- Life insurance

-

The foundation of life insurance is the recognition of the value of a human life and the possibility of indemnification for the loss of that value. —F. C. Oviatt, Economic place of insurance and its relation to society[1] Life insurance is a contract between an insurance policy holder and an insurer, where the insurer promises to pay a designated beneficiary a sum of money (the "benefits") upon the death of the insured person. Depending on the contract, other events such as terminal illness or critical illness may also trigger payment. The policy holder typically pays a premium, either regularly or as a lump sum. Other expenses (such as funeral expenses) are also sometimes included in the premium; however in the United States the predominant form simply specifies a lump sum to be paid on the policy holder's death.

The advantage for the policy owner is "peace of mind", in knowing that the death of the insured person will not result in financial hardship for loved ones.

Life policies are legal contracts and the terms of the contract describe the limitations of the insured events. Specific exclusions are often written into the contract to limit the liability of the insurer; common examples are claims relating to suicide, fraud, war, riot and civil commotion.

Life-based contracts tend to fall into two major categories:

- Protection policies – designed to provide a benefit in the event of specified event, typically a lump sum payment. A common form of this design is term insurance.

- Investment policies – where the main objective is to facilitate the growth of capital by regular or single premiums. Common forms (in the US) are whole life, universal life and variable life policies.

Contents

Overview

Parties to contract

There is a difference between the insured and the policy owner, although the owner and the insured are often the same person. For example, if Joe buys a policy on his own life, he is both the owner and the insured. But if Jane, his wife, buys a policy on Joe's life, she is the owner and he is the insured. The policy owner is the guarantor and he will be the person to pay for the policy. The insured is a participant in the contract, but not necessarily a party to it. Also, most companies allow the payer and owner to be different, e. g. a grand parent paying premiums for a policy on a child, owned by a grandchild.

The beneficiary receives policy proceeds upon the insured person's death. The owner designates the beneficiary, but the beneficiary is not a party to the policy. The owner can change the beneficiary unless the policy has an irrevocable beneficiary designation. If a policy has an irrevocable beneficiary, any beneficiary changes, policy assignments, or cash value borrowing would require the agreement of the original beneficiary.

In cases where the policy owner is not the insured (also referred to as the celui qui vit or CQV), insurance companies have sought to limit policy purchases to those with an insurable interest in the CQV. For life insurance policies, close family members and business partners will usually be found to have an insurable interest. The insurable interest requirement usually demonstrates that the purchaser will actually suffer some kind of loss if the CQV dies. Such a requirement prevents people from benefiting from the purchase of purely speculative policies on people they expect to die. With no insurable interest requirement, the risk that a purchaser would murder the CQV for insurance proceeds would be great. In at least one case, an insurance company which sold a policy to a purchaser with no insurable interest (who later murdered the CQV for the proceeds), was found liable in court for contributing to the wrongful death of the victim (Liberty National Life v. Weldon, 267 Ala.171 (1957)).

Contract terms

Special exclusions may apply, such as suicide clauses, whereby the policy becomes null and void if the insured commits suicide within a specified time (usually two years after the purchase date; some states provide a statutory one-year suicide clause). Any misrepresentations by the insured on the application may also be grounds for nullification. Most US states specify a maximum contestability period, often no more than two years. Only if the insured dies within this period will the insurer have a legal right to contest the claim on the basis of misrepresentation and request additional information before deciding whether to pay or deny the claim.

The face amount of the policy is the initial amount that the policy will pay at the death of the insured or when the policy matures, although the actual death benefit can provide for greater or lesser than the face amount. The policy matures when the insured dies or reaches a specified age (such as 100 years old).

Costs, insurability and underwriting

The insurer (the life insurance company) calculates the policy prices with intent to fund claims to be paid and administrative costs, and to make a profit. The cost of insurance is determined using mortality tables calculated by actuaries. Actuaries are professionals who employ actuarial science, which is based on mathematics (primarily probability and statistics). Mortality tables are statistically based tables showing expected annual mortality rates. It is possible to derive life expectancy estimates from these mortality assumptions. Such estimates can be important in taxation regulation.[2][3]

The three main variables in a mortality table are commonly age, gender, and use of tobacco, but more recently in the US, preferred class-specific tables have been introduced. The mortality tables provide a baseline for the cost of insurance, but in practice these mortality tables are used in conjunction with the health and family history of the individual applying for a policy to determine premiums and insurability. Mortality tables currently in use by life insurance companies in the United States are individually modified by each company using pooled industry experience studies as a starting point. In the 1980s and 90s, the SOA 1975–80 Basic Select & Ultimate tables were the typical reference points, while the 2001 VBT and 2001 CSO tables were published more recently. The newer tables include separate mortality tables for smokers and non-smokers, and the CSO tables include separate tables for preferred classes.[4]

