- Economic history of the Russian Federation

-

Contents

Historical background

Main article: Economic history of the Soviet UnionFor about 60 years, the Russian economy and that of the rest of the Soviet Union operated on the basis of a centrally planned economy, with a state control over virtually all means of production and over investment, production, and consumption decisions throughout the economy. Economic policy was made according to directives from the Communist Party, which controlled all aspects of economic activity. Since the collapse of Communism in the early 1990s, Russia has experienced difficulties in making the transition from a centrally planned economy to a market based economy.

Much of the structure of the Soviet economy that operated until 1987 originated under the leadership of Joseph Stalin, with only incidental modifications made between 1953 and 1987. Five-year plan and annual plans were the chief mechanisms the Soviet government used to translate economic policies into programs. According to those policies, the State Planning Committee (Gosudarstvennyy planovyy komitet—Gosplan) formulated countrywide output targets for stipulated planning periods. Regional planning bodies then refined these targets for economic units such as state industrial enterprises and state farms (sovkhozy; sing., sovkhoz) and collective farms (kolkhozy; sing., kolkhoz), each of which had its own specific output plan. Central planning operated on the assumption that if each unit met or exceeded its plan, then demand and supply would balance.

The government's role was to ensure that the plans were fulfilled. Responsibility for production flowed from the top down. At the national level, some seventy government ministries and state committees, each responsible for a production sector or subsector, supervised the economic production activities of units within their areas of responsibility. Regional ministerial bodies reported to the national-level ministries and controlled economic units in their respective geographical areas.

Map of the electric grid during the Soviet era.

Map of the electric grid during the Soviet era.

The plans incorporated output targets for raw materials and intermediate goods as well as final goods and services. In theory, but not in practice, the central planning system ensured a balance among the sectors throughout the economy. Under central planning, the state performed the allocation functions that prices perform in a market system. In the Soviet economy, prices were an accounting mechanism only. The government established prices for all goods and services based on the role of the product in the plan and on other noneconomic criteria. This pricing system produced anomalies. For example, the price of bread, a traditional staple of the Russian diet, was below the cost of the wheat used to produce it. In some cases, farmers fed their livestock bread rather than grain because bread cost less. In another example, rental fees for apartments were set very low to achieve social equity, yet housing was in extremely short supply. Soviet industries obtained raw materials such as oil, natural gas, and coal at prices below world market levels, encouraging waste.

The central planning system allowed Soviet leaders to marshal resources quickly in times of crisis, such as the Nazi invasion, and to reindustrialize the country during the postwar period. The rapid development of its defence and industrial base after the war permitted the Soviet Union to become a superpower.

The attempts and failures of reformers during the era of perestroika (restructuring) in the regime of Mikhail Gorbachev (1985–91) attested to the complexity of the challenge.

Transition to Market Economy

After 1991, under the leadership of Boris Yeltsin, the country made a significant turn toward developing a market economy by implanting basic tenets such as market-determined prices. Two fundamental and interdependent goals — macroeconomic stabilization and economic restructuring — the transition from central planning to a market-based economy. The former entailed implementing fiscal and monetary policies that promote economic growth in an environment of stable prices and exchange rates. The latter required establishing the commercial, and institutional entities — banks, private property, and commercial legal codes— that permit the economy to operate efficiently. Opening domestic markets to foreign trade and investment, thus linking the economy with the rest of the world, was an important aid in reaching these goals. The Gorbachev regime failed to address these fundamental goals. At the time of the Soviet Union's demise, the Yeltsin government of the Russian Republic had begun to attack the problems of macroeconomic stabilization and economic restructuring. By mid-1996, the results were mixed.

Since collapse of the Soviet Union in 1991, Russia has tried to develop a market economy and achieve consistent economic growth. In October 1991, Yeltsin announced that Russia would proceed with radical, market-oriented reform along the lines of "shock therapy", as recommended by the United States and IMF.[1] However, this policy resulted in economic collapse, with millions being plunged into poverty and corruption and crime spreading rapidly.[2] Hyperinflation resulted from the removal of Soviet price controls and again following the 1998 Russian financial crisis. Assuming the role as the continuing legal personality of the Soviet Union, Russia took up the responsibility for settling the USSR's external debts, even though its population made up just half of the population of the USSR at the time of its dissolution.[3]

The Russian GDP contracted an estimated 40% between 1991 and 1998, despite the country's wealth of natural resources, its well-educated population, and its diverse - although increasingly dilapidated - industrial base. Such a figure may be misleading, however, since much of the Soviet Union's GDP was military spending and the production of goods for which there was little demand. The discontinuation of much of that wasteful spending created the false impression of larger than actual economic contraction.[4]

Critical elements such as privatization of state enterprises and extensive foreign investment were rushed into place in the first few years of the post-Soviet period. But other fundamental parts of the economic infrastructure, such as commercial banking and authoritative, comprehensive commercial laws, were absent or only partly in place by 1996. Although by the mid-1990s a return to Soviet-era central planning seemed unlikely, the configuration of the post-transition economy remained unpredictable.

