- Microfinance

-

Community-based savings bank in Cambodia. There are a rich variety of financial institutions which serve the poor.

Community-based savings bank in Cambodia. There are a rich variety of financial institutions which serve the poor.

Microfinance is the provision of financial services to low-income clients or solidarity lending groups including consumers and the self-employed, who traditionally lack access to banking and related services.

More broadly, it is a movement whose object is "a world in which as many poor and near-poor households as possible have permanent access to an appropriate range of high quality financial services, including not just credit but also savings, insurance, and fund transfers."[1] Those who promote microfinance generally believe that such access will help poor people out of poverty.

Microfinance is a broad category of services, which includes microcredit. Microcredit is provision of credit services to poor clients. Although microcredit is one of the aspects of microfinance, conflation of the two terms is endemic in public discourse. Critics often attack microcredit while referring to it indiscriminately as either 'microcredit' or 'microfinance'. Due to the broad range of microfinance services, it is difficult to assess impact, and very few studies have tried to assess its full impact.[2]

Challenges

Traditionally, banks have not provided financial services, such as loans, to clients with little or no cash income. Banks incur substantial costs to manage a client account, regardless of how small the sums of money involved. For example, although the total gross revenue from delivering one hundred loans worth $1,000 each will not differ greatly from the revenue that results from delivering one loan of $100,000, it takes nearly a hundred times as much work and cost to manage a hundred loans as it does to manage one. The fixed cost of processing loans of any size is considerable as assessment of potential borrowers, their repayment prospects and security; administration of outstanding loans, collecting from delinquent borrowers, etc., has to be done in all cases. There is a break-even point in providing loans or deposits below which banks lose money on each transaction they make. Poor people usually fall below that breakeven point. A similar equation resists efforts to deliver other financial services to poor people.

In addition, most poor people have few assets that can be secured by a bank as collateral. As documented extensively by Hernando de Soto and others, even if they happen to own land in the developing world, they may not have effective title to it.[3] This means that the bank will have little recourse against defaulting borrowers.

Seen from a broader perspective, the development of a healthy national financial system has long been viewed as a catalyst for the broader goal of national economic development (see for example Alexander Gerschenkron, Paul Rosenstein-Rodan, Joseph Schumpeter, Anne Krueger ). However, the efforts of national planners and experts to develop financial services for most people have often failed in developing countries, for reasons summarized well by Adams, Graham & Von Pischke in their classic analysis 'Undermining Rural Development with Cheap Credit'.[4]

Because of these difficulties, when poor people borrow they often rely on relatives or a local moneylender, whose interest rates can be very high. An analysis of 28 studies of informal moneylending rates in 14 countries in Asia, Latin America and Africa concluded that 76% of moneylender rates exceed 10% per month, including 22% that exceeded 100% per month. Moneylenders usually charge higher rates to poorer borrowers than to less poor ones.[5] While moneylenders are often demonized and accused of usury, their services are convenient and fast, and they can be very flexible when borrowers run into problems. Hopes of quickly putting them out of business have proven unrealistic, even in places where microfinance institutions are active.[citation needed]

Over the past centuries practical visionaries, from the Franciscan monks who founded the community-oriented pawnshops of the 15th century, to the founders of the European credit union movement in the 19th century (such as Friedrich Wilhelm Raiffeisen) and the founders of the microcredit movement in the 1970s (such as Muhammad Yunus) have tested practices and built institutions designed to bring the kinds of opportunities and risk-management tools that financial services can provide to the doorsteps of poor people.[6] While the success of the Grameen Bank (which now serves over 7 million poor Bangladeshi women) has inspired the world, it has proved difficult to replicate this success. In nations with lower population densities, meeting the operating costs of a retail branch by serving nearby customers has proven considerably more challenging. Hans Dieter Seibel, board member of the European Microfinance Platform, is in favour of the group model. This particular model (used by many Microfinance institutions) makes financial sense, he says, because it reduces transaction costs. Microfinance programmes also need to be based on local funds. Local Roots