Recent US mortality tables predict that roughly 0.35 in 1,000 non-smoking males aged 25 will die during the first year of coverage after underwriting.[5] Mortality approximately doubles for every extra ten years of age, so the mortality rate in the first year for underwritten non-smoking men is about 2.5 in 1,000 people at age 65.[6] Compare this with the US population male mortality rates of 1.3 per 1,000 at age 25 and 19.3 at age 65 (without regard to health or smoking status).[7]

The mortality of underwritten persons rises much more quickly than the general population. At the end of 10 years the mortality of that 25 year-old, non-smoking male is 0.66/1000/year. Consequently, in a group of one thousand 25-year-old males with a $100,000 policy, all of average health, a life insurance company would have to collect approximately $50 a year from each participant to cover the relatively few expected claims. (0.35 to 0.66 expected deaths in each year x $100,000 payout per death = $35 per policy). Other costs, such as administrative and sales expenses, also need to be considered when setting the premiums. A 10 year policy for a 25-year-old non-smoking male with preferred medical history may get offers as low as $90 per year for a $100,000 policy in the competitive US life insurance market.

Most of the revenue received by insurance companies consists of premiums paid by policy holders, with some additional money being made through the investment of some of the cash raised from premiums. Rates charged for life insurance increase with the insurer's age because, statistically, people are more likely to die as they get older. The insurance company will investigate the health of and applicant for a policy to assess the likelihood of incurring a claim, in the same way that a bank would investigate an applicant for a loan to assess the likelihood of a default. Group Insurance policies are an exception to this. This investigation and resulting evaluation of the risk is termed underwriting. Health and lifestyle questions are asked, with certain responses or revelations possibly meriting further investigation. Life insurance companies in the United States support the Medical Information Bureau (MIB),[8] which is a clearing house of information on persons who have applied for life insurance with participating companies in the last seven years. As part of the application, the insurer often requires the applicant's permission to obtain information from their physicians.[9]

Underwriters will determine the purpose of insurance; the most common being to protect the owner's family or financial interests in the event of the insured's death. Other purposes include estate planning or, in the case of cash-value contracts, investment for retirement planning. Bank loans or buy-sell provisions of business agreements are another acceptable purpose.

Life insurance companies are never legally required underwrite or to provide coverage to anyone, with the exception of Civil Rights Act compliance requirements. Insurance companies alone determine insurability, and some people, for their own health or lifestyle reasons, are deemed uninsurable. The policy can be declined or rated (increasing the premium amount to compensate for a greater probability of a claim).[citation needed]

Many companies separate applicants into four general categories. These categories are preferred best, preferred, standard, and tobacco.[citation needed] Preferred best is reserved only for the healthiest individuals in the general population. This may mean, that the proposed insured has no adverse medical history, is not under medication for any condition, and his family (immediate and extended) have no history of early-onset cancer, diabetes, or other conditions.[10] Preferred means that the proposed insured is currently under medication for a medical condition and has a family history of particular illnesses.[citation needed] Most people are in the standard category.[citation needed] Profession, travel history, and lifestyle factor into whether the proposed insured will be granted a policy, and which category the insured falls. For example, a person who would otherwise be classified as preferred best may be denied a policy if he or she travels to a high risk country.[citation needed] Underwriting practices can vary from insurer to insurer, encouraging competition.

Death proceeds

Upon the insured's death, the insurer requires acceptable proof of death before it pays the claim. The normal minimum proof required is a death certificate, and the insurer's claim form completed, signed (and typically notarized).[citation needed] If the insured's death is suspicious and the policy amount is large, the insurer may investigate the circumstances surrounding the death before deciding whether it has an obligation to pay the claim.

Payment from the policy may be as a lump sum or as an annuity, which is paid in regular installments for either a specified period or for the beneficiary's lifetime.[citation needed]

Insurance vs assurance

The specific uses of the terms "insurance" and "assurance" are sometimes confused. In general, in jurisdictions where both terms are used, "insurance" refers to providing coverage for an event that might happen (fire, theft, flood, etc.), while "assurance" is the provision of coverage for an event that is certain to happen. In the United States both forms of coverage are called "insurance", for reasons of simplicity in companies selling both products.[citation needed]

Types

Life insurance may be divided into two basic classes: temporary and permanent; or the following subclasses: term, universal, whole life and endowment life insurance.