Monetary and fiscal policies

In January 1992, the government clamped down on money and credit creation at the same time that it lifted price controls. However, beginning in February, the Central Bank, headed by Viktor Gerashchenko, loosened the reins on the money supply. In the second and third quarters of 1992, the money supply had increased at especially sharp rates of 34% and 30%, respectively. By the end of 1992, the Russian money supply had increased by eighteen times. This led directly to high inflation and to a deterioration in the exchange rate of the ruble.

The sharp increase in the money supply was influenced by large foreign currency deposits that state-run enterprises and individuals had built up, and by the depreciation of the ruble. Enterprises drew on these deposits to pay wages and other expenses after the Government had tightened restrictions on monetary emissions. Commercial banks monetized enterprise debts by drawing down accounts in foreign banks and drawing on privileged access to accounts in the Central Bank.

Inflation

In 1992, the first year of economic reform, retail prices in Russia increased by 2,520%. A major cause of the increase was the deregulation of most of the prices in January 1992, a step that prompted an average price increase of 245% in that month alone. By 1993 the annual rate had declined to 240%, still a very high figure. In 1994 the inflation rate had improved to 224%.[citation needed]

Trends in annual inflation rates mask variations in monthly rates, however. In 1994, for example, the government managed to reduce monthly rates from 21% in January to 4% in August, but rates climbed once again, to 16.4% by December and 18% by January 1995. Instability in Russian monetary policy caused the variations. After tightening the flow of money early in 1994, the Government loosened its restrictions in response to demands for credits by agriculture, industries in the Far North, and some favored large enterprises. In 1995 the pattern was avoided more successfully by maintaining the tight monetary policy adopted early in the year and by passing a relatively stringent budget. Thus, the monthly inflation rate held virtually steady below 5% in the last quarter of the year. For the first half of 1996, the inflation rate was 16.5%. However, experts noted that control of inflation was aided substantially by the failure to pay wages to workers in state enterprises, a policy that kept prices low by depressing demand.[citation needed] [5]

Exchange rates

An important symptom of Russian macroeconomic instability has been severe fluctuations in the exchange rate of the ruble. From July 1992, when the ruble first could be legally exchanged for United States dollars, to October 1995, the rate of exchange between the ruble and the dollar declined from 144 rubles per US$1 to around 5,000 per US$1. Prior to July 1992, the ruble's rate was set artificially at a highly overvalued level. But rapid changes in the nominal rate (the rate that does not account for inflation) reflected the overall macroeconomic instability. The most drastic example of such fluctuation was the Black Tuesday (1994) 27% reduction in the ruble's value.[citation needed]

In July 1995, the Central Bank announced its intention to maintain the ruble within a band of 4,300 to 4,900 per US$1 through October 1995, but it later extended the period to June 1996. The announcement reflected strengthened fiscal and monetary policies and the buildup of reserves with which the government could defend the ruble. By the end of October 1995, the ruble had stabilized and actually appreciated in inflation-adjusted terms. It remained stable during the first half of 1996. In May 1996, a "crawling band" exchange rate was introduced to allow the ruble to depreciate gradually through the end of 1996, beginning between 5,000 and 5,600 per US $1 and ending between 5,500 and 6,100.[citation needed]

Another sign of currency stabilization was the announcement that effective June 1996, the ruble would become fully convertible on a current-account basis. This meant that Russian citizens and foreigners would be able to convert rubles to other currencies for trade transactions.[citation needed]

Privatization

When once all enterprises belonged to the state and were supposed to be equally owned amongst all citizens, they fell into the hands of a few, who became immensely rich. Stocks of the state-owned enterprises were issued, and these new publicly traded companies were quickly handed to the members of Nomenklatura or known criminal bosses. For example, the director of a factory during the Soviet regime would often become the owner of the same enterprise. During the same period, violent criminal groups often took over state enterprises, clearing the way by assassinations or extortion. Corruption of government officials became an everyday rule of life. Under the government's cover, outrageous financial manipulations were performed that enriched the narrow group of individuals at key positions of the business and government mafia. Many took billions in cash and assets outside of the country in an enormous capital flight.[6]

The largest state enterprises were controversially privatized by President Boris Yeltsin to insiders[7] for far less than they were worth.[1] Many Russians consider these infamous "oligarchs" to be thieves.[8] Through their immense wealth, the oligarchs wielded significant political influence.