Although much progress has been made, the problem has not been solved yet, and the overwhelming majority of people who earn less than $1 a day, especially in the rural areas, continue to have no practical access to formal sector finance. Microfinance has been growing rapidly with $25 billion currently at work in microfinance loans.[7] It is estimated that the industry needs $250 billion to get capital to all the poor people who need it.[7] The industry has been growing rapidly, and concerns have arisen that the rate of capital flowing into microfinance is a potential risk unless managed well.[8]

As seen in the State of Andhra Pradesh (India), these systems can easily fail. Some reasons being lack of use by potential customers, over-indebtedness, poor operating procedures, neglect of duties and inadequate regulations.[9]

History

The history of microfinancing can be traced back as long to the middle of the 1800s when the theorist Lysander Spooner was writing over the benefits from small credits to entrepreneurs and farmers as a way getting the people out of poverty. But it was at the end of World War II with the Marshall plan that the concept had a big impact.

The today use of the expression microfinancing has it roots in the 1970s when organizations, such as Grameen Bank of Bangladesh with the microfinance pioneer Muhammad Yunus, were starting and shaping the modern industry of microfinancing. Another pioneer in this sector is Akhtar Hameed Khan.

Boundaries and principles

Poor people borrow from informal moneylenders and save with informal collectors. They receive loans and grants from charities. They buy insurance from state-owned companies. They receive funds transfers through formal or informal remittance networks. It is not easy to distinguish microfinance from similar activities. It could be claimed that a government that orders state banks to open deposit accounts for poor consumers, or a moneylender that engages in usury, or a charity that runs a heifer pool are engaged in microfinance. Ensuring financial services to poor people is best done by expanding the number of financial institutions available to them, as well as by strengthening the capacity of those institutions. In recent years there has also been increasing emphasis on expanding the diversity of institutions, since different institutions serve different needs.

Some principles that summarize a century and a half of development practice were encapsulated in 2004 by Consultative Group to Assist the Poor (CGAP) and endorsed by the Group of Eight leaders at the G8 Summit on June 10, 2004:[6]

- Poor people need not just loans but also savings, insurance and money transfer services.

- Microfinance must be useful to poor households: helping them raise income, build up assets and/or cushion themselves against external shocks.

- "Microfinance can pay for itself."[10] Subsidies from donors and government are scarce and uncertain, and so to reach large numbers of poor people, microfinance must pay for itself.

- Microfinance means building permanent local institutions.

- Microfinance also means integrating the financial needs of poor people into a country's mainstream financial system.

- "The job of government is to enable financial services, not to provide them."[11]

- "Donor funds should complement private capital, not compete with it."[11]

- "The key bottleneck is the shortage of strong institutions and managers."[11] Donors should focus on capacity building.

- Interest rate ceilings hurt poor people by preventing microfinance institutions from covering their costs, which chokes off the supply of credit.

- Microfinance institutions should measure and disclose their performance – both financially and socially.

Microfinance is considered as a tool for socio-economic development,and can be clearly distinguished from charity. Families who are destitute, or so poor they are unlikely to be able to generate the cash flow required to repay a loan, should be recipients of charity. Others are best served by financial institutions.

Debates at the boundaries

There are several key debates at the boundaries of microfinance.

Practitioners and donors from the charitable side of microfinance frequently argue for restricting microcredit to loans for productive purposes–such as to start or expand a microenterprise. Those from the private-sector side respond that because money is fungible, such a restriction is impossible to enforce, and that in any case it should not be up to rich people to determine how poor people use their money.

Perhaps influenced by traditional Western views about usury, the role of the traditional moneylender has been subject to much criticism, especially in the early stages of modern microfinance. As more poor people gained access to loans from microcredit institutions however, it became apparent that the services of moneylenders continued to be valued. Borrowers were prepared to pay very high interest rates for services like quick loan disbursement, confidentiality and flexible repayment schedules. They did not always see lower interest rates as adequate compensation for the costs of attending meetings, attending training courses to qualify for disbursements or making monthly collateral contributions. They also found it distasteful to be forced to pretend they were borrowing to start a business, when they were often borrowing for other reasons (such as paying for school fees, dealing with health costs or securing the family food supply).[12] The more recent focus on inclusive financial systems (see section below) affords moneylenders more legitimacy, arguing in favour of regulation and efforts to increase competition between them to expand the options available to poor people.

