- Superannuation in Australia

-

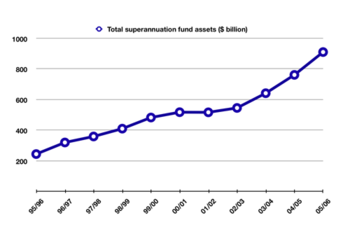

Total superannuation industry assets at the end of the financial year 1996-2006.

Total superannuation industry assets at the end of the financial year 1996-2006.

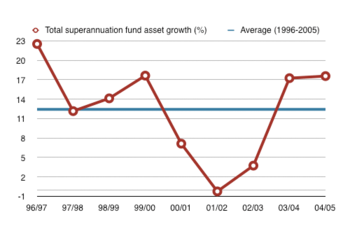

Annual total superannuation industry asset growth 1996-2005.

Annual total superannuation industry asset growth 1996-2005.Superannuation is a retirement (including pensions) program in Australia. It has a compulsory element whereby employers are required by law to pay an additional amount based on a proportion of an employee's salaries and wages (currently 9%) into a complying superannuation fund.

An individual's superannuation fund can be accessed when the employee meets one of the conditions of release contained in Schedule 1 of the Superannuation Industry (Supervision) Regulations 1994.[1]

Contents

Introduction

Prior to the introduction of the "Superannuation Guarantee" in 1992 by the Keating Labor government, reasonably widespread superannuation arrangements had been in place for many years under industrial awards negotiated by the union movement between wage increases.

The compulsory "Superannuation Guarantee" system was introduced as part of a major reform package addressing Australia's retirement income policies. It was anticipated that Australia, along with many other Western nations, would experience a major demographic shift in the coming decades, resulting in the anticipated increase in age pension payments placing an unaffordable strain on the Australian economy. The proposed solution was a "three pillars" approach to retirement income:

- A safety net consisting of a means-tested Government age pension system

- Private savings generated through compulsory contributions to superannuation

- Voluntary savings through superannuation and other investments

The change came about through a tripartite agreement between the government, employers and the trade unions. The trade unions agreed to forego a national 3% pay increase which would be put into the new superannuation system for all employees in Australia. This was matched by employers contributions which were set to increase over time to a proposed 12%. Subsequent changes meant this has been capped at the lower employer rate of 9%.

Since its introduction, employers have been required to make compulsory contributions to superannuation on behalf of most of their employees. This contribution was originally set at 3% of the employees' income, and has been gradually increased by the Australian government. Since 1 July 2002, the minimum contribution has been set at 9% of an employee's ordinary time earnings. The 9% is thus not payable on overtime rates but is payable on remuneration items such as bonuses, commissions, shift loading and casual loadings.

Though there is general widespread support for compulsory superannuation today, it was met with strong resistance by small business groups at the time of its introduction who were fearful of the burden associated with its implementation and its ongoing costs.[2]

The Howard government was criticised by former Prime Minister Paul Keating for its reluctance to increase the compulsory rate of superannuation. Keating argued that had the compulsory rate been 15% since 1996, rather than the current 9%, total superannuation assets in Australia would be approaching $2 trillion - almost double the current level.[3]

After more than a decade of compulsory contributions, Australian workers have over $1.28 trillion[4] in superannuation assets. Australians now have more money invested in managed funds per capita than any other economy.[5]

Compulsory superannuation in combination with buoyant economic growth has turned Australia into a 'shareholder society', where most workers are now indirect investors in the stock market. Consequently, a lively personal investment marketplace has developed, and many Australians take an interest in investment topics.

Operation

Employer contributions

Employers must make superannuation contributions to the employees' at 9% to a designated superannuation fund at least every three months. The superannuation contributions are invested over the period of the employees' working life and the sum of compulsory and voluntary contributions, plus earnings, less taxes and fees is paid to the person when they choose to retire. The sum most people receive is predominantly made up of compulsory employer contributions.

Special rules apply in relation to employers providing defined benefit arrangements. There are less common traditional employer funds where benefits are determined by a formula usually based on final average salary and length of service. Essentially, instead of minimum contributions, employers need to provide a minimum level of benefit.

Superannuation Guarantee law applies to all working Australians, except those earning less than $450 per month, or aged under 18 or over 70. Individuals can choose to make extra voluntary contributions to their superannuation and receive tax benefits for doing so.

Access to superannuation

As superannuation is money invested for one's retirement, strict government rules prevent early access to preserved benefits except in very limited and restricted circumstances, including severe financial hardship or on compassionate grounds, such as for medical treatment not available through Medicare.

