream in the UK. This instance of the invention has been credited to John Shepherd-Barron of printing firm De La Rue,[9] who was awarded an OBE in the 2005 New Year's Honours List.[10] His design used special cheques that were matched with a personal identification number, as plastic bank cards had not yet been invented.[11]

The Barclays-De La Rue machine (called De La Rue Automatic Cash System or DACS)[12] beat the Swedish saving banks' and a company called Metior's machine (a device called Bankomat) by nine days and Westminster Bank’s-Smith Industries-Chubb system (called Chubb MD2) by a month. The collaboration of a small start-up called Speytec and Midland Bank developed a third machine which was marketed after 1969 in Europe and the USA by the Burroughs Corporation. The patent for this device (GB1329964) was filed on September 1969 (and granted in 1973) by John David Edwards, Leonard Perkins, John Henry Donald, Peter Lee Chappell, Sean Benjamin Newcombe & Malcom David Roe.

Both the DACS and MD2 accepted only a single-use token or voucher which was retained by the machine while the Speytec worked with a card with a magnetic strip at the back. They used principles including Carbon-14 and low-coercivity magnetism in order to make fraud more difficult. The idea of a PIN stored on the card was developed by a British engineer working on the MD2 named James Goodfellow in 1965 (patent GB1197183 filed on 2 May 1966 with Anthony Davies). The essence of this system was that it enabled the verification of the customer with the debited account without human intervention. This patent is also the earliest instance of a complete “currency dispenser system” in the patent record. This patent was filed on 5 March 1968 in the USA (US 3543904) and granted on 1 December 1970. It had a profound influence on the industry as a whole. Not only did future entrants into the cash dispenser market such as NCR Corporation and IBM licence Goodfellow’s PIN system, but a number of later patents reference this patent as “Prior Art Device”.[13]

After looking first hand at the experiences in Europe, in 1968 the networked ATM was pioneered in the US, in Dallas, Texas, by Donald Wetzel, who was a department head at an automated baggage-handling company called Docutel. On September 2, 1969, Chemical Bank installed the first ATM in the U.S. at its branch in Rockville Centre, New York. The first ATMs were designed to dispense a fixed amount of cash when a user inserted a specially coded card.[14] A Chemical Bank advertisement boasted "On Sept. 2 our bank will open at 9:00 and never close again."[15] Chemicals' ATM, initially known as a Docuteller was designed by Donald Wetzel and his company Docutel. Chemical executives were initially hesitant about the electronic banking transition given the high cost of the early machines. Additionally, executives were concerned that customers would resist having machines handling their money.[16] In 1995, the Smithsonian National Museum of American History recognised Docutel and Wetzel as the inventors of the networked ATM.[17]

ATMs first came into use in December 1972 in the UK; the IBM 2984 was designed at the request of Lloyds Bank. The 2984 CIT (Cash Issuing Terminal) was the first true Cashpoint, similar in function to today's machines; Cashpoint is still a registered trademark of Lloyds TSB in the UK. All were online and issued a variable amount which was immediately deducted from the account. A small number of 2984s were supplied to a US bank. Notable[citation needed] historical models of ATMs include the IBM 3624 and 473x series, Diebold 10xx and TABS 9000 series, NCR 1780 and earlier NCR 770 series.

Location

An ATM Encrypting PIN Pad (EPP) with German markings

An ATM Encrypting PIN Pad (EPP) with German markings ATM in Vatican with menu in Latin language

ATM in Vatican with menu in Latin languageATMs are placed not only near or inside the premises of banks, but also in locations such as shopping centers/malls, airports, grocery stores, petrol/gas stations, restaurants, or anywhere frequented by large numbers of people. There are two types of ATM installations: on- and off-premise. On-premise ATMs are typically more advanced, multi-function machines that complement a bank branch's capabilities, and are thus more expensive. Off-premise machines are deployed by financial institutions and Independent Sales Organizations (ISOs) where there is a simple need for cash, so they are generally cheaper mono-function devices. In Canada, ABMs not operated by a financial institution are known as "White Label ABMs".

In North America banks often have drive-thru lanes providing access to ATMs.

Many ATMs have a sign above them, called a topper, indicating the name of the bank or organization owning the ATM and possibly including the list of ATM networks to which that machine is connected.

Financial networks

An ATM in the Netherlands. The logos of a number of interbank networks this ATM is connected to are shown

An ATM in the Netherlands. The logos of a number of interbank networks this ATM is connected to are shownMost ATMs are connected to interbank networks, enabling people to withdraw and deposit money from machines not belonging to the bank where they have their account or in the country where their accounts are held (enabling cash withdrawals in local currency). Some examples of interbank networks include PULSE, PLUS, Cirrus, Interac, Interswitch, STAR, and LINK.

ATMs rely on authorization of a financial transaction by the card issuer or other authorizing institution via the communications network. This is often performed through an ISO 8583 messaging system.

Many banks charge ATM usage fees. In some cases, these fees are charged solely to users who are not customers of the bank where the ATM is installed; in other cases, they apply to all users.

In order to allow a more diverse range of devices to attach to their networks, some interbank networks have passed rules expanding the definition of an ATM to be a terminal that either has the vault within its footprint or utilizes the vault or cash drawer within the merchant establishment, which allows for the use of a scrip cash dispenser.

A Diebold 1063ix with a dial-up modem visible at the base

A Diebold 1063ix with a dial-up modem visible at the baseATMs typically connect directly to their host or ATM Controller via either ADSL or dial-up modem over a telephone line or directly via a leased line. Leased lines are preferable to POTS lines because they require less time to establish a connection. Leased lines may be comparatively expensive to operate versus a POTS line, meaning less-trafficked machines will usually rely on a dial-up modem. That dilemma may be solved as high-speed Internet VPN connections become more ubiquitous. Common lower-level layer communication protocols used by ATMs to communicate back to the bank include SNA over SDLC, TC500 over Async, X.25, and TCP/IP over Ethernet.

In addition to methods employed for transaction security and secrecy, all communications traffic between the ATM and the Transaction Processor may also be encrypted via methods such as SSL.[18]

Global use

There are no hard international or government-compiled numbers totaling the complete number of ATMs in use worldwide. Estimates developed by ATMIA place the number of ATMs in use currently at over 2.2 million.[19]

For the purpose of analyzing ATM usage around the world, financial institutions generally divide the world into seven regions, due to the penetration rates, usage statistics, and features deployed. Four regions (USA, Canada, Europe, and Japan) have high numbers of ATMs per million people.[20][21] Despite the large number of ATMs, there is additional demand for machines in the Asia/Pacific area as well as in Latin America.[22][23] ATMs have yet to reach high numbers in the Near East/Africa.[24]

The world's most northerly installed ATM is located at Longyearbyen, Svalbard, Norway.[citation needed]

The world's most southerly installed ATM is located at McMurdo Station, Antarctica.[25]

While India claims to have the world's highest installed ATM at Nathu La Pass, India installed by the Union Bank of India at 4310 meters, there are higher ATMs installed in Nagchu County, Tibet at 4500 meters by Agricultural Bank of China.[26][27]

Israel has the world's lowest installed ATM at Ein Bokek at the Dead Sea, installed independently by a grocery store at 421 meters below sea level.[28]

While ATMs are ubiquitous on modern cruise ships, ATMs can also be found on some US Navy ships.[29]

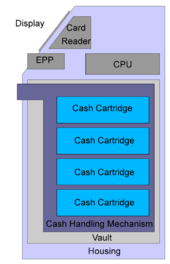

Hardware

A block diagram of an ATM

A block diagram of an ATMAn ATM is typically made up of the following devices:

- CPU (to control the user interface and transaction devices)

- Magnetic and/or Chip card reader (to identify the customer)

- PIN Pad (similar in layout to a Touch tone or Calculator keypad), often manufactured as part of a secure enclosure.