Modern microfinance emerged in the 1970s with a strong orientation towards private-sector solutions. This resulted from evidence that state-owned agricultural development banks in developing countries had been a monumental failure, actually undermining the development goals they were intended to serve (see the compilation edited by Adams, Graham & Von Pischke).[4] Nevertheless public officials in many countries hold a different view, and continue to intervene in microfinance markets.

There has been a long-standing debate over the sharpness of the trade-off between 'outreach' (the ability of a microfinance institution to reach poorer and more remote people) and its 'sustainability' (its ability to cover its operating costs—and possibly also its costs of serving new clients—from its operating revenues).[13] Although it is generally agreed that microfinance practitioners should seek to balance these goals to some extent, there are a wide variety of strategies, ranging from the minimalist profit-orientation of BancoSol in Bolivia to the highly integrated not-for-profit orientation of BRAC in Bangladesh. This is true not only for individual institutions, but also for governments engaged in developing national microfinance systems.

Microfinance experts generally agree that women should be the primary focus of service delivery. Evidence shows that they are less likely to default on their loans than men. Industry data from 2006 for 704 MFIs reaching 52 million borrowers includes MFIs using the solidarity lending methodology (99.3% female clients) and MFIs using individual lending (51% female clients). The delinquency rate for solidarity lending was 0.9% after 30 days (individual lending—3.1%), while 0.3% of loans were written off (individual lending—0.9%).[14] Because operating margins become tighter the smaller the loans delivered, many MFIs consider the risk of lending to men to be too high. This focus on women is questioned sometimes, however. A recent study of microenterpreneurs from Sri Lanka published by the World Bank found that the return on capital for male-owned businesses (half of the sample) averaged 11%, whereas the return for women-owned businesses was 0% or slightly negative.[15]

Microfinancial services may be needed everywhere, including the developed world.[citation needed] However, in developed economies intense competition within the financial sector, combined with a diverse mix of different types of financial institutions with different missions, ensures that most people have access to some financial services.[citation needed] Efforts to transfer microfinance innovations such as solidarity lending from developing countries to developed ones have met with little success.[16]

Financial needs of poor people

Financial needs and financial services.

Financial needs and financial services.In developing economies and particularly in the rural areas, many activities that would be classified in the developed world as financial are not monetized: that is, money is not used to carry them out. Almost by definition, poor people have very little money. But circumstances often arise in their lives in which they need money or the things money can buy.

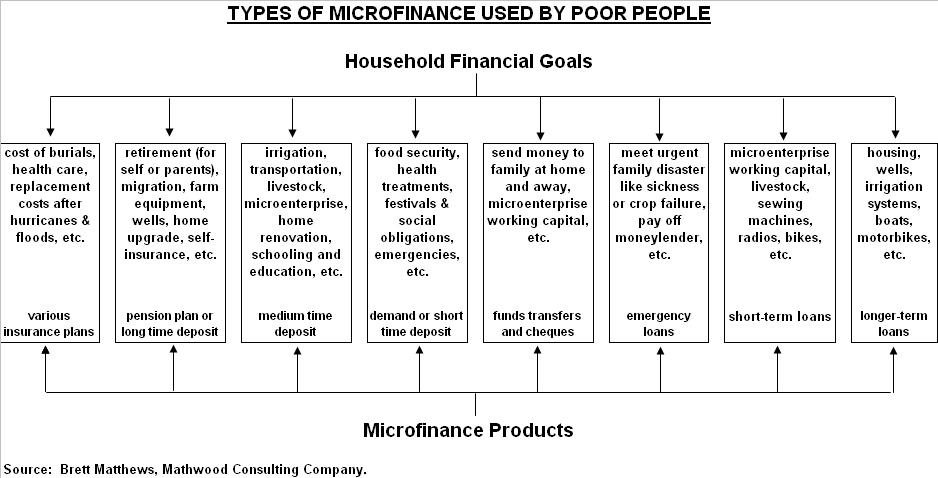

In Stuart Rutherford’s recent book The Poor and Their Money, he cites several types of needs:[17]

- Lifecycle Needs: such as weddings, funerals, childbirth, education, homebuilding, widowhood, old age.