Generally, superannuation benefits fall into three (3) categories:

- Preserved benefits;

- Restricted non-preserved benefits; and

- Unrestricted non-preserved benefits.

Preserved benefits are benefits that must be retained in a superannuation fund until the employee's 'preservation age'. Currently, all workers must wait until they are 55 before they may access these funds. All contributions made after 1 July 1999 fall into this category.

Restricted non-preserved benefits although not preserved, cannot be accessed until an employee meets a condition of release, such as terminating their employment in an employer superannuation scheme.

Unrestricted non-preserved benefits do not require the fulfilment of a condition of release, and may be accessed upon the request of the worker. For example, where a worker has previously satisfied a condition of release and decided not to access the money in their superannuation fund.

Preservation age

Date of birth Preservation age Before 1 July 1960 55 1 July 1960 – 30 June 1961 56 1 July 1961 – 30 June 1962 57 1 July 1962 – 30 June 1963 58 1 July 1963 – 30 June 1964 59 After 30 June 1964 60 Eligibility for access to preserved benefits depends on a worker's preservation age. The Howard government announced changes in 1997 to the superannuation system designed to induce Australians to stay in the workforce for a longer period of time, delaying the effect of population ageing. Previously, any Australian could access their preserved benefits once they reached 55 years of age. However, after legislation was passed in 1999, an employee's preservation age depends on their date of birth.

Hence, by 2025, all Australian workers wishing to access their superannuation would be at least 60 years old.

Reasonable benefit limits

Reasonable benefit limits (RBL) were the maximum amount of retirement and termination of employment benefits that a person could receive over their lifetime at concessional tax rates. RBLs were abolished from 1 July 2007.[6]

There were two types of RBLs - a lump sum RBL and a higher pension RBL. The lump sum RBL applied to most people. Generally, the higher pension RBL applied to people who took 50% or more of their benefits in the form of pensions or annuities that met certain conditions (for example, restrictions on the ability to convert the pension back into a lump sum).[7]

Each year, RBLs were indexed according to movement in Average Weekly Ordinary Time Earnings published by the Australian Bureau of Statistics. For the financial year ending 30 June 2005, the lump sum RBL was $619,223 and the pension RBL was $1,238,440.[7]

Superannuation taxes

Main article: Taxation of Superannuation in AustraliaMost superannuation is concessionally taxed at a flat rate of 15% at two main points: on contributions, and on earnings. Contributions either in the form of employer superannuation payments, or member salary sacrifice, are taxed at this rate.

In most industry funds, the earnings tax is paid before profits are disbursed to members so it appears as a lower level of interest on the member's statement. Members can also contribute funds into their super after income tax has been paid on it; in this case they are not liable for 15% contributions tax and may be eligible to receive a matching contribution from the government depending on income.

These taxes contribute over $6 billion in annual government revenue.[8] Superannuation is a tax-advantaged method of saving as the 15% tax rate on contributions is lower than the rate an employee would have paid if they received the money as income. The Federal government announced in its 2006/07 budget that from 1 July 2007, Australians over the age of 60 will face no taxes on withdrawing monies out of their superannuation fund if it is from a taxed source.

In 1996, the federal government imposed an extra 'superannuation surcharge' on higher income earners as a temporary levy to raise revenue. As part of the 2001 election campaign, the government promised to reduce the surcharge from 15% to 10.5% over three years. The superannuation surcharge was eventually scrapped in the 2005/06 budget, and has been abolished since 1 July 2005.

From 1 January 2006, the government has allowed the splitting of contributions with a spouse.[9] This allows a couple, who are members of superannuation funds, to split their contributions — personal and employer — evenly. They can thus reduce the risk of exceeding their reasonable benefit limits and therefore reduce their chances of paying a higher rate of tax on their retirement savings. Since the reasonable benefits limit have been removed - 2007 legislation - it is no longer necessary to split contributions expressly for this reason.

Superannuation co-contribution scheme

Since 1 July 2003, the Government has made available incentives of a Government co-contribution of up to $1,500 for lower income employees who make personal contributions to their own superannuation fund. Depending on individual income thresholds, the Government pays up to $1.50 for every $1 contributed. The amount has since been lowered and is now a matching contribution up to $1,000 (until 2012), but will be increased in two stages to the same level as before by the 2014/15 financial year.

The 2007 Federal Budget announced a one-off double payment of the co-contributions paid due to personal contributions in the 2005/2006 financial year. Lower income earners received up to $3000 co-contribution for $1000 of personal contributions in that year.