1991-1992

Government efforts to take over the credit expansion also proved ephemeral in the early years of the transition. Domestic credit increased about nine times between the end of 1991 and 1992. The credit expansion was caused in part by the buildup of interenterprise arrears and the RCB's subsequent financing of those arrears. The Government restricted financing to state enterprises after it lifted controls on prices in January 1992, but enterprises faced cash shortages because the decontrol of prices cut demand for their products. Instead of curtailing production, most firms chose to build up inventories. To support continued production under these circumstances, enterprises relied on loans from other enterprises. By mid-1992, when the amount of unpaid interenterprise loans had reached 3.2 trillion rubles (about US$20 billion), the government froze interenterprise debts. Shortly thereafter, the government provided 181 billion rubles (about US$1.1 billion) in credits to enterprises that were still holding debt.[citation needed]

The government also failed to constrain its own expenditures in this period, partially under the influence of the post-Soviet Supreme Soviet of Russia, which encouraged the Soviet-style financing of favored industries. By the end of 1992, the Russian budget deficit was 20% of GDP, much higher than the 5% projected under the economic program and stipulated under the International Monetary Fund (IMF) conditions for international funding. This budget deficit was financed largely by expanding the money supply. These monetary and fiscal policies were a factor along with price liberalization in an inflation rate of over 2,000% in 1992.[citation needed]

In late 1992, deteriorating economic conditions and a sharp conflict with the parliament led Yeltsin to dismiss neoliberal reform advocate Yegor Gaidar as prime minister. Gaidar's successor was Viktor Chernomyrdin, a former head of the State Natural Gas Company (Gazprom), who was considered less favorable to neoliberal reform.[citation needed]

1993

Chernomyrdin formed a new government with Boris Fedorov, an economic reformer, as deputy prime minister and finance minister. Fedorov considered macroeconomic stabilization a primary goal of Russian economic policy. In January 1993, Fedorov announced a so-called anticrisis program to control inflation through tight monetary and fiscal policies. Under the program, the government would control money and credit emissions by requiring the RCB to increase interest rates on credits by issuing government bonds, by partially financing budget deficits, and by starting to close inefficient state enterprises. Budget deficits were to be brought under control by limiting wage increases for state enterprises, by establishing quarterly budget deficit targets, and by providing a more efficient social safety net for the unemployed and pensioners.[citation needed]

The printing of money and domestic credit expansion moderated somewhat in 1993. In a public confrontation with the parliament, Yeltsin won a referendum on his economic reform policies that may have given the reformers some political clout to curb state expenditures. In May 1993, the Ministry of Finance and the Central Bank agreed to macroeconomic measures, such as reducing subsidies and increasing revenues, to stabilize the economy. The Central Bank was to raise the discount lending rate to reflect inflation. Based on positive early results from this policy, the IMF extended the first payment of US$1.5 billion to Russia from a special Systemic Transformation Facility (STF) the following July.[citation needed]

Fedorov's anticrisis program and the Government's accord with the Central Bank had some effect. In the first three quarters of 1993, the Central Bank held money expansion to a monthly rate of 19%. It also substantially moderated the expansion of credits during that period. The 1993 annual inflation rate was around 1,000%, a sharp improvement over 1992, but still very high. The improvement figures were exaggerated, however, because state expenditures had been delayed from the last quarter of 1993 to the first quarter of 1994. State enterprise arrears, for example, had built up in 1993 to about 15 trillion rubles (about US$13 billion, according to the mid-1993 exchange rate).[citation needed]

1994

In June 1994, Chernomyrdin presented a set of moderate reforms calculated to accommodate the more conservative elements of the Government and parliament while placating reformers and Western creditors. The prime minister pledged to move ahead with restructuring the economy and pursuing fiscal and monetary policies conducive to macroeconomic stabilization. But stabilization was undermined by the Central Bank, which issued credits to enterprises at subsidized rates, and by strong pressure from industrial and agricultural lobbies seeking additional credits.[citation needed]