- Personal Emergencies: such as sickness, injury, unemployment, theft, harassment or death.

- Disasters: such as fires, floods, cyclones and man-made events like war or bulldozing of dwellings.

- Investment Opportunities: expanding a business, buying land or equipment, improving housing, securing a job (which often requires paying a large bribe), etc.

Poor people find creative and often collaborative ways to meet these needs, primarily through creating and exchanging different forms of non-cash value. Common substitutes for cash vary from country to country but typically include livestock, grains, jewelry, and precious metals.

As Marguerite Robinson describes in The Microfinance Revolution, the 1980s demonstrated that "microfinance could provide large-scale outreach profitably," and in the 1990s, "microfinance began to develop as an industry" (2001, p. 54). In the 2000s, the microfinance industry's objective is to satisfy the unmet demand on a much larger scale, and to play a role in reducing poverty. While much progress has been made in developing a viable, commercial microfinance sector in the last few decades, several issues remain that need to be addressed before the industry will be able to satisfy massive worldwide demand. The obstacles or challenges to building a sound commercial microfinance industry include:

- Inappropriate donor subsidies

- Poor regulation and supervision of deposit-taking MFIs

- Few MFIs that meet the needs for savings, remittances or insurance

- Limited management capacity in MFIs

- Institutional inefficiencies

- Need for more dissemination and adoption of rural, agricultural microfinance methodologies

Ways in which poor people manage their money

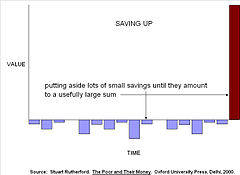

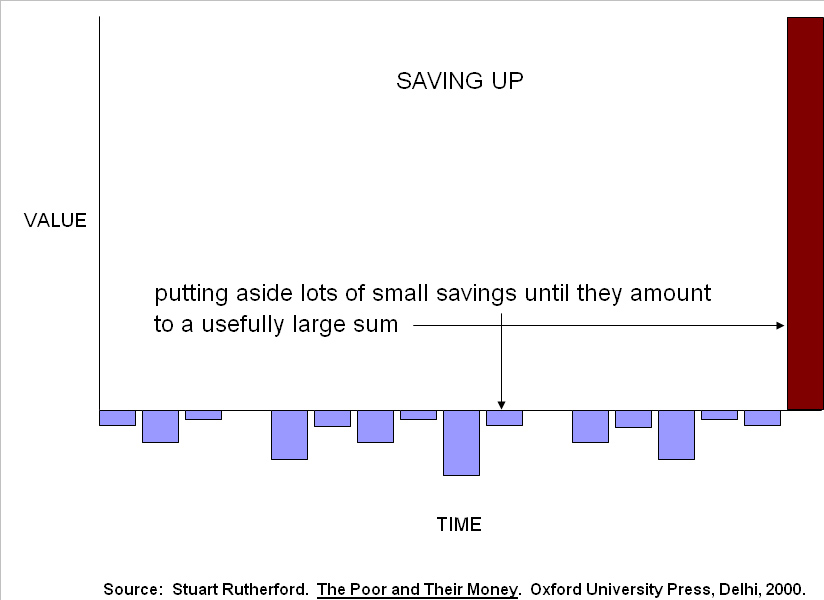

Saving up

Saving upRutherford argues that the basic problem poor people as money managers face is to gather a 'usefully large' amount of money. Building a new home may involve saving and protecting diverse building materials for years until enough are available to proceed with construction. Children’s schooling may be funded by buying chickens and raising them for sale as needed for expenses, uniforms, bribes, etc. Because all the value is accumulated before it is needed, this money management strategy is referred to as 'saving up'.[citation needed]