Superannuation funds

Trustee structure

Superannuation funds operate as trusts with trustees being responsible for the prudential operation of their funds and in formulating and implementing an investment strategy. Some specific duties and obligations are codified in the Superannuation Industry (Supervision) Act 1993 - other obligations are the subject of general trust law. Trustees are liable under law for breaches of obligations. Superannuation trustees have, inter alia, an obligation to ensure that superannuation monies are invested prudently with consideration given to diversification and liquidity.

Investments

Other than a few very specific provisions in the Superannation Industry (Supervision) Act 1993 (largely related to investments in assets related to the employer) funds are not subject to any asset requirements or investment exposure floors. There are no minimum rate of return requirements, nor a government guarantee of benefits. There are some minor restrictions on borrowing and the use of derivatives and investments in the shares and property of employer sponsors of funds.

As a result, superannuation funds tend to invest in a wide variety of assets with a mix of duration and risk/return characteristics. The recent investment performance of superannuation funds compares favourably with alternative assets such as ten year bonds.

Types of superannuation funds

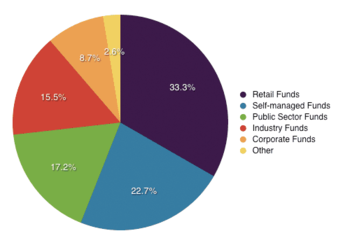

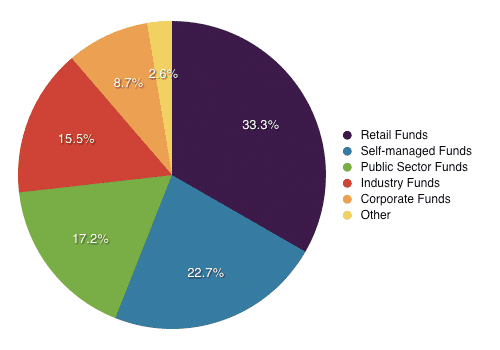

Share of superannuation industry fund assets.

Share of superannuation industry fund assets.There are about 500,000 superannuation funds in operation in Australia. Of those, 362 have assets totalling greater than $50 million.

There are seven main types of superannuation funds:

- Industry Funds are multiemployer funds run by employer associations and/or unions. Unlike Retail/Wholesale funds they are run solely for the benefit of members as there are no shareholders.

- Wholesale Master Trusts are multiemployer funds run by financial institutions for groups of employees. These are also classified as Retail funds by APRA.

- Retail Master Trusts/Wrap platforms are funds run by financial institutions for individuals.

- Employer Stand-alone Funds are funds established by employers for their employees. Each fund has its own trust structure that is not necessarily not shared by other employers.

- Self Managed Superannuation Funds (SMSFs or Do-It-Yourself Funds) are funds established for a small number of individuals (fewer than 5) and regulated by the Australian Taxation Office. Generally the Trustees of the fund are the fund members (where there is a Corporate Trustee, the members are the directors of that company). This is now the largest segment of the superannuation industry by value.

- Small APRA Funds (SAFs) are funds established for a small number of individuals (fewer than 5) but unlike SMSFs the Trustee is an Approved Trustee, not the member/s, and the funds are regulated by APRA. This structure is often used for members who want control of their superannuation investments but are unable or unwilling to meet the requirements of Trusteeship of an SMSF.

- Public Sector Employees Funds are funds established by governments for their employees.

Retail and Wholesale Master Trusts are the largest sector of the Australian Superannuation Market

Choice of superannuation funds

From 1 July 2005, changes to the law mean that many Australian employees are able to choose the fund their employer's future superannuation guarantee contributions are paid into. Choice of superannuation funds allows workers to:

- change funds when their current fund is not available with a new employer;

- consolidate superannuation accounts to cut costs and paperwork;

- change to a lower-fee and/or better service superannuation fund;

- change to a better performing superannuation fund.

Regulation

Legislation

Superannuation funds are principally regulated under the Superannuation Industry (Supervision) Act 1993 and the Financial Services Reform Act 2002. Compulsory employer contributions are regulated via the Superannuation Guarantee (Administration) Act 1992

Superannuation Industry (Supervision) Act 1993 (SIS)

The Superannuation Industry (Supervision) Act sets all the rules that a complying superannuation fund must obey (adherence to these rules is called compliance). The rules cover general areas relating to the trustee, investments, management, fund accounts and administration, enquiries and complaints.

SIS also:

- regulates the operation of superannuation funds; and

- sets penalties for trustees when the rules of operation are not met.

In June 2004 the SIS Act and Regulations were amended to require all superannuation trustees to apply to become a Registrable Superannuation Entity Licensee (RSE Licensee) in addition each of the superannuation funds the trustee operates is also required to be registered. The transition period is intended to end 30 June 2006. The new licensing regime requires trustees of superannuation funds to demonstrate to APRA that they have adequate resources (human, technology and financial), risk management systems and appropriate skills and expertise to manage the superannuation fund. The licensing regime has lifted the bar for superannuation trustees with a significant number of small to medium size superannuation funds exiting the industry due to the increasing risk and compliance demands.