By October 1994, inflation, which had been reduced by tighter fiscal and monetary policies early in 1994, began to soar once again to dangerous levels. On 11 October, a day that became known as Black Tuesday, the value of the ruble on interbank exchange markets plunged by 27%. Although experts presented a number of theories to explain the drop, including the existence of a conspiracy, the loosening of credit and monetary controls clearly was a significant cause of declining confidence in the Russian economy and its currency.[citation needed]

In late 1994, Yeltsin reasserted his commitment to macroeconomic stabilization by firing Viktor Gerashchenko, head of the Central Bank, and nominating Tatyana Paramonova as his replacement. Although reformers in the Russian government and the IMF and other Western supporters greeted the appointment with skepticism, Paramonova was able to implement a tight monetary policy that ended cheap credits and restrained interest rates (although the money supply fluctuated in 1995). Furthermore, the parliament passed restrictions on the use of monetary policy to finance the state debt, and the Ministry of Finance began to issue government bonds at market rates to finance the deficits.[citation needed]

The government also began to address the interenterprise debt that had been feeding inflation. The 1995 budget draft, which was proposed in September 1994, included a commitment to reducing inflation and the budget deficit to levels acceptable to the IMF, with the aim of qualifying for additional international funding. In this budget proposal, the Chernomyrdin government sent a signal that it no longer would tolerate soft credits and loose budget constraints, and that stabilization must be a top government priority.[citation needed]

According to official Russian data, in 1994 the national gross domestic product (GDP) was 604 trillion rubles (about US$207 billion according to the 1994 exchange rate), or about 4% of the United States GDP for that year. But this figure underestimates the size of the Russian economy. Adjusted by a purchasing-power parity formula to account for the lower cost of living in Russia, the 1994 Russian GDP was about US$678 billion, making the Russian economy approximately 10% of the United States economy. In 1994 the adjusted Russian GDP was US$4,573 per capita, approximately 19% of that of the United States.

1995

During most of 1995, the government maintained its commitment to tight fiscal constraints, and budget deficits remained within prescribed parameters. However, in 1995 pressures mounted to increase government spending to alleviate wage arrearages, which were becoming a chronic problem within state enterprises, and to improve the increasingly tattered social safety net. In fact, in 1995 and 1996 the state's failure to pay many such obligations (as well as the wages of most state workers) was a major factor in keeping Russia's budget deficit at a moderate level. Conditions changed by the second half of 1995. The members of the State Duma (beginning in 1994, the lower house of the Federal Assembly, Russia's parliament) faced elections in December, and Yeltsin faced dim prospects in his 1996 presidential reelection bid. Therefore, political conditions caused both Duma deputies and the president to make promises to increase spending.[citation needed]

In addition, late in 1995 Yeltsin dismissed Anatoly Chubais, one of the last economic reform advocates remaining in a top Government position, as deputy prime minister in charge of economic policy. In place of Chubais, Yeltsin named Vladimir Kadannikov, a former automobile plant manager whose views were antireform. This move raised concerns in Russia and the West about Yeltsin's commitment to economic reform. Another casualty of the political atmosphere was RCB chairman Paramonova, whose nomination had remained a source of controversy between the State Duma and the Government. In November 1995, Yeltsin was forced to replace her with Sergey Dubinin, a Chernomyrdin protégé who continued the tight-money policy that Paramonova had established.[citation needed]

1996

As of mid-1996, four and one-half years after the launching of Russia's post-Soviet economic reform, experts found the results promising but mixed. The Russian economy has passed through a long and wrenching depression. Official Russian economic statistics indicate that from 1990 to the end of 1995, Russian GDP declined by roughly 50%, far greater than the decline that the United States experienced during the Great Depression.[citation needed] (However, alternative estimates by Western neoliberal pro-disregulation analysts described a much less severe decline, taking into account the upward bias of Soviet-era economic data and the downward bias of post-Soviet data. E.g. IMF estimates: [1]) Much of the decline in production has occurred in the military-industrial complex and other heavy industries that benefited most from the economic priorities of Soviet planners but have much less robust demand in a free market.

But other major sectors such as agriculture, energy, and light industry also suffered from the transition. To enable these sectors to function in a market system, inefficient enterprises had to be closed and workers laid off, with resulting declines in output and consumption. Analysts had expected that Russia's GDP would begin to rise in 1996, but data for the first six months of the year showed a continuing decline, and some Russian experts predicted a new phase of economic crisis in the second half of the year.