- Secure cryptoprocessor, generally within a secure enclosure.

- Display (used by the customer for performing the transaction)

- Function key buttons (usually close to the display) or a Touchscreen (used to select the various aspects of the transaction)

- Record Printer (to provide the customer with a record of their transaction)

- Vault (to store the parts of the machinery requiring restricted access)

- Housing (for aesthetics and to attach signage to)

Recently[when?], due to heavier computing demands and the falling price of computer-like architectures, ATMs have moved away from custom hardware architectures using microcontrollers and/or application-specific integrated circuits to adopting the hardware architecture of a personal computer, such as, USB connections for peripherals, ethernet and IP communications, and use personal computer operating systems. Although it is undoubtedly cheaper to use commercial off-the-shelf hardware, it does make ATMs potentially vulnerable to the same sort of problems exhibited by conventional computers.

Business owners often lease ATM terminals from ATM service providers.

The vault of an ATM is within the footprint of the device itself and is where items of value are kept. Scrip cash dispensers do not incorporate a vault.

Mechanisms found inside the vault may include:

- Dispensing mechanism (to provide cash or other items of value)

- Deposit mechanism including a Check Processing Module and Bulk Note Acceptor (to allow the customer to make deposits)

- Security sensors (Magnetic, Thermal, Seismic, gas)

- Locks: (to ensure controlled access to the contents of the vault)

- Journaling systems; many are electronic (a sealed flash memory device based on proprietary standards) or a solid-state device (an actual printer) which accrues all records of activity including access timestamps, number of bills dispensed, etc. - This is considered sensitive data and is secured in similar fashion to the cash as it is a similar liability.

ATM vaults are supplied by manufacturers in several grades. Factors influencing vault grade selection include cost, weight, regulatory requirements, ATM type, operator risk avoidance practices, and internal volume requirements.[30] Industry standard vault configurations include Underwriters Laboratories UL-291 "Business Hours" and Level 1 Safes,[31] RAL TL-30 derivatives,[32] and CEN EN 1143-1 - CEN III and CEN IV.[33][34]

ATM manufacturers recommend that vaults be attached to the floor to prevent theft.[35]

Software

With the migration to commodity PC hardware, standard commercial "off-the-shelf" operating systems and programming environments can be used inside of ATMs. Typical platforms previously used in ATM development include RMX or OS/2. Today the vast majority of ATMs worldwide use a Microsoft OS, primarily Windows XP Professional or Windows XP Embedded.

A small number of deployments may still be running older versions such as Windows NT, Windows CE or Windows 2000. There is a computer industry security view or consensus that desktop operating systems have greater risks as operating systems for cash dispensing machines than other types of operating systems like (secure) real-time operating systems (RTOS). RISKS Digest has many articles about cash machine operating system vulnerabilities.[36]

Linux is also finding some reception in the ATM marketplace. An example of this is Banrisul, the largest bank in the south of Brazil, which has replaced the MS-DOS operating systems in its ATMs with Linux. Banco do Brasil is also migrating ATMs to Linux.

Common application layer transaction protocols, such as Diebold 91x (911 or 912) and NCR NDC or NDC+ provide emulation of older generations of hardware on newer platforms with incremental extensions made over time to address new capabilities, although companies like NCR continuously improve these protocols issuing newer versions (e.g. NCR's AANDC v3.x.y, where x.y are subversions). Most major ATM manufacturers provide software packages that implement these protocols. Newer protocols such as IFX have yet to find wide acceptance by transaction processors.[37]

With the move to a more standardized software base, financial institutions have been increasingly interested in the ability to pick and choose the application programs that drive their equipment. WOSA/XFS, now known as CEN XFS (or simply XFS), provides a common API for accessing and manipulating the various devices of an ATM. J/XFS is a Java implementation of the CEN XFS API.

While the perceived benefit of XFS is similar to the Java's "Write once, run anywhere" mantra, often different ATM hardware vendors have different interpretations of the XFS standard. The result of these differences in interpretation means that ATM applications typically use a middleware to even out the differences between various platforms.

With the onset of Windows operating systems and XFS on ATM's, the software applications have the ability to become more intelligent. This has created a new breed of ATM applications commonly referred to as programmable applications. These types of applications allows for an entirely new host of applications in which the ATM terminal can do more than only communicate with the ATM switch. It is now empowered to connected to other content servers and video banking systems.

Notable ATM software that operates on XFS platforms include Triton PRISM, Diebold Agilis EmPower, NCR APTRA Edge, Absolute Systems AbsoluteINTERACT, KAL Kalignite, Phoenix Interactive VISTAatm, and Wincor Nixdorf ProTopas.

With the move of ATMs to industry-standard computing environments, concern has risen about the integrity of the ATM's software stack.[38]

Security

Security, as it relates to ATMs, has several dimensions. ATMs also provide a practical demonstration of a number of security systems and concepts operating together and how various security concerns are dealt with.

Physical

Early ATM security focused on making the ATMs invulnerable to physical attack; they were effectively safes with dispenser mechanisms. A number of attacks on ATMs resulted, with thieves attempting to steal entire ATMs by ram-raiding.[39] Since late 1990s, criminal groups operating in Japan improved ram-raiding by stealing and using a truck loaded with a heavy construction machinery to effectively demolish or uproot an entire ATM and any housing to steal its cash.[40]

Another attack method, plofkraak, is to seal all openings of the ATM with silicone and fill the vault with a combustible gas or to place an explosive inside, attached, or near the ATM. This gas or explosive is ignited and the vault is opened or distorted by the force of the resulting explosion and the criminals can break in.[41] This type of theft has occurred in the Netherlands, Belgium, France, Denmark, Germany and Australia.[42][43] This type of attacks can be prevented by a number of gas explosion prevention devices also known as gas suppression system. These systems use explosive gas detection sensor to detect explosive gas and to neutralize it by releasing a special explosion suppression chemical which changes the composition of the explosive gas and renders it ineffective.

Modern ATM physical security, per other modern money-handling security, concentrates on denying the use of the money inside the machine to a thief, by using different types of Intelligent Banknote Neutralisation Systems.

A common method is to simply rob the staff filling the machine with money. To avoid this, the schedule for filling them is kept secret, varying and random. The money is often kept in cassettes, which will dye the money if incorrectly opened.