Term insurance

Term assurance provides life insurance coverage for a specified term. The policy does not accumulate cash value. Term is generally considered "pure" insurance, where the premium buys protection in the event of death and nothing else.

There are three key factors to be considered in term insurance:

- Face amount (protection or death benefit),

- Premium to be paid (cost to the insured), and

- Length of coverage (term).

Various insurance companies sell term insurance with many different combinations of these three parameters. The face amount can remain constant or decline. The term can be for one or more years. The premium can remain level or increase. Common types of term insurance include level, annual renewable and mortgage insurance.

Level term policy features a premium fixed for a period longer than a year. These terms are commonly 5, 10, 15, 20, 25, 30 and even 35 years. Level term is often used for long-term planning and asset management as premiums remain constant year to year, allowing for long-term budgeting. At the end of the term, some policies contain a renewal or conversion option. With guaranteed renewal, the insurance company guarantees it will issue a policy of an equal or lesser amount without regard to the insurability of the insured and with a premium set for the insured's age at that time. Some companies however do not guarantee renewal, and require proof of insurability at the time of renewal. Renewal that requires proof of insurability often includes a conversion option that allows the insured to convert the term policy to a permanent one, possibly compelling the applicant to agree to higher premiums. Renewal and conversion options can be very important when selecting a policy.

Annual renewable term is a one-year policy, but the insurance company guarantees it will issue a policy of an equal or lesser amount regardless of the insurability of the applicant, and with a premium set for the applicant's age at that time.

Another common type of term insurance is mortgage life insurance, which usually involves a level-premium, declining face value policy. The face amount is intended to equal the amount of the mortgage on the policy owner's property, such that any outstanding amount on the applicant's mortgage will be paid should the applicant die.

A policy holder insures his life for a specified term. If he dies before that specified term is up (with the exception of suicide), his estate or named beneficiary receives a payout. If he does not die before the term is up, he receives nothing. However, in some European countries (notably Serbia), insurance policy is such that the policy holder receives the amount he has insured himself to, or the amount he has paid to the insurance company in total. Suicide used to be excluded from all insurance policies[when?]. However, after a number of court judgements, many insurers began awarding payouts in the event of suicide (except for cases where it can be demonstrated that the insured committed suicide solely to access the policy payout). Generally, if an insured person commits suicide within the first two policy years, the insurer will simply return the premiums paid as a compromise. After this period, the full death benefit may be paid in the event of suicide.

Permanent life insurance

Permanent life insurance is life insurance that remains active until the policy matures, unless the owner fails to pay the premium when due. The policy cannot be cancelled by the insurer for any reason except fraudulent application, and any such cancellation must occur within a period of time defined by law (usually two years). A permanent insurance policy accumulates a cash value, reducing the risk to which the insurance company is exposed, and thus the insurance expense over time. This means that a policy with a million dollar face value can be relatively expensive to a 70-year-old. The owner can access the money in the cash value by withdrawing money, borrowing the cash value, or surrendering the policy and receiving the surrender value.

The four basic types of permanent insurance are whole life, universal life, limited pay and endowment.

Whole life coverage

Whole life insurance provides lifetime death benefit coverage for a level premium in most cases. Premiums are much higher than term insurance at younger ages, but as term insurance premiums rise with age at each renewal, the cumulative value of all premiums paid across a life time are roughly equal if policies are maintained until average life expectancy. Part of the insurance contract stipulates that the policyholder is entitled to a cash value reserve, which is part of the policy and guaranteed by the company. This cash value can be accessed at any time through policy loans and are received income tax free. Policy loans are available until the insured's. If there are any unpaid loans upon death, the insurer subtracts the loan amount from the death benefit and pays the remainder to the beneficiary named in the policy.

While the marketing divisions of some life insurance companies often explain whole life as a "death benefit with a savings component", this distinction is artificial according to life insurance actuaries Albert E. Easton and Timothy F. Harris.[11] The cash value reserve builds up against the death benefit of the policy and reduces the net amount at risk. The net amount at risk is the amount the insurer must pay to the beneficiary should the insured die before the policy has accumulated an amount equal to the death benefit. It is the difference between the current cash value amount and the total death benefit amount. Because of this relationship between the cash value and death benefit, it may be more accurate to describe the policy as a single, indivisible product, as no actual separation of the cash value and death benefit is possible. The insurer is actually setting aside money as a cash reserve to pay the future death benefit claim. This suggests that the cash value is technically part of the death benefit, which is "earned" as cash over time. The lack of separation between the cash value and death benefit also explains why insurers do not pay both the death benefit and the cash value to the beneficiary.