The pain of the restructuring has been assuaged somewhat by the emergence of a new private sector. Western experts believe that Russian data overstate the dimensions of Russia's economic collapse by failing to reflect a large portion of the country's private-sector activity. The Russian services sector, especially retail sales, is playing an increasingly vital role in the economy, accounting for nearly half of GDP in 1995. The services sector's activities have not been adequately measured. Data on sector performance are skewed by the underreporting or nonreporting of output that Russia's tax laws encourage. According to Western analysts, by the end of 1995 more than half of GDP and more than 60% of the labor force were based in the private sector.

An important but unconventional service in Russia's economy is "shuttle trading" — the transport and sale of consumer goods by individual entrepreneurs, of whom 5 to 10 million were estimated to be active in 1996. Traders buy goods in foreign countries such as China, Turkey, and the United Arab Emirates and in Russian cities, then sell them on the domestic market where demand is highest. Yevgeniy Yasin, minister of economics, estimated that in 1995 some US$11 billion worth of goods entered Russia in this way. Shuttle traders have been vital in maintaining the standard of living of Russians who cannot afford consumer goods on the conventional market. However, domestic industries such as textiles suffer from this infusion of competing merchandise, whose movement is unmonitored, untaxed, and often mafia-controlled.

The geographical distribution of Russia's wealth has been skewed at least as severely as it was in Soviet times. By the mid-1990s, economic power was being concentrated in Moscow at an even faster rate than the federal government was losing political power in the rest of the country. In Moscow an economic oligarchy, composed of politicians, banks, businesspeople, security forces, and city agencies, controlled a huge percentage of Russia's financial assets under the rule of Moscow's energetic and popular mayor, Yuriy Luzhkov. Unfortunately, organized crime also has played a strong role in the growth of the city. Opposed by a weak police force, Moscow's rate of protection rackets, contract murders, kickbacks, and bribes — all intimately connected with the economic infrastructure — has remained among the highest in Russia. Most businesses have not been able to function without paying for some form of mafia protection, informally called a krysha (the Russian word for roof).

Luzhkov, who has close ties to all legitimate power centers in the city, has overseen the construction of sports stadiums, shopping malls, monuments to Moscow's history, and the ornate Christ the Savior Cathedral. In 1994 Yeltsin gave Luzhkov full control over all state property in Moscow. In the first half of 1996, the city privatized state enterprises at the rate of US$1 billion per year, a faster rate than the entire national privatization process in the same period. Under Luzhkov's leadership, the city government also acquired full or major interests in a wide variety of enterprises — from banking, hotels, and construction to bakeries and beauty salons. Such ownership has allowed Luzhkov's planners to manipulate resources efficiently and with little or no competition. Meanwhile, Moscow also became the center of foreign investment in Russia, often to the exclusion of other regions. For example, the McDonald's fast-food chain, which began operations in Moscow in 1990, enjoyed immediate success but expanded only in Moscow. The concentration of Russia's banking industry in Moscow gave the city a huge advantage in competing for foreign commercial activity.

In mid-1996 the national government appeared to have achieved some degree of macroeconomic stability. However, longer-term stability depends on the ability of policy makers to withstand the inflationary pressures of demands for state subsidies and easier credits for failing enterprises and other special interests. (Chubais estimated that spending promises made during Yeltsin's campaign amounted to US$250 per voter, which if actually spent would approximately double the national budget deficit; most of Yeltsin's pledges seemingly were forgotten shortly after his reelection.)

By 1996 the structure of Russian economic output had shifted far enough that it more closely resembled that of a developed market economy than the distorted Soviet central-planning model. With the decline in demand for defense industry goods, overall production has shifted from heavy industry to consumer production. However, in the mid-1990s the low quality of most domestically produced consumer goods continued to limit enterprises' profits and therefore their ability to modernize production operations. On the other side of the "vicious circle," reliance on an outmoded production system guaranteed that product quality would remain low and uncompetitive.

Most prices were left to the market, although local and regional governments control the prices of some staples. Energy prices remain controlled, but the Government has been shifting these prices upward to close the gap with world market prices.

A 1996 government report quantified so-called "shadow economy" which yields no taxes or government statistics as accounting for about 51% of the economy and 40% of its cash turnover.