Transactional secrecy and integrity

A Triton brand ATM with a dip style card reader and a triple DES keypad

A Triton brand ATM with a dip style card reader and a triple DES keypadThe security of ATM transactions relies mostly on the integrity of the secure cryptoprocessor: the ATM often uses commodity components that are not considered to be "trusted systems".

Encryption of personal information, required by law in many jurisdictions, is used to prevent fraud. Sensitive data in ATM transactions are usually encrypted with DES, but transaction processors now usually require the use of Triple DES.[44] Remote Key Loading techniques may be used to ensure the secrecy of the initialization of the encryption keys in the ATM. Message Authentication Code (MAC) or Partial MAC may also be used to ensure messages have not been tampered with while in transit between the ATM and the financial network.

Customer identity integrity

A BTMU ATM with a palm scanner (to the right of the screen)

A BTMU ATM with a palm scanner (to the right of the screen)There have also been a number of incidents of fraud by Man-in-the-middle attacks, where criminals have attached fake keypads or card readers to existing machines. These have then been used to record customers' PINs and bank card information in order to gain unauthorized access to their accounts. Various ATM manufacturers have put in place countermeasures to protect the equipment they manufacture from these threats.[45][46]

Alternate methods to verify cardholder identities have been tested and deployed in some countries, such as finger and palm vein patterns,[47] iris, and facial recognition technologies. However, recently[when?], cheaper mass production equipment has been developed and is being installed in machines globally that detect the presence of foreign objects on the front of ATMs, current tests have shown 99% detection success for all types of skimming devices.[48]

Device operation integrity

ATMs that are exposed to the outside must be vandal and weather resistant

ATMs that are exposed to the outside must be vandal and weather resistantOpenings on the customer-side of ATMs are often covered by mechanical shutters to prevent tampering with the mechanisms when they are not in use. Alarm sensors are placed inside the ATM and in ATM servicing areas to alert their operators when doors have been opened by unauthorized personnel.

Rules are usually set by the government or ATM operating body that dictate what happens when integrity systems fail. Depending on the jurisdiction, a bank may or may not be liable when an attempt is made to dispense a customer's money from an ATM and the money either gets outside of the ATM's vault, or was exposed in a non-secure fashion, or they are unable to determine the state of the money after a failed transaction.[49] Bank customers often complain that banks have made it difficult to recover money lost in this way, but this is often complicated by the bank's own internal policies regarding suspicious activities typical of the criminal element.[50]

Customer security

Dunbar Armored ATM Techs watching over ATMs that have been installed in a van

Dunbar Armored ATM Techs watching over ATMs that have been installed in a vanIn some countries, multiple security cameras and security guards are a common feature.[51] In the United States, The New York State Comptroller's Office has criticized the New York State Department of Banking for not following through on safety inspections of ATMs in high crime areas.[52]

Critics of ATM operators assert that the issue of customer security appears to have been abandoned by the banking industry;[53] it has been suggested that efforts are now more concentrated on deterrent legislation than on solving the problem of forced withdrawals.[54]

At least as far back as July 30, 1986, critics of the industry have called for the adoption of an emergency PIN system for ATMs, where the user is able to send a silent alarm in response to a threat.[55] Legislative efforts to require an emergency PIN system have appeared in Illinois,[56] Kansas[57] and Georgia,[58] but none have succeeded as of yet. In January 2009, Senate Bill 1355 was proposed in the Illinois Senate that revisits the issue of the reverse emergency PIN system.[59] The bill is again resisted by the banking lobby and supported by the police.[60]

In 1998 three towns outside of Cleveland, Ohio, in response to an ATM crime wave, adopted ATM Consumer Security Legislation requiring that a 9-1-1 switch be installed at all outside ATMs within their jurisdiction. Since the passing of these laws 11 years ago, there have been no repeat crimes. In the wake of an ATM Murder in Sharon Hill, Pennsylvania, The City Council of Sharon Hill passed an ATM Consumer Security Bill as well, with the same result. As of July 2009, ATM Consumer Security Legislation is currently pending in New York, New Jersey, and Washington D.C.

In China, many efforts to promote security have been made. On-premises ATMs are often located inside the bank's lobby which may be accessible 24 hours a day. These lobbies have extensive CCTV coverage, an emergency telephone and a security guard on the premises. Bank lobbies that are not guarded 24 hours a day may also have secure doors that can only be opened from outside by swiping your bank card against a wall-mounted scanner, allowing the bank to identify who enters the building. Most ATMs will also display on-screen safety warnings and may also be fitted with convex mirrors above the display allowing the user to see what is happening behind them.

Alternative uses

Two NCR Personas 84 ATMs at a bank in Jersey dispensing two types of pound sterling banknotes: Bank of England notes on the left, and States of Jersey notes on the right

Two NCR Personas 84 ATMs at a bank in Jersey dispensing two types of pound sterling banknotes: Bank of England notes on the left, and States of Jersey notes on the rightAlthough ATMs were originally developed as just cash dispensers, they have evolved to include many other bank-related functions. In some countries, especially those which benefit from a fully integrated cross-bank ATM network (e.g.: Multibanco in Portugal), ATMs include many functions which are not directly related to the management of one's own bank account, such as:

- Deposit currency recognition, acceptance, and recycling[61][62]

- Paying routine bills, fees, and taxes (utilities, phone bills, social security, legal fees, taxes, etc.)

- Printing bank statements

- Updating passbooks

- Loading monetary value into stored value cards

- Purchasing

- Postage stamps.

- Lottery tickets

- Train tickets

- Concert tickets

- Movie tickets

- Shopping mall gift certificates.

- Games and promotional features[63]

- Fastloans

- CRM at the ATM

- Donating to charities[64]

- Cheque Processing Module

- Adding pre-paid cell phone / mobile phone credit.

- Paying (in full or partially) the credit balance on a card linked to a specific current account.

- Transferring money between linked accounts (such as transferring between checking and savings accounts)

- Gold - "In London last week [in 2011] some smart businessmen launched the country’s first gold ATM. Stick in your credit card or some cash, and the machine will swap your plastic or paper money for a small bar of the real stuff."[65]

Increasingly banks are seeking to use the ATM as a sales device to deliver pre approved loans and targeted advertising using products such as ITM (the Intelligent Teller Machine) from Aptra Relate from NCR. ATMs can also act as an advertising channel for companies to advertise their own products or third-party products and services.[66]

In Canada, ATMs are called guichets automatiques in French and sometimes "Bank Machines" in English. The Interac shared cash network does not allow for the selling of goods from ATMs due to specific security requirements for PIN entry when buying goods.[67] CIBC machines in Canada, are able to top-up the minutes on certain pay as you go phones.

A South Korean ATM with mobile bank port and bar code reader

A South Korean ATM with mobile bank port and bar code readerManufacturers have demonstrated and have deployed several different technologies on ATMs that have not yet reached worldwide acceptance, such as:

- Biometrics, where authorization of transactions is based on the scanning of a customer's fingerprint, iris, face, etc. Biometrics on ATMs can be found in Asia.[68][69][70]

- Cheque/Cash Acceptance, where the ATM accepts and recognise cheques and/or currency without using envelopes[71] Expected to grow in importance in the US through Check 21 legislation.