The advantages of whole life insurance are guaranteed death benefits, guaranteed cash values, fixed, predictable annual premiums and mortality and expense charges that will not reduce the cash value of the policy. The disadvantages of whole life are inflexibility of premiums and the fact that the internal rate of return in the policy may not be competitive with other savings alternatives. Riders are available that can allow one to increase the death benefit by paying additional premium. One such rider is a paid-up additions rider.

The death benefit can also be increased through the use of policy dividends, though these dividends cannot be guaranteed and may be higher or lower than historical rates over time. According to internal documents from some life insurance companies, like Massachusetts Mutual, the internal rate of return and dividend payment realized by the policyholder is often a function of when the policyholder buys the policy and how long that policy remains in force. Dividends paid on a whole life policy can be utilized in many ways. First, if "paid-up additions" is elected, dividends will purchase additional death benefit which will increase the death benefit of the policy to the named beneficiary. Since this additional death benefit generates cash value, it also increases the cash value of the policy. Another alternative is to opt in for 'reduced premiums' on some policies. This reduces the owed premiums by the non-guaranteed dividends amount. A third option allows the owner to take the dividends as they are paid out (although some policies provide other/different/less options than these - it depends on the company for some cases). A final option is to invest the dividends in the insurance company's general or separate account.

Universal life coverage

Universal life insurance (UL) is a relatively new insurance product, intended to combine permanent insurance coverage with greater flexibility in premium payment, along with the potential for greater growth of cash values. There are several types of universal life insurance policies which include interest sensitive (also known as "traditional fixed universal life insurance"), variable universal life (VUL), guaranteed death benefit, and equity indexed universal life insurance.

A universal life insurance policy includes a cash value. Premiums increase the cash values, but the cost of insurance (along with any other charges assessed by the insurance company) reduces cash values. However, with the exception of VUL, interest is paid at a rate specified by the company, further increasing cash values. With VUL, cash values will ebb and flow relative to the performance of the investment sub-accounts the policy owner has chosen. The surrender value of the policy is the amount payable to the policy owner after applicable surrender charges, if any.

Universal life insurance addresses the perceived disadvantages of whole life – namely that premiums and death benefit are fixed. With universal life, both the premiums and death benefit are flexible. Except with regards to guaranteed death benefit universal life, this flexibility comes the disadvantage of reduced guarantees.

Depending on how interest is credited, the internal rate of return can be higher as it moves with prevailing interest rates (interest-sensitive) or the financial markets (equity indexed universal life and variable universal life). Mortality costs and administrative charges are known, and cash value may be considered more easily attainable because the owner can discontinue premiums if the cash value allows this.

Flexible death benefit means the policy owner can choose to decrease the death benefit. The death benefit could also be increased by the policy owner, but that would typically require the insured to go through a new underwriting. Another feature of flexible death benefit is the ability to choose from option A or option B death benefits, and to change those options during the life of the insured. Option A is often referred to as a level death benefit. Generally speaking, the death benefit will remain level for the life of the insured and premiums are expected to be lower than policies with an Option B death benefit. Option B pays the face amount plus the cash value. If cash values grow over time, so would the death benefit which is payable to the insured's beneficiaries. If cash values decline, the death benefit would also decline. Presumably, option B death benefit policies would require higher premiums than option A policies.

Limited-pay

Another type of permanent insurance is Limited-pay life insurance, in which all the premiums are paid over a specified period after which no additional premiums are due to keep the policy in force. Common limited pay periods include 10-year, 20-year, and are paid out at the age of 65.

Endowments

Main article: Endowment policyEndowments are policies in which the cumulative cash value of the policy equals the death benefit at a certain age. The age at which this condition is reached is known as the endowment age. Endowments are considerably more expensive (in terms of annual premiums) than either whole life or universal life because the premium paying period is shortened and the endowment date is earlier.

In the United States, the Technical Corrections Act of 1988 tightened the rules on tax shelters (creating modified endowments). These follow tax rules in the same manner as annuities and IRAs.

Endowment insurance is paid out whether the insured lives or dies, after a specific period (e.g. 15 years) or a specific age (e.g. 65).

Accidental death

Accidental death is a limited life insurance designed to cover the insured should they pass away due to an accident. Accidents include anything from an injury and upwards, but do not typically cover deaths resulting from health problems or suicide. Because they only cover accidents, these policies are much less expensive than other life insurance policies.