1997-1998

By the end of 1997, Russia had achieved some progress. Inflation had been brought under control, the ruble was stabilized, and an ambitious privatization program had transferred thousands of enterprises to private ownership. Some important market-oriented laws had also been passed, including a commercial code governing business relations and the establishment of an arbitration court for resolving economic disputes.

But in 1998 difficulties in implementing fiscal reforms aimed at raising government revenues and a dependence on short-term borrowing to finance budget deficits led to a serious financial crisis in 1998, contributing to a sharp decline in Russia's earnings from oil exports and resulting in an exodus of foreign investors. The government allowed the ruble to fall precipitously and stopped payment on $40 billion in ruble bonds.

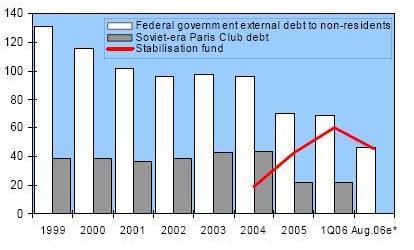

Russian public debt

Russian public debt1999

In 1999, output increased for only the second time since 1991, by an officially estimated 6.4%, regaining 4.6% drop of 1998. This increase was achieved despite a year of potential turmoil that included the tenure of three premiers and culminated in the New Year's Eve resignation of President Boris Yeltsin. Of great help was the tripling of international oil prices in the second half of 1999, raising the export surplus to $29 billion.

On the negative side, inflation rose to an average 85% in 1998, compared with a 11% average in 1997 and a hoped-for 36% average in 1999. Ordinary persons found their wages falling by roughly 30% and their pensions by 45%. The Vladimir Putin government has given high priority to supplementing low incomes by paying down wage and pension arrears.

2000-2007

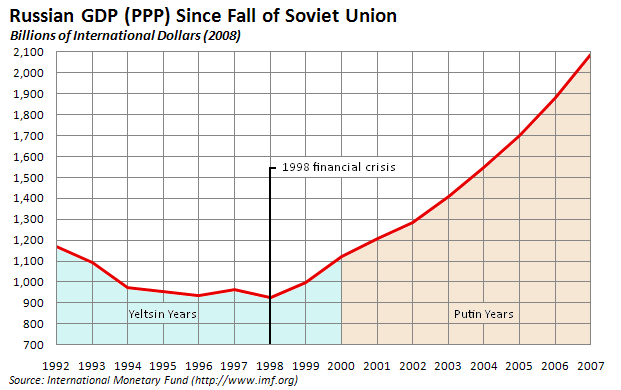

Russian economy since fall of the Soviet Union.

Russian economy since fall of the Soviet Union.Russia posted gross domestic product growth of 6.4% in 1999, 10% in 2000, 5.1% in 2001, 4.7% in 2002, 7.3% in 2003, 7.2% in 2004, 6.4% in 2005, 8.2% in 2006 and 8.5% in 2007[9] with industrial sector posting high growth figures as well.

Under the presidency of Vladimir Putin Russia's economy saw the nominal Gross Domestic Product (GDP) double, climbing from 22nd to 11th largest in the world. The economy made real gains of an average 7% per year (2000: 10%, 2001: 5.1%, 2002: 4.7%, 2003: 7.3%, 2004: 7.2%, 2005: 6.4%, 2006: 8.2%, 2007: 8.5%, 2008: 5.6%), making it the 6th largest economy in the world in GDP(PPP). In 2007, Russia's GDP exceeded that of 1990, meaning it has overcome the devastating consequences of the Soviet era, 1998 financial crisis, and preceding recession in the 1990s.[10] On a per capita basis, Russian GDP was US$11,339 per individual in 2008, making Russians 57th richest on both a purchasing power and nominal basis.

During Putin's eight years in office, industry grew by 75%, investments increased by 125%,[10] and agricultural production and construction increased as well. Real incomes more than doubled and the average salary increased eightfold from $80 to $640.[11][12][13] The volume of consumer credit between 2000–2006 increased 45 times,[14][15] and during that same time period, the middle class grew from 8 million to 55 million, an increase of 7 times. The number of people living below the poverty line also decreased from 30% in 2000 to 14% in 2008.[10][16][17]

Inflation remained a problem however, as the government failed to contain the growth of prices. Between 1999–2007 inflation was kept at the forecast ceiling only twice, and in 2007 the inflation exceeded that of 2006, continuing an upward trend at the beginning of 2008.[10]

In the June 2002 G8 Summit, leaders of the eight nations signed a statement agreeing to explore cancellation of some of Russia's old Soviet debt to use the savings for safeguarding materials in Russia that could be used by terrorists. Under the proposed deal, $10 billion would come from the United States and $10 billion from other G-8 countries over 10 years.