- Bar code scanning[72]

- On-demand printing of "items of value" (such as movie tickets, traveler's cheques, etc.)

- Dispensing additional media (such as phone cards)

- Co-ordination of ATMs with mobile phones[73]

- Customer-specific advertising[74]

- Integration with non-banking equipment[75][76]

Reliability

Before an ATM is placed in a public place, it typically has undergone extensive testing with both test money and the backend computer systems that allow it to perform transactions. Banking customers also have come to expect high reliability in their ATMs,[77] which provides incentives to ATM providers to minimize machine and network failures. Financial consequences of incorrect machine operation also provide high degrees of incentive to minimize malfunctions.[78]

ATMs and the supporting electronic financial networks are generally very reliable, with industry benchmarks typically producing 98.25% customer availability for ATMs[79] and up to 99.999% availability for host systems. If ATMs do go out of service, customers could be left without the ability to make transactions until the beginning of their bank's next time of opening hours.

This said, not all errors are to the detriment of customers; there have been cases of machines giving out money without debiting the account, or giving out higher value notes as a result of incorrect denomination of banknote being loaded in the money cassettes. Errors that can occur may be mechanical (such as card transport mechanisms; keypads; hard disk failures; envelope deposit mechanisms); software (such as operating system; device driver; application); communications; or purely down to operator error.

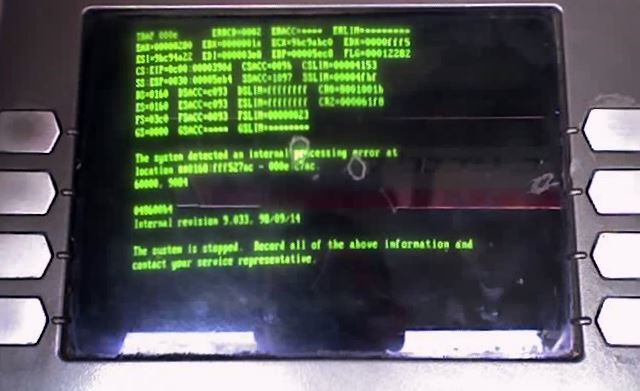

An ATM running OS/2 that has crashed

An ATM running OS/2 that has crashedTo aid in reliability, some ATMs print each transaction to a roll paper journal that is stored inside the ATM, which allows both the users of the ATMs and the related financial institutions to settle things based on the records in the journal in case there is a dispute. In some cases, transactions are posted to an electronic journal to remove the cost of supplying journal paper to the ATM and for more convenient searching of data.

Improper money checking can cause the possibility of a customer receiving counterfeit banknotes from an ATM. While bank personnel are generally trained better at spotting and removing counterfeit cash,[80][81] the resulting ATM money supplies used by banks provide no guarantee for proper banknotes, as the Federal Criminal Police Office of Germany has confirmed that there are regularly incidents of false banknotes having been dispensed through bank ATMs.[82] Some ATMs may be stocked and wholly owned by outside companies, which can further complicate this problem. Bill validation technology can be used by ATM providers to help ensure the authenticity of the cash before it is stocked in an ATM; ATMs that have cash recycling capabilities include this capability.[83]

Fraud

As with any device containing objects of value, ATMs and the systems they depend on to function are the targets of fraud. Fraud against ATMs and people's attempts to use them takes several forms.

The first known instance of a fake ATM was installed at a shopping mall in Manchester, Connecticut in 1993. By modifying the inner workings of a Fujitsu model 7020 ATM, a criminal gang known as The Bucklands Boys were able to steal information from cards inserted into the machine by customers.[84]

In some cases, bank fraud could occur at ATMs whereby the bank accidentally stocks the ATM with bills in the wrong denomination, therefore giving the customer more money than should be dispensed.[85] The result of receiving too much money may be influenced by the card holder agreement in place between the customer and the bank.[86][87]

In a variation of this, WAVY-TV reported an incident in Virginia Beach of September 2006 where a hacker who had probably obtained a factory-default admin password for a gas station's white label ATM caused the unit to assume it was loaded with $5 USD bills instead of $20s, enabling himself—and many subsequent customers—to walk away with four times the money they said they wanted to withdraw.[88] This type of scam was featured on the TV series The Real Hustle.

ATM behavior can change during what is called "stand-in" time, where the bank's cash dispensing network is unable to access databases that contain account information (possibly for database maintenance). In order to give customers access to cash, customers may be allowed to withdraw cash up to a certain amount that may be less than their usual daily withdrawal limit, but may still exceed the amount of available money in their account, which could result in fraud.[89]

Card fraud

ATM lineup

ATM lineup

In an attempt to prevent criminals from shoulder surfing the customer's PINs, some banks draw privacy areas on the floor.

For a low-tech form of fraud, the easiest is to simply steal a customer's card. A later variant of this approach is to trap the card inside of the ATM's card reader with a device often referred to as a Lebanese loop. When the customer gets frustrated by not getting the card back and walks away from the machine, the criminal is able to remove the card and withdraw cash from the customer's account.

Another simple form of fraud involves attempting to get the customer's bank to issue a new card and stealing it from their mail.[90]