It is also very commonly offered as accidental death and dismemberment insurance (AD&D) policy. In an AD&D policy, benefits are available not only for accidental death, but also for the loss of limbs or bodily functions, such as sight and hearing.

Accidental death and AD&D policies very rarely pay a benefit, either because the cause of death is not covered by the policy, or the coverage is not maintained after the accident until death occurs. To be aware of what coverage they have, an insured should always review their policy for what it covers and what it excludes. Often, it does not cover an insured who puts themselves at risk in activities such as parachuting, flying, professional sports or involvement in a war (military or not). Also, some insurers will exclude death and injury due to (but not limited to) motor racing and mountaineering.

Accidental death benefits can also be added to a standard life insurance policy as a rider. If this rider is purchased, the policy will generally pay double the face amount if the insured dies due to an accident. This used to be commonly referred to as a double indemnity policy. In some cases, insurers may even offer triple indemnity cover.

Related products

Riders are modifications to the insurance policy added at the same time the policy is issued. These riders change the basic policy to provide some feature desired by the policy owner. A common rider is accidental death (see above). Another common rider is a premium waiver, which waives future premiums if the insured becomes disabled.

Joint life insurance is either a term or permanent policy insuring two or more persons with the proceeds payable on either the first or second death.

Survivorship life is a whole life policy insuring two lives with the proceeds payable on the second (later) death.

Single premium whole life is a policy with only one premium which is payable at the time the policy matures.

Modified whole life is a whole life policy featuring smaller premiums for a specified period of time, after which the premiums increase for the remainder of the policy.

Group life insurance is term insurance covering a group of people, usually employees of a company or members of a union or association. Individual proof of insurability is not normally a consideration in the underwriting. Rather, the underwriter considers the size, turnover and financial strength of the group. Contract provisions will attempt to exclude the possibility of adverse selection. Group life insurance often includes a provision for a member exiting the group to buy individual coverage.

Senior and preneed products

Insurance companies have in recent years developed products to offer to niche markets, most notably targeting the senior market to address needs of an ageing population. Many companies offer policies tailored to the needs of senior applicants. These are often low to moderate face value whole life insurance policies, to allow a senior citizen purchasing insurance at an older issue age an opportunity to buy affordable insurance. This may also be marketed as final expense insurance, and an agent or company may suggest that the policy proceeds could be used for end-of-life expenses.

Preneed (or prepaid) insurance policies are whole life policies that, although available at any age, are usually offered to older applicants. This type of insurance is designed specifically to cover funeral expenses when the insured person dies. In many cases, the applicant signs a pre-funded funeral arrangement with a funeral home at the time the policy is applied for. The death proceeds are then guaranteed to be directed to the funeral services provider for payment of services rendered. Most contracts dictate that any excess proceeds will go either to the insured's estate or a designated beneficiary.

Investment policies

With-profits policies

Main article: With-profits policySome policies afford the policyholder a share of the profits of the insurance company – these are termed with-profits policies. Other policies provide no rights to a share of the profits of the company, these are non-profit policies.

With-profits policies are used as a form of collective investment to achieve capital growth. Other policies offer a guaranteed return not dependent on the company's underlying investment performance; these are often referred to as without-profit policies, which may be construed as a misnomer.

Investment bonds

Main article: Insurance bondPensions

Pensions are a form of life assurance. However, whilst basic life assurance, permanent health insurance and non-pensions annuity business all include an amount of mortality or morbidity risk for the insurer, pensions pose a longevity risk.

A pension fund will be built up throughout a person's working life. When the person retires, the pension will become in payment, and at some stage the pensioner will buy an annuity contract, which will guarantee a certain pay-out each month until death.

Annuities

Main article: Life annuityAn annuity is a contract with an insurance company whereby the insured pays an initial premium or premiums into a tax-deferred account, which pays out a sum at pre-determined intervals. There are two periods: the accumulation (when payments are paid into the account) and the annuitization (when the insurance company pays out). IRS rules restrict how money can be withdrawn from an annuity. Distributions may be taxable and/or penalized.

Taxation

United States

Premiums paid by the policy owner are normally not deductible for federal and state income tax purposes, and proceeds paid by the insurer upon the death of the insured are not included in gross income for federal and state income tax purposes.[12] However, if the proceeds are included in the "estate" of the deceased, it is likely they will be subject to federal and state estate and inheritance tax.