The Financial Services Reform Act 2002 (FSR)

The Financial Services Reform Act covers a very broad area of finance and is designed to provide standardisation within the financial services industry. Under the FSR, to operate a superannuation fund, the trustee must have a licence to run a fund and the individuals within the funds require a licence to perform their job.

With regard to superannuation, FSR:

- provides licensing of 'dealers' (providers of financial products and services);

- oversees the training of agents representing dealers;

- sets out the requirements regarding what information must be provided on any financial product to members and prospective members; and

- sets out the requirements that determine good-conduct and misconduct rules for superannuation funds.

Regulatory bodies

Four main regulatory bodies keep watch over superannuation funds to ensure they comply with the legislation:

- The Australian Prudential Regulation Authority (APRA) is responsible for ensuring that superannuation funds behave in a prudent manner. APRA also reviews a fund's annual accounts to assess their compliance with the SIS.

- The Australian Securities and Investments Commission (ASIC) ensures that trustees of superannuation funds comply with their obligations regarding the provision of information to fund members during their membership. ASIC is also responsible for consumer protection in the financial services area (including superannuation). It also monitors funds' compliance with the FSR.

- The Australian Taxation Office (ATO) ensures that self-managed superannuation funds adhere to the rules and regulations. It also makes sure that the right amount of tax is taken from the superannuation savings of all Australians.

- The Superannuation Complaints Tribunal (SCT) administers the Superannuation (Resolution of Complaints) Act. This Act provides the formal process for the resolution of complaints. The SCT will try to resolve any complaints between a member and the superannuation fund by negotiation or conciliation. The SCT only deals with complaints when no satisfactory resolution has been reached.

Similar schemes in other countries

- Registered Retirement Savings Plan (RRSP) (Canada)

- Individual Retirement Account (IRA) and 401K (USA)

See also

International:

- Pension systems around the world

Notes

- ^ Superannuation Industry (Supervision) Regulations 1994 - Schedule 1, Commonwealth Consolidated Regulations, www.austlii.edu.au, accessed 3 October 2011.

- ^ Patrick Collinson (2004) Australia may hold key to pensions, The Guardian, 12 October 2004, retrieved 21 July 2006.

- ^ Lateline - Tony Jones speaks to former prime minister, Paul Keating, broadcast 13 September 2006, Australian Broadcasting Corporation, retrieved 6 October 2006.

- ^ Quarterly Superannuation Performance September 2010, retrieved 28 January 2011[dead link]

- ^ Australia 'tops' in managed funds, 23 January 2006, Sydney Morning Herald, retrieved 23 January 2006.

- ^ RBLs were abolished from 1 July 2007, however there were still RBL obligations for superannuation benefits paid up to 30 June 2007.

Superannuation and reasonable benefit limits, Australian Taxation Office, 4 August 2011, accessed 3 October 2011. - ^ a b What are RBLs?, Australian Taxation Office, 5 June 2007, accessed 3 October 2011

- ^ 2006/07 Estimates of Revenue, 2006-07 Budget, Australian Government, 2006, retrieved 21 July 2006

- ^ "Split that can benefit you and your spouse". The Sydney Morning Herald. 1 January 2006. http://www.smh.com.au/news/superannuation/split-that-can-benefit-you-and-your-spouse/2006/01/02/1136050380691.html. Retrieved 24 January 2006.

External links

- ASIC's consumer and investor website MoneySmart - Superannuation and Retirement

- Australian Taxation Office - Superannuation

- Superannuation Plain Talk Guides by Vanguard Investments Australia

- Retail Superannuation Find a Fund tool by 2020 DIRECTINVEST

- Trustee IT: New turnkey information technology for Superannuation Funds to help reduce 'per member' costs as recommended by the Cooper Review

Australian economy History Currency State economies Industries Agriculture · Tourism · Insurance · Property market · Fishing industry · Mining · Wine · Manufacturing · Car industry · Transport · Telecommunications · Ports · SuperannuationTaxation Banking and Finance Regulatory agencies Reserve Bank · ACCC · Corporations law · AIRC · APRA · ASIC · ASX · S&P/ASX 50 · S&P/ASX 200 · Corporations powerEnergy Energy efficiency rating · Biofuel · Wind power · Geothermal power · National Electricity Market · Green electricityEconomic conditions Unions Trade agreements

Wikimedia Foundation. 2010.