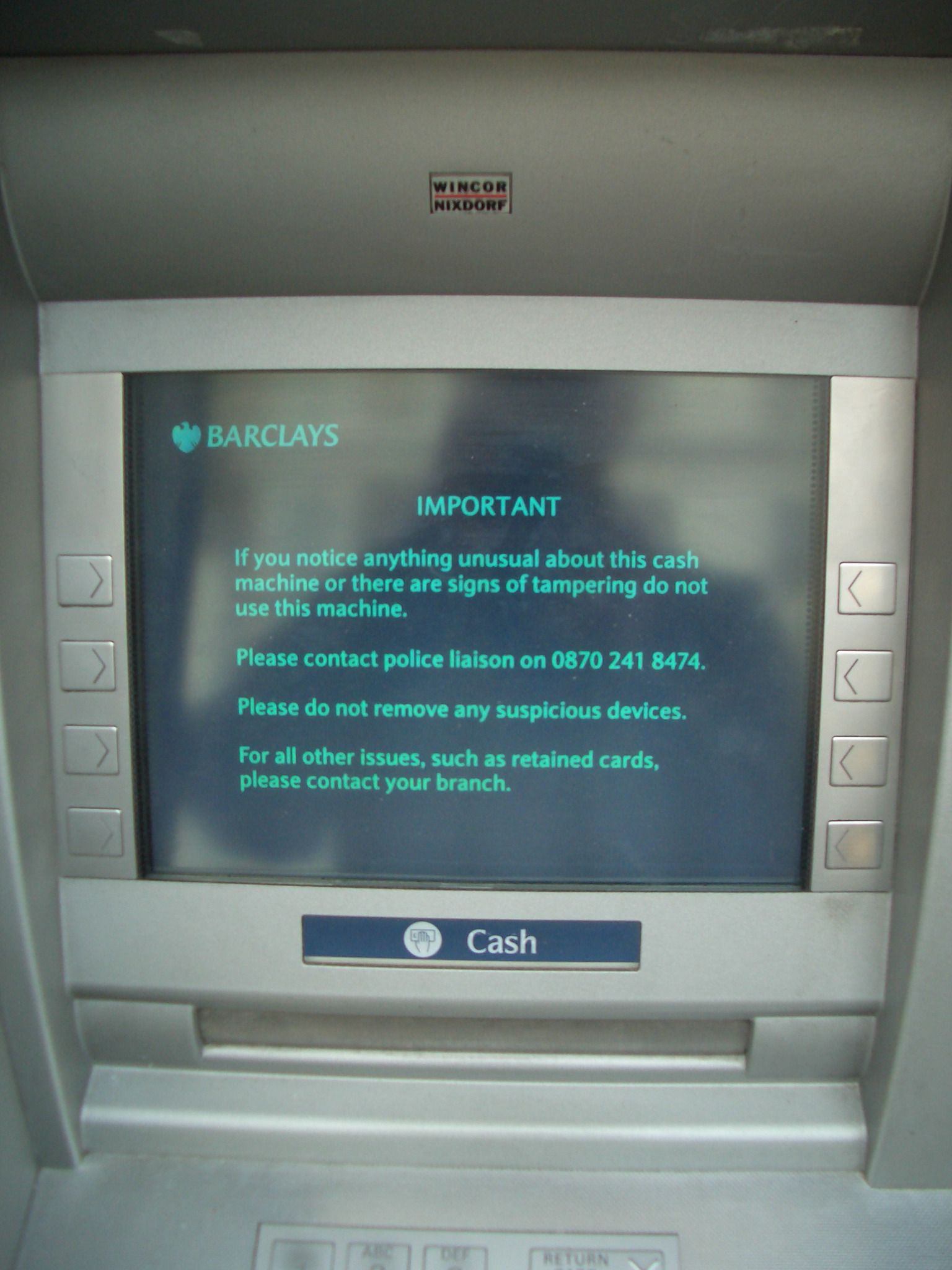

Some ATMs may put up warning messages to customers to not use them when it detects possible tampering

Some ATMs may put up warning messages to customers to not use them when it detects possible tamperingThe concept and various methods of copying the contents of an ATM card's magnetic stripe on to a duplicate card to access other people's financial information was well known in the hacking communities by late 1990.[91]

In 1996 Andrew Stone, a computer security consultant from Hampshire in the UK, was convicted of stealing more than £1 million by pointing high definition video cameras at ATMs from a considerable distance, and by recording the card numbers, expiry dates, etc. from the embossed detail on the ATM cards along with video footage of the PINs being entered. After getting all the information from the videotapes, he was able to produce clone cards which not only allowed him to withdraw the full daily limit for each account, but also allowed him to sidestep withdrawal limits by using multiple copied cards. In court, it was shown that he could withdraw as much as £10,000 per hour by using this method. Stone was sentenced to five years and six months in prison.[92]

By contrast, a newer high-tech method of operating sometimes called card skimming or card cloning involves the installation of a magnetic card reader over the real ATM's card slot and the use of a wireless surveillance camera or a modified digital camera to observe the user's PIN. Card data is then cloned onto a second card and the criminal attempts a standard cash withdrawal. The availability of low-cost commodity wireless cameras and card readers has made it a relatively simple form of fraud, with comparatively low risk to the fraudsters.[93]

In an attempt to stop these practices, countermeasures against card cloning have been developed by the banking industry, in particular by the use of smart cards which cannot easily be copied or spoofed by unauthenticated devices, and by attempting to make the outside of their ATMs tamper evident. Older chip-card security systems include the French Carte Bleue, Visa Cash, Mondex, Blue from American Express[94] and EMV '96 or EMV 3.11. The most actively developed form of smart card security in the industry today is known as EMV 2000 or EMV 4.x.

EMV is widely used in the UK (Chip and PIN) and other parts of Europe, but when it is not available in a specific area, ATMs must fallback to using the easy–to–copy magnetic stripe to perform transactions. This fallback behaviour can be exploited.[95] However the fallback option has been removed by several UK banks, meaning if the chip is not read, the transaction will be declined.

In February 2009, a group of criminals used counterfeit ATM cards to steal $9 million from 130 ATMs in 49 cities around the world all within a time period of 30 minutes.[96]

Card cloning and skimming can be detected by the implementation of magnetic card reader heads and firmware that can read a signature embedded in all magnetic stripes during the card production process. This signature known as a "MagnePrint" or "BluPrint" can be used in conjunction with common two factor authentication schemes utilized in ATM, debit/retail point-of-sale and prepaid card applications.[citation needed]

Another ATM fraud issue is ATM card theft which includes credit card trapping and debit card trapping at ATMs. Originating in South America this type of ATM fraud has spread globally. Although somewhat replaced in terms of volume by ATM skimming incidents, a re-emergence of card trapping has been noticed in regions such as Europe where EMV Chip and PIN cards have increased in circulation.[97]

Related devices

A Talking ATM is a type of ATM that provides audible instructions so that persons who cannot read an ATM screen can independently use the machine. All audible information is delivered privately through a standard headphone jack on the face of the machine. Alternatively, some banks such as the Nordea and Swedbank use a built-in external speaker which may be invoked by pressing the talk button on the keypad.[98] Information is delivered to the customer either through pre-recorded sound files or via text-to-speech speech synthesis.

A postal interactive kiosk may also share many of the same components as an ATM (including a vault), but only dispenses items relating to postage.[99][100]

A scrip cash dispenser may share many of the same components as an ATM, but lacks the ability to dispense physical cash and consequently requires no vault. Instead, the customer requests a withdrawal transaction from the machine, which prints a receipt. The customer then takes this receipt to a nearby sales clerk, who then exchanges it for cash from the till.[101]

A Teller Assist Unit may also share many of the same components as an ATM (including a vault), but they are distinct in that they are designed to be operated solely by trained personnel and not the general public, they do not integrate directly into interbank networks, and are usually controlled by a computer that is not directly integrated into the overall construction of the unit.

See also

A Restaurant advertising its ATM availability

A Restaurant advertising its ATM availability- Automated cash handling

- Security of automated teller machines

- Banknote counter

- Cash register

- EFTPOS

- Electronic funds transfer

- Financial cryptography

- Key management

- List of companies involved with ATMs

- Payroll

- Phantom withdrawal

- RAS syndrome

- Verification and validation

References

- ^ Schlichter, Sarah (2007-02-05). "Using ATM's abroad - Travel - Travel Tips - msnbc.com". MSNBC. http://www.msnbc.msn.com/id/16994358/. Retrieved 2011-02-11.

- ^ "Inventor of the Week: Archive". Web.mit.edu. http://web.mit.edu/invent/iow/simjian.html. Retrieved 2011-02-11.