Cash value increases within the policy are not subject to income taxes unless certain events occur. For this reason, insurance policies can be a legal and legitimate tax shelter wherein savings can increase without taxation until the owner withdraws the money from the policy. In flexible-premium policies, large deposits of premium could cause the contract to be considered a modified endowment contract by the Internal Revenue Service (IRS), which negates many of the tax advantages associated with life insurance. The insurance company, in most cases, will inform the policy owner of this danger before deciding their premium.

The tax ramifications of life insurance are complex. The policy owner would be well advised to carefully consider them. As always, both the United States Congress and state legislatures can change the tax laws at any time.

United Kingdom

Premiums are not usually deductible against income tax or corporation tax, however qualifying policies issued prior to 14 March 1984 do still attract LAPR (Life Assurance Premium Relief) at 15% (with the net premium being collected from the policyholder).

Non-investment life policies do not normally attract either income tax or capital gains tax on claim. If the policy has as investment element such as an endowment policy, whole of life policy or an investment bond then the tax treatment is determined by the qualifying status of the policy.

Qualifying status is determined at the outset of the policy if the contract meets certain criteria. Essentially, long term contracts (10 years plus) tend to be qualifying policies and the proceeds are free from income tax and capital gains tax. Single premium contracts and those running for a short term are subject to income tax depending upon the marginal rate in the year a gain is made. All UK insurers pay a special rate of corporation tax on the profits from their life book; this is deemed as meeting the lower rate (20% in 2005–06) of liability for policyholders. Therefore a policyholder who is a higher rate taxpayer (40% in 2005-06), or becomes one through the transaction, must pay tax on the gain at the difference between the higher and the lower rate. This gain is reduced by applying a calculation called top-slicing based on the number of years the policy has been held. Although this is complicated, the taxation of life assurance-based investment contracts may be beneficial compared to alternative equity-based collective investment schemes (unit trusts, investment trusts and OEICs). One feature which especially favors investment bonds is the '5% cumulative allowance' – the ability to draw 5% of the original investment amount each policy year without being subject to any taxation on the amount withdrawn. If not used in one year, the 5% allowance can roll over into future years, subject to a maximum tax-deferred withdrawal of 100% of the premiums payable. The withdrawal is deemed by the HMRC (Her Majesty's Revenue and Customs) to be a payment of capital and therefore the tax liability is deferred until maturity or surrender of the policy. This is an especially useful tax planning tool for higher rate taxpayers who expect to become basic rate taxpayers at some predictable point in the future (e.g. retirement), as at this point the deferred tax liability will not result in tax being due.

The proceeds of a life policy will be included in the estate for death duty (in the UK, inheritance tax) purposes. Policies written in trust may fall outside the estate. Trust law and taxation of trusts can be complicated, so any individual intending to use trusts for tax planning would usually seek professional advice from an Independent Financial Adviser and/or a solicitor.

Pension term assurance

Although available before April 2006, from this date pension term assurance became widely available in the UK. Most UK insurers adopted the name "life insurance with tax relief" for the product. Pension term assurance is effectively normal term life assurance with tax relief on the premiums. All premiums are paid at a net of basic rate tax at 22%, and higher rate tax payers can gain an extra 18% tax relief via their tax return. Although not suitable for all, PTA briefly became one of the most common forms of life assurance sold in the UK until, Chancellor Gordon Brown announced the withdrawal of the scheme in his pre-budget announcement on 6 December 2006.

History

Main article: History of insuranceInsurance began as a way of reducing the risk to traders, as early as 2000 BC in China and 1750 BC in Babylon. Life insurance dates to ancient Rome; "burial clubs" covered the cost of members' funeral expenses and assisted survivors financially. Modern life insurance originated in 17th century England, originally as insurance for traders.[13] Merchants, ship owners and underwriters met to discuss deals at Lloyd's Coffee House, predecessor to the famous Lloyd's of London. The first society to sell life insurance was the Amicable Society for a Perpetual Assurance Office.

The first insurance company in the United States was formed in Charleston, South Carolina in 1732, but it provided only fire insurance. The sale of life insurance in the U.S. began in the late 1760s. The Presbyterian Synods in Philadelphia and New York created the Corporation for Relief of Poor and Distressed Widows and Children of Presbyterian Ministers in 1759; Episcopalian priests organized a similar fund in 1769. Between 1787 and 1837 more than two dozen life insurance companies were started, but fewer than half a dozen survived.

Prior to the American Civil War, many insurance companies in the United States insured the lives of slaves for their owners. In response to bills passed in California in 2001 and in Illinois in 2003, the companies have been required to search their records for such policies. New York Life, for example, reported that Nautilus sold 485 slaveholder life insurance policies during a two-year period in the 1840s; they added that their trustees voted to end the sale of such policies 15 years before the Emancipation Proclamation.