In 2003, the debt has risen to $19 billion due to higher Ministry of Finance and Eurobond payments. However, $1 billion of this has been prepaid, and some of the private sector debt may already have been repurchased. Russia continued to explore debt swap/exchange opportunities.

On January 1, 2004, the Stabilization fund of the Russian Federation was established by the Government of Russia as a part of the federal budget to balance it if oil price falls. Now the Stabilization fund of the Russian Federation]] is being modernized. The Stabilization Fund was be divided into two parts on February 1, 2008. The first part is a reserve fund equal to 10 percent of GDP (10% of GDP equals to about $200 billion now), and is invested in a similar way as the Stabilization Fund. The second part is turned into the National Prosperity Fund of Russian Federation. The National Prosperity Fund is to be invested into more risky instruments, including the shares of foreign companies. Shyhkin, Maxim. "Stabilization Fund to Be Converted into National Prosperity". http://www.kommersant.com/p791856/new_fund_to_specialize_on_portfolio_investments/. Retrieved 2007-08-02.

The Russian economy remained commodity-driven despite its growth. Payments from the fuel and energy sector in the form of customs duties and taxes accounted for nearly half of the federal budget's revenues. The large majority of Russia's exports was made up by raw materials and fertilizers,[10] although exports as a whole accounted for only 8.7% of the GDP in 2007, compared to 20% in 2000.[18]

There was also a growing gap between rich and poor in Russia. Between 2000–2007 the incomes of the rich grew from approximately 14 times to 17 times larger than the incomes of the poor. The income differentiation ratio shows that the 10% of Russia's rich live increasingly better than the 10% of the poor, amongst whom are mostly pensioners and unskilled workers in depressive regions. (See: Gini Coefficient)

Russia has been experiencing a boom in capital investment since the beginning of 2007. Capital investment showed record growth in June, rising 27.2 percent over June of last year in real terms (adjusted for price changes), to 579.8 billion rubles, with construction industry leading the way. That is a rise of 58 percent in nominal terms and a better showing than in China. Modern Russia has never before seen such a growth rate. The rate of investment in Russia rose 22.3 percent in the first half of 2007 compared to the same period the year before. The increase during that period in 2005 was only 11 percent. The statistics significantly exceed both the conservative prognoses of the Ministry of Economic Development and Trade and less conservative independent analyses. According to Interfax, the consensus among analysts at the end of last month 15.3-percent growth compared to last year.[19]

As of 2007 real GDP increased by the highest percentage since the fall of the Soviet Union at 8.1%, the ruble remains stable, inflation has been moderate, and investment began to increase again. In 2007 the World Bank declared that the Russian economy had achieved "unprecedented macroeconomic stability".[20] Russia is making progress in meeting its foreign debts obligations. During 2000-01, Russia not only met its external debt services but also made large advance repayments of principal on IMF loans but also built up Central Bank reserves with government budget, trade, and current account surpluses. The FY 2002 Russian Government budget assumes payment of roughly $14 billion in official debt service payments falling due. Large current account surpluses have brought a rapid appreciation of the ruble over the past several years. This has meant that Russia has given back much of the terms-of-trade advantage that it gained when the ruble fell by 60% during the debt crisis. Oil and gas dominate Russian exports, so Russia remains highly dependent upon the price of energy. Loan and deposit rates at or below the inflation rate inhibit the growth of the banking system and make the allocation of capital and risk much less efficient than it would be otherwise.

By the end of first decade of 21st century, the ECB reported that the country has caught a new strain of Dutch disease.[21]

2008-present

See also: 2008–2009 Russian financial crisisArms sales have increased to the point where Russia is second (with 0.6 the amount of US arms sale) in the world in sale of weapons, the IT industry has recorded a record year of growth concentrating on high end niches like algorithm design and microelectronics, while leaving the lesser end work to India and China; Russia is now the world's third biggest destination for outsourcing software behind India and China. The space launch industry is now the world's second largest behind the European Ariane 5 and nuclear power plant companies are going from strength to strength, selling plants to China and India, and recently signed a joint venture with Toshiba to develop cutting edge power plants.

The civilian aerospace industry has developed the Sukhoi Superjet, as well as the upcoming MS 21 project to compete with Boeing and Airbus.