- ^ 'Universal Match Maps Acquisition’, The New York Times, 22 March 1961

- ^ ‘Machine Accepts Cash Deposits’, The New York Times, 12 April 1961

- ^ 'Fast Machine with a Buck', Pacific Stars and Stripes, p. 7, 14 July 1966

- ^ ‘Instant Cash via Credit Cards’, ABA Banking Journal, p. 99, January 1967

- ^ Ny Teknik: Premiär för pengar ur väggen

- ^ "Enfield's cash gift to the world". BBC London. 27 June 2007. http://www.bbc.co.uk/london/content/articles/2007/06/26/cash_machine_feature.shtml.

- ^ Milligan, Brian (25 June 2007). "The man who invented the cash machine". BBC News. http://news.bbc.co.uk/2/hi/business/6230194.stm. Retrieved 26 April 2010.

- ^ "ATM inventor honoured". BBC News. 31 December 2004. http://news.bbc.co.uk/2/hi/uk_news/scotland/4135269.stm. Retrieved 26 April 2010.

- ^ "ATM inventor John Shepherd-Barron dies at age of 84 on 20th May 2010". The LA Times, May 19, 2010. 19 May 2010. http://latimesblogs.latimes.com/afterword/2010/05/atm-inventor-john-shepherdbarron-dies-at-84.html.

- ^ Mary Bellis. The ATM of John Shepherd Barron. About.com. Retrieved 2011-04-29.

- ^ B. Batiz-Lazo and R. J. K. Reid. "Evidence from the patent record on the development of cash dispensing technology". History of Telecommunications Conference, 2008. Histelcon 2008. IEEE. http://ieeexplore.ieee.org/xpl/freeabs_all.jsp?arnumber=4668724.

- ^ 1969: the year everything changed - Google Books. Books.google.com. http://books.google.com/books?id=XZMrIchANY4C&pg=PA266. Retrieved 2011-02-11.

- ^ Popular Mechanics - Google Books. Books.google.com. http://books.google.com/books?id=BtEDAAAAMBAJ&lpg=PA84&pg=PA84. Retrieved 2011-02-11.

- ^ "Interview with Mr. Don Wetzel". Americanhistory.si.edu. http://americanhistory.si.edu/collections/comphist/wetzel.htm. Retrieved 2011-02-11.

- ^ "Automatic teller machine". The History of Computing Project. Thocp.net. 17 April 2006. http://www.thocp.net/hardware/atm.htm. Retrieved 2011-02-11.

- ^ [1][dead link]

- ^ "ATM Industry Association Global ATM Clock". Atmia.com. http://www.atmia.com/mig/globalatmclock/. Retrieved 2011-09-15.

- ^ http://www.interac.org/en_n3_31_abmstats.html

- ^ "Statistics on payment and settlement systems in selected countries - Figures for 2004". Bis.org. 2006-03-31. http://www.bis.org/publ/cpss74.htm. Retrieved 2011-02-11.

- ^ "Central bank payment system information". Bis.org. 2001-02-05. http://www.bis.org/cpss/paysysinfo.htm. Retrieved 2011-02-11.

- ^ http://www.eiu.com/site_info.asp?info_name=eiu_Visa_accessing_payments_systems_Latin_America

- ^ http://www.bis.org/events/cbcd06e.pdf

- ^ http://antarcticsun.usap.gov/oldissues96-97/astdec15.htm

- ^ "ABC Nagqu Branch cares about rural Tibetans". En.tibet.cn. 2007-12-28. http://en.tibet.cn/news/tin/t20071228_292098.htm. Retrieved 2011-02-11.

- ^ [2][dead link]

- ^ "ים המוות מתעורר לחיים; נרשמה עלייה של 8% בלינות באיזור בשנת 2006 - צרכנות". TheMarker. http://www.themarker.com/tmc/article.jhtml?log=tag&ElementId=skira20070206_822342. Retrieved 2011-02-11.

- ^ [3][dead link]

- ^ "ATM Cash Machine Frequently Asked Questions". Atmdepot.com. http://www.atmdepot.com/help.aspx#f4. Retrieved 2011-02-11.

- ^ "Scope for UL 291". Ulstandardsinfonet.ul.com. 2004-12-21. http://ulstandardsinfonet.ul.com/scopes/scopes.asp?fn=0291.html. Retrieved 2011-02-11.

- ^ [4][dead link]

- ^ "CEN On-line catalogue - ICS: 13.310 Protection against crime" Comité Européen de Normalisation

- ^ "BSI: Standards, Training, Testing, Assessment & Certification". Bsonline.bsi-global.com. http://www.bsonline.bsi-global.com/search/item/1928003. Retrieved 2011-02-11.

- ^ "Triton Systems | ATM manufacturer". Tritonatm.com. 2010-11-17. http://www.tritonatm.com/en/service/manuals/07100-00008F%20(9100UsrMan(5.0)).pdf. Retrieved 2011-02-11.

- ^ http://catless.ncl.ac.uk/php/risks/search.php?query=cash+machine

- ^ "Messaging standard to give multiple channels a common language". selfserviceworld.com. http://www.selfserviceworld.com/article.php?id=1252. Retrieved 2011-02-11.

- ^ "Technology News: Security: Windows Cash-Machine Worm Generates Concern". Technewsworld.com. http://www.technewsworld.com/story/32350.html. Retrieved 2011-02-11.

- ^ "An end to ram raids?". ATM Marketplace. http://www.atmmarketplace.com/article.php?id=6736. Retrieved 2011-02-11.

- ^ [5][dead link]

- ^ "ATM bombings up 3000%". News24. 2008-07-12. http://www.news24.com/SouthAfrica/News/ATM-bombings-up-3000-20080712. Retrieved 2011-04-07.

- ^ http://www.theregister.co.uk/2006/03/14/exploding_atm_attack/

- ^ "Attacks on banks devised in Europe - National". smh.com.au. 2008-11-25. http://www.smh.com.au/news/national/attacks-on-banks-devised-in-europe/2008/11/25/1227491548435.html/. Retrieved 2011-02-11.

- ^ [6][dead link]

- ^ "The No. 1 ATM security concern". ATM Marketplace. http://www.atmmarketplace.com/article.php?id=7000&na=1. Retrieved 2011-02-11.

- ^ "Diebold ATM Fraud" (PDF). http://buy.cuna.org/download/diebold_fraudpaper.pdf. Retrieved 2011-02-11.

- ^ [7][dead link]

- ^ [8][dead link]

- ^ http://www.kuluttajavirasto.fi/user_nf/default_mag.asp?id=12263&lmf=11440&mode=readdoc&tmf=11440

- ^ "Title1". Moneycentral.msn.com. http://moneycentral.msn.com/content/Banking/P57803.asp. Retrieved 2011-02-11.

- ^ "NYSBD - Text of the ATM Safety Act". Banking.state.ny.us. 1997-06-01. http://www.banking.state.ny.us/legal/atmsafe.htm. Retrieved 2011-02-11.

- ^ "DiNapoli Calls for Better Oversight of Bank ATMs". Osc.state.ny.us. 2007-10-04. http://www.osc.state.ny.us/press/releases/oct07/100407.htm. Retrieved 2011-02-11.