Market trends

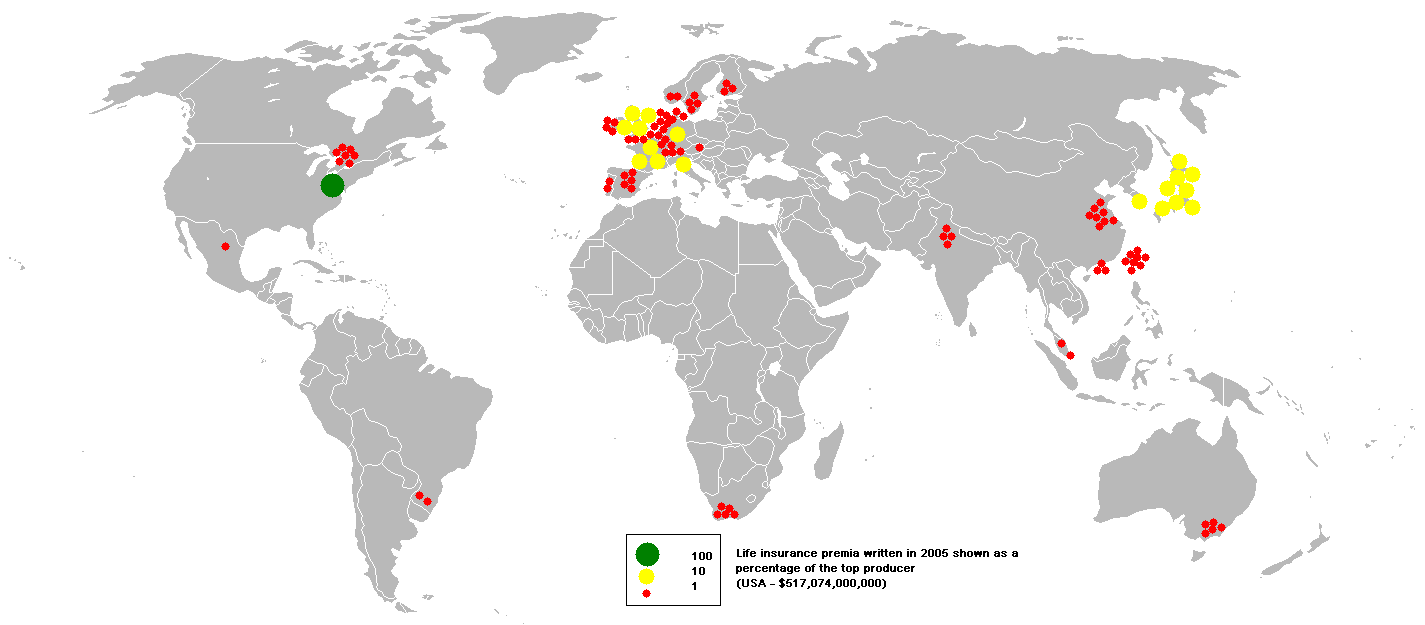

Life insurance premiums written in 2005

Life insurance premiums written in 2005

According to a study by Swiss Re, the EU was the largest market for life insurance premiums in 2005, followed by the USA and Japan.

Stranger originated

Stranger originated life insurance or STOLI is a life insurance policy that is held or financed by a person who has no relationship to the insured person. Generally, the purpose of life insurance is to provide peace of mind by assuring that financial loss or hardship will be alleviated in the event of the insured person's death. STOLI has often been used as an investment technique whereby investors will encourage someone (usually an elderly person) to purchase life insurance and name the investors as the beneficiary of the policy. This undermines the primary purpose of life insurance, as the investors would incur no financial loss should the insured person die. In some jurisdictions, there are laws to discourage or prevent STOLI.

Criticism

Although some aspects of the application process (such as underwriting and insurable interest provisions) make it difficult, life insurance policies have been used to facilitate exploitation and fraud. In the case of life insurance, there is a possible motive to purchase a life insurance policy, particularly if the face value is substantial, and then murder the insured. Usually, the larger the claim, and the more serious the incident, the larger and more intense the ensuing investigation, consisting of police and insurer investigators.[14]

The television series Forensic Files has included episodes that feature this scenario. There was also a documented case in 2006, where two elderly women were accused of taking in homeless men and assisting them. As part of their assistance, they took out life insurance for the men. After the contestability period ended on the policies, the women are alleged to have had the men killed via hit-and-run car crashes.[15]