The recent global economic downturn has resulted in three major shocks to Russia's long-term economic growth, though. Oil prices dropped from $140 per barrel to $40 per barrel, a decrease in access to financing with an increase in sovereign and corporate bond spreads, and the reversal of capital flows from $80 billion of in-flows to $130 billion of out-flows have all served to crush fledging Russian economic growth. In January 2009, industrial production was down almost 16% year to year, fixed capital investment was down 15.5% year to year, and GDP had shrunk 9% year to year.[22] However, in the second quarter the GDP rose by 7.5 percent on a quarterly basis indicating the beginning of economic recovery.

See also

References

- ^ a b "Nuffield Poultry Study Group—Visit to Russia". pg 7. The BEMB Research and Education Trust. Archived from the original on 2007-11-30. http://web.archive.org/web/20071130222528/http://www.bembtrust.org.uk/Russia+Report+no+app.pdf. Retrieved 2007-12-27.

- ^ "Members". APEC Study Center; City University of Hong Kong. http://www.fb.cityu.edu.hk/research/apec/index.cfm?page=members. Retrieved 2007-12-27.

- ^ "Russia pays off USSR’s entire debt, sets to become crediting country". Pravda.ru. http://english.pravda.ru/russia/economics/22-08-2006/84038-paris-club-0. Retrieved 2007-12-27.

- ^ Schliefer, Andrei; Treisman, Daniel, October 2003 A Normal Country - Harvard Institute of Economic Research Retrieved on February 25, 2009

- ^ Russians abroad

- ^ "Russia: Clawing Its Way Back to Life (int'l edition)". BusinessWeek. http://www.businessweek.com/1999/99_48/b3657252.htm. Retrieved 2007-12-27.

- ^ Nicholson, Alex. "Metal is the latest natural resource bonanza for Russia". International Herald Tribune. http://www.iht.com/articles/2007/08/14/business/metal.php.

- ^ Page, Jeremy (May 16, 2005). "Analysis: punished for his political ambitions". London: The Times. http://www.timesonline.co.uk/tol/news/world/article523129.ece. Retrieved 2007-12-27.

- ^ Russia's GDP growth reached 8.5% in 2007 - statistics service Novosti Retrieved on March 19, 2008

- ^ a b c d e Russia’s economy under Vladimir Putin: achievements and failures RIA Novosti Retrieved on May 1, 2008

- ^ Russians weigh an enigma with Putin’s protégé MSNBC Retrieved on May 3, 2008

- ^ Medvedev is new Russian president Al Jazeera Retrieved on May 7, 2008

- ^ Putin’s Economy – Eight Years On Russia Profile, Retrieved on April 23, 2008

- ^ РОЗНИЧНЫЙ ПОДХОД. Российские банки борются за частников

- ^ Ежегодно объем потребительского кредитования в России удваивается

- ^ ОСНОВНЫЕ СОЦИАЛЬНО-ЭКОНОМИЧЕСКИЕ ИНДИКАТОРЫ УРОВНЯ ЖИЗНИ НАСЕЛЕНИЯ

- ^ CIA - The World Factbook - Russia

- ^ Rosstat Confirms Record GDP Growth Kommersant Retrieved on May 5, 2008

- ^ Shyshkin, Maxim. "The Russian Investment Boom Continues". http://www.kommersant.com/p788945/finance_macroeconomics/. Retrieved 2007-07-23.

- ^ Russia attracts investors despite its image BBC News Retrieved on March 2008

- ^ Mining accounts for most of the economic growth(pdf)

- ^ Russia in the Global Storm. http://www.carnegieendowment.org/events/?fa=eventDetail&id=1326. April 21, 2009.

External links

Economy of Russia History Soviet Union · Privatization · 1998 financial crisis · National Priority Projects · 2008–2009 financial crisis · Medvedev modernisation programme · Timeline of largest projects

Natural resources Timber · Mining · Aluminium · Oil reserves · Energy · Nuclear power · Geothermal power · Renewable energyAgriculture Industry Aircraft · Automotive · Defence · Petroleum industry · Shipbuilding · Science and technology · Space industryServices Regional economies Natural resources of Primorsky Krai · Federal subjects by GRP · Federal subjects by HDI · Federal subjects by unemployment rateEconomic regions Central · Ural · North Caucasus · Volga · West Siberian · East Siberian · Volga-Vyatka · Northwestern · Central Black Earth · Far Eastern · NorthernOther Categories:

Wikimedia Foundation. 2010.