- ^ [9][dead link]

- ^ [10][dead link]

- ^ Representative Mario Biaggi, Congressional Record, July 30, 1986, Page 18232 et seq.

- ^ "ATM Report". Obre.state.il.us. http://www.obre.state.il.us/AGENCY/News/atmrpt.htm. Retrieved 2011-02-11.

- ^ http://www.cunews.com/newsletters/2004216.htm

- ^ "sb379_SB_379_PF_2.html". Legis.state.ga.us. http://www.legis.state.ga.us/legis/2005_06/versions/sb379_SB_379_PF_2.htm. Retrieved 2011-02-11.

- ^ "Illinois General Assembly - Bill Status for SB1355". Ilga.gov. http://www.ilga.gov/legislation/BillStatus.asp?DocNum=1355&GAID=10&DocTypeID=SB&LegId=42570&SessionID=76&GA=96. Retrieved 2011-02-11.

- ^ Kravetz, Andy (2009-02-18). "ATM software aimed at reversing crime - Peoria, IL". pjstar.com. http://www.pjstar.com/news/x1745367387/ATM-software-aimed-at-reversing-crime. Retrieved 2011-02-11.

- ^ "Rising interest rates, gas prices hit vault-cash providers". selfserviceworld.com. http://www.selfserviceworld.com/article.php?id=15827&site=5&prc=. Retrieved 2011-02-11.

- ^ "NCR and Fujitsu Develop Cash Deposit and Bill Recycling Module for ATMs : Fujitsu Global". Fujitsu.com. http://www.fujitsu.com/global/news/pr/archives/month/2004/20040318.html. Retrieved 2011-02-11.

- ^ "Business | Bank puts the 'fun' into 'funds'". BBC News. 2005-07-20. http://news.bbc.co.uk/1/hi/business/4700053.stm. Retrieved 2011-02-11.

- ^ Harvey, Rachel (2006-01-10). "Asia-Pacific | Indonesians make ATM sacrifices". BBC News. http://news.bbc.co.uk/1/hi/world/asia-pacific/4597692.stm. Retrieved 2011-02-11.

- ^ Lynn, Matthew, "What will replace the dollar as global currency?: Gold? Renminbi? Maybe commodities?", MarketWatch, July 7, 2011 12:00 a.m. EDT. Retrieved 2011-07-07.

- ^ "ATM:ad First For Comic Relief". creativematch. 2005-03-10. http://www.creativematch.co.uk/?action=viewnews&ni=90724. Retrieved 2011-02-11.

- ^ http://www.interac.org/en_n3_14_consumersfaq.html

- ^ "Japan Post to go with fingerprints for ATMs | The Japan Times Online". Search.japantimes.co.jp. 2006-08-06. http://search.japantimes.co.jp/cgi-bin/nn20060806a5.html. Retrieved 2011-02-11.

- ^ ""Place Your Hand on the Scanner" | Science and Technology | Trends in Japan". Web Japan. 2005-05-10. http://web-japan.org/trends/science/sci050510.html. Retrieved 2011-02-11.

- ^ Mastrull, Diane (1996-11-11). "Sensar has its eye on the prize with $42 million Japanese deal | Philadelphia Business Journal". Bizjournals.com. http://www.bizjournals.com/philadelphia/stories/1996/11/11/story4.html. Retrieved 2011-02-11.

- ^ "BAI Banking Strategies Magazine - Articles Online". Bai.org. 2011-02-01. http://www.bai.org/nl/v1/N20/articles/V1_N20_01.asp?WT.mc_id=BSRDI_ARTICLEARCHIVE_V1_N20_01. Retrieved 2011-02-11.

- ^ "The Check is NOT in the Mail". Accurapid.com. http://accurapid.com/journal/16brasbank.htm. Retrieved 2011-02-11.

- ^ "Japanese bank to allow cellphone ATM access". Engadget. http://www.engadget.com/2006/01/27/japanese-bank-to-allow-cellphone-atm-access/. Retrieved 2011-02-11.

- ^ "Wincor Nixdorf Germany" (in (German)). Wincor-nixdorf.com. http://www.wincor-nixdorf.com/internet/se/Products/Software/Banking/MultiChannel/ProSales/index.html. Retrieved 2011-02-11.

- ^ "Industrial Automated Gas Pumping Station and ATM MCF547x ColdFire® Solutions By Freescale". Freescale.com. http://www.freescale.com/webapp/sps/site/application.jsp?nodeId=02430ZR8tt8105. Retrieved 2011-02-11.

- ^ "NRT Technology Corporation - Gaming and casino solutions: QuickJack". Nrtpos.com. http://www.nrtpos.com/html/gamingquickjack.shtml. Retrieved 2011-02-11.

- ^ "Barking Up the Wrong Tree – Factors Influencing Customer Satisfaction in Retail Banking in the UK - Page 5". Managementjournals.com. http://www.managementjournals.com/journals/marketing/article27-p5.htm. Retrieved 2011-02-11.

- ^ Rebecca Allison (2003-01-16). "ATM gives out free cash and lands family in court | UK news". London: The Guardian. http://www.guardian.co.uk/uk_news/story/0,3604,875749,00.html. Retrieved 2011-02-11.

- ^ [11][dead link]

- ^ [12][dead link]

- ^ "Materials- Bank Notes- Bank of Canada". Bankofcanada.ca. http://www.bankofcanada.ca/en/banknotes/education/index.htm. Retrieved 2011-02-11.

- ^ "Falschgeld: Blüten aus dem Geldautomat? - Wirtschaft". Stern.De. 2004-05-05. http://www.stern.de/wirtschaft/geldanlage/:Falschgeld-Bl%FCten-Geldautomat/523625.html. Retrieved 2011-02-11.

- ^ "Wincor Nixdorf Germany" (in (German)). Wincor-nixdorf.com. http://www.wincor-nixdorf.com/internet/com/Products/CashSystems/CashRecycling/ProCash3100/index.html. Retrieved 2011-02-11.

- ^ "1.05: The Bucklands Boys and Other Tales of the ATM". Wired.com. http://www.wired.com/wired/archive/1.05/atm_pr.html. Retrieved 2011-02-11.

- ^ "Double money in cash point error". BBC News. 2004-04-28. http://news.bbc.co.uk/1/hi/england/tyne/3667279.stm.

- ^ http://www.rbcroyalbank.com/cards/documentation/ch_agreements/ch_agree_client.html

- ^ "Europe | Mad rush to faulty ATM in France". BBC News. 2005-12-23. http://news.bbc.co.uk/1/hi/world/europe/4552288.stm. Retrieved 2011-02-11.

- ^ "Video". Cnn.com. 2005-06-06. http://www.cnn.com/video/player/player.html?url=/video/tech/2006/09/14/owens.va.atm.scam.wavy. Retrieved 2011-02-11.

- ^ "Kennison v Daire [1986] HCA 4; (1986) 160 CLR 129 (20 February 1986)". Austlii.edu.au. 1986-02-20. http://www.austlii.edu.au/au/cases/cth/HCA/1986/4.html. Retrieved 2011-02-11.