Recently, viatical settlements have created problems for life insurance providers. A viatical settlement involves the purchase of a life insurance policy from an elderly or terminally ill policy holder. The policy holder sells the policy (including the right to name the beneficiary) to a purchaser for a price discounted from the policy value. The seller has cash in hand, and the purchaser will realize a profit when the seller dies and the proceeds are delivered to the purchaser. In the meantime, the purchaser continues to pay the premiums. Although both parties have reached an agreeable settlement, insurers are troubled by this trend. Insurers calculate their rates with the assumption that a certain portion of policy holders will seek to redeem the cash value of their insurance policies before death. They also expect that a certain portion will stop paying premiums and forfeit their policies. However, viatical settlements ensure that such policies will with absolute certainty be paid out. Some purchasers, in order to take advantage of the potentially large profits, have even actively sought to collude with uninsured elderly and terminally ill patients, and created policies that would have not otherwise been purchased. These policies are guaranteed losses from the insurers' perspective.

See also

References

Specific references

- ^ Oviatt, p. 181

- ^ IRS Retirement Plans FAQs regarding Revenue Ruling 2002-62

- ^ IRS Bulletin No. 2002–42

- ^ "AAA/SOA Review of the Interim Mortality Tables Developed by Tillinghast and Proposed for Use by the ACLI from the Joint American Academy of Actuaries/Society of Actuaries Review Team" August 29, 2006

- ^ Actuary.org

- ^ Actuary.org

- ^ Arias, Elizabeth (2004-02-18). "United States Life Tables, 2001". National Vital Statistics Report 52 (14). http://www.cdc.gov/nchs/data/nvsr/nvsr52/nvsr52_14.pdf. Retrieved 3 November 2011.

- ^ Medical Information Bureau (MIB) website

- ^ MIB Consumer FAQs

- ^ "How do Insurance Rating Classifications Work?". http://www.lifeinsure.com/lifeinsurance/Insurance-Rating-Classifications.asp. Retrieved 4 November 2011.

- ^ Easton, A.E., Harris, T.F. (1999). "Actuarial Aspects Of Individual Life Insurance And Annuity Contracts". Winsted, Connecticut: Actex Publications, Inc.

- ^ Internal Revenue Code § 101(a)(1)

- ^ "And whereas I have left in the hands of Doctor Ducke Channcellor of London two pollicies of insurance the one of one hundred pounds for the safe arivall of our Shipp in Guiana which is in mine owne name, if we miscarry by the waie (which God forbid) I bequeath the advantage thereof to my said Cosin Thomas Muchell...whereas there is an other insurance of one hundred pounds assured by the said Doctor Arthur Ducke on my life for one yeare if I chance to die within that tyme I entreat the said doctor Ducke to make it over to the said Thomas Muchell his kinsman..." Will of Robert Hayman, 1628 (proved 1632):Records of the Prerogative Court of Canterbury, Catalogue Reference PROB 11/163

- ^ Coalition Against Insurance Fraud – Impact Statement

- ^ "Two Elderly Women Indicted on Fraud Charges in Deaths of LA Hit-Run". Insurance Journal. June 1, 2006. http://www.insurancejournal.com/news/west/2006/06/01/69022.htm.

- Sources

- Oviatt, F. C. "Economic place of insurance and its relation to society" in American Academy of Political and Social Science; National American Woman Suffrage Association Collection (Library of Congress) (1905). Annals of the American Academy of Political and Social Science. XXVI. Published by A.L. Hummel for the American Academy of Political and Social Science. pp. 181–191. http://books.google.com/books?id=moMQAAAAYAAJ&pg=RA1-PA1. Retrieved 8 June 2011.

External links

- Learn About Life Insurance - Insurance Information Institute Life Insurance Learning Center

- A History of Life Insurance in the United States through World War I

- Life Insurance Needs Calculator and Information - The Life and Health Insurance Foundation For Education is a nonprofit organization dedicated to helping consumers make smart insurance decisions to safeguard their families’ financial futures.

Insurance Types of insurance LifeBusinessBond insurance · Directors and officers liability insurance · Errors and omissions insurance · Fidelity bond · Professional indemnity insurance · Professional liability insurance · Protection and indemnity insurance · Trade credit insuranceResidentialTransport/

CommunicationOtherHistory of insurance · Casualty insurance · Crime insurance · Crop insurance · Group insurance · Liability insurance · No-fault insurance · Pet insurance · Reinsurance · Terrorism insurance · Wage insurance · Weather insurance · Workers' compensationInsurance policy and law Categories:

Wikimedia Foundation. 2010.