- ^ http://venus.soci.niu.edu/~cudigest/phracks/phrack-08

- ^ Fredric L. Rice, Organized Crime Civilian Response. "Phrack Classic Volume Three, Issue 32, File #1 of XX Phrack Classic Newsletter Issue XXXII". Skepticfiles.org. http://www.skepticfiles.org/hacker/phrack32.htm. Retrieved 2011-02-11.

- ^ Stephen Castell. "Seeking after the truth in computer evidence: any proof of ATM fraud? — ITNOW". Itnow.oxfordjournals.org. http://itnow.oxfordjournals.org/cgi/content/abstract/38/6/17. Retrieved 2011-02-11.

- ^ http://www.snopes.com/crime/warnings/atmcamera.asp

- ^ "What the Hell Do Smart Cards Do?". Fast Company. 2002-02-28. http://www.fastcompany.com/magazine/56/wth.html. Retrieved 2011-02-11.

- ^ "Tamil Nadu / Chennai News : Four more held in fake credit card racket case". Chennai, India: The Hindu. 2006-05-19. http://www.hindu.com/2006/05/19/stories/2006051920380300.htm. Retrieved 2011-02-11.

- ^ Previous post Next post. "Global ATM Caper Nets Hackers $9 Million in One Day | Threat Level". Wired.com. http://www.wired.com/threatlevel/2009/02/atm/. Retrieved 2011-02-11.

- ^ "ATM Security Issues & ATM Fraud Issues by Geography | ATMSecurity.com ATM Security news ATM Security issues ATM fraud info ATM". Atmsecurity.com. 2009-03-04. http://www.atmsecurity.com/articles/atm-fraud/atm-security-issues-atm-fraud-issues-by-geography.html. Retrieved 2011-02-11.

- ^ pepsi says: (2011-01-25). "Why is there braille on drive-up ATM machines?". Zidbits. http://zidbits.com/2011/01/25/why-is-there-braille-on-drive-up-atm-machines/. Retrieved 2011-02-11.

- ^ "Postal Service Mailing Kiosks Now In Every State". Usps.com. 2004-12-30. http://www.usps.com/communications/news/press/2004/pr04_098.htm. Retrieved 2011-02-11.

- ^ http://www.lunewsviews.com/apc.htm

- ^ "About Script ATMs: How Do Cashless ATMs Work? - What is Scrip, or Cashless Atm Machines?". Atmscrip.com. http://www.atmscrip.com/what_is_scrip.html. Retrieved 2011-02-11.

Further reading

- Brain, Marshall Marshall Brain's More How Stuff Works, John Wiley and Sons Ltd, New York, October 2002, ISBN 0-7645-6711-X

- Donley, Richard Everything has its price, Fireside Books /Simon & Schuster, New Jersey, March 1995, ISBN 0-671-89559-1

- Guile, Bruce R., Quinn, James Brian Managing Innovation Cases from the Services Industries, National Academy Press, Washington (D.C.), January 1988, ISBN 0-309-03926-6

- Hillier, David Money Transmission and the Payments Market, Financial World Publishing, Kent UK, January 2002, ISBN 0-85297-643-7

- IESNA Committee Lighting for Automatic Teller Machines, Illuminating Engineering Society of North America, January 1997, ISBN 0-87995-122-2

- Ikenson, Ben Patents: Ingenious Inventions How They Work and How They Came to Be, Gina Black Dog & Leventhal Publishers, Inc., April 2004, ISBN 1-57912-367-8

- Mcall, Susan Resolution of Banking Disputes, Sweet & Maxwell, Ltd., December 1990, ISBN 0-85121-644-7

- Peterson, Kirk Automated Teller Machine as a National Bank under the Federal Law, William S. Hein & Co., Inc., August 1987, ISBN 0-89941-587-3

- Schneier, Bruce (January 2004). Secrets and Lies: Digital Security in a Networked World. John Wiley & Sons. ISBN 0471453803.

- Zotti, Ed Triumph of the Straight Dope, Random House, February 1999, ISBN 0-345-42008-X

- The Fraudsters - How Con Artists Steal Your Money (ISBN 978-1-903582-82-4)by Eamon Dillon, published September 2008 by Merlin Publishing

External links

- Britain celebrates 40 years of the ATM

- The Money Machines: An account of U.S. ATM history; By Ellen Florian, Fortune.com

- Automated teller machine at the Open Directory Project

- World Map and Chart of Automated Teller Machines per 100,000 Adults by Lebanese-economy-forum, World Bank data

Interbank networks by region Multiregional Africa CashNet · CMI · Interswitch · SASWITCHAsia Pacific 1LINK · ACS · ALTO · atm5 · ATM Bersama · ATM Pool · BancNet · Banknetvn (Vietnam) · BANCS · Bankline · Cashnet · CashTree · Dutch Bangla Bank Nexus · eftpos

ENS · ETC · Expressnet · FISC · JETCO · EPS · Link · MICS · MEPS · MegaLink · MITR · MNET · NFS · Nationlink · Omnibus · Prima · SmartLink (Vietnam) · UnionPay · Vietnam Bank Card (VNBC) · Yucho · RuPayCaribbean Europe 4B · Altın Nokta · BamCard · BankAxept · Banklink · Bankomat · BKM · CB · DIAS · Equens · Eufiserv · Euronet · Euro 6000 · Girocard (Cash Group, CashPool, Bankcard-Servicenetz) · LINK · Multibanco · Ortak Nokta · Otto. · Sbercard · ServiRed · StarNet · Transfond · Zolotaya KoronaMiddle East North America Abby · ACCEL/Exchange · Access 24 · Acculink · Advantage · AFFN · Alaska Option · Alert · Allpoint · Annie · ARN · Award · BankMate · BOH · Cash Station · CashStream · Checkokard · CO-OP · Credit Union 24 · Credomatic · Discover Network · Easy Answer · Express · Express Teller · Fastbank · Gulfnet · HandiBank · Handy 24 · Honor · Instant Cash · Instant Teller · Interlink · Interac · Jeanie · KETS · LYNX · MAC · Magic Line · Member Access Pacific · Minibank · Money Belt · Money Network · MoneyMaker · MoneyPass · Money Station · MOST · MPact · Networks · NYCE · Peak · Presto! · PROSA · Pulse · Quest · RED · Red Total · SC 24 · Service Card System · SHAZAM · STAR · SUM · The Exchange · Transact · Paymenex · Transfund · TX Network · Tyme · Universal Money Center · Via · X-PRESS 24 · Yankee 24South America Credit, charge, and debit cards Major credit cards Major debit cards Charge cards Regional cards BC Card · Carte Bleue · China UnionPay · Dankort · Discover · Girocard (EC) · Interac · Laser · RuPay · V PAYDefunct cards Accounts Interest Payment Technology Automated teller machine · EMV · Smart card · Contactless payment · Interbank network · Credit card terminal · Magnetic stripe cardSecurity/crime Categories:- Automation

- Banking terms and equipment

- Banks

- 1969 introductions

- Embedded systems

- Payment systems

- Banking technology

- Commercial machines

Wikimedia Foundation. 2010.