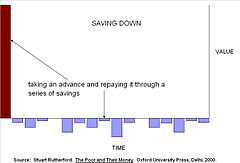

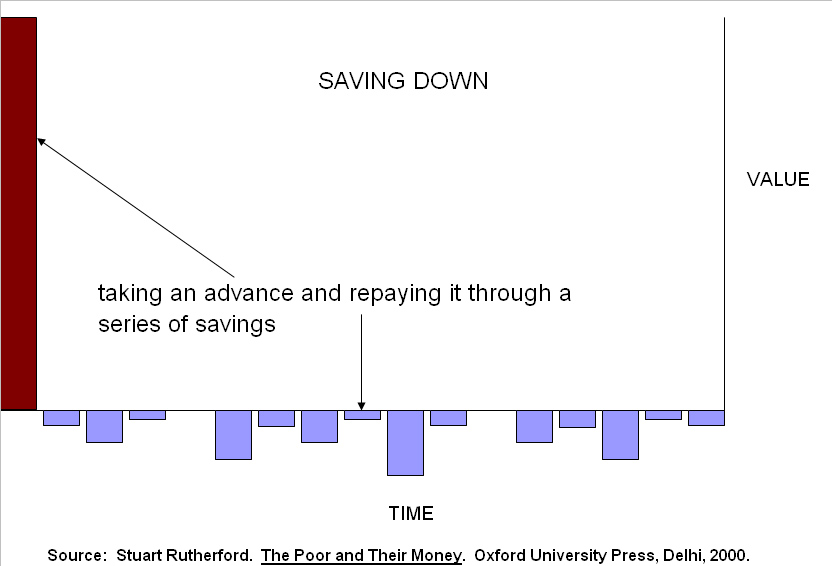

Often people don't have enough money when they face a need, so they borrow. A poor family might borrow from relatives to buy land, from a moneylender to buy rice, or from a microfinance institution to buy a sewing machine. Since these loans must be repaid by saving after the cost is incurred, Rutherford calls this 'saving down'. Rutherford's point is that microcredit is addressing only half the problem, and arguably the less important half: poor people borrow to help them save and accumulate assets. Microcredit institutions should fund their loans through savings accounts that help poor people manage their myriad risks.[citation needed]

Saving down

Saving downMost needs are met through mix of saving and credit. A benchmark impact assessment of Grameen Bank and two other large microfinance institutions in Bangladesh found that for every $1 they were lending to clients to finance rural non-farm micro-enterprise, about $2.50 came from other sources, mostly their clients' savings.[18] This parallels the experience in the West, in which family businesses are funded mostly from savings, especially during start-up.

Recent studies have also shown that informal methods of saving are unsafe. For example a study by Wright and Mutesasira in Uganda concluded that "those with no option but to save in the informal sector are almost bound to lose some money – probably around one quarter of what they save there."[19]

The work of Rutherford, Wright and others has caused practitioners to reconsider a key aspect of the microcredit paradigm: that poor people get out of poverty by borrowing, building microenterprises and increasing their income. The new paradigm places more attention on the efforts of poor people to reduce their many vulnerabilities by keeping more of what they earn and building up their assets. While they need loans, they may find it as useful to borrow for consumption as for microenterprise. A safe, flexible place to save money and withdraw it when needed is also essential for managing household and family risk.[citation needed]

Current scale of microfinance operations

No systematic effort to map the distribution of microfinance has yet been undertaken. A useful recent benchmark was established by an analysis of 'alternative financial institutions' in the developing world in 2004.[20] The authors counted approximately 665 million client accounts at over 3,000 institutions that are serving people who are poorer than those served by the commercial banks. Of these accounts, 120 million were with institutions normally understood to practice microfinance. Reflecting the diverse historical roots of the movement, however, they also included postal savings banks (318 million accounts), state agricultural and development banks (172 million accounts), financial cooperatives and credit unions (35 million accounts) and specialized rural banks (19 million accounts).

Regionally the highest concentration of these accounts was in India (188 million accounts representing 18% of the total national population). The lowest concentrations were in Latin American and the Caribbean (14 million accounts representing 3% of the total population) and Africa (27 million accounts representing 4% of the total population, with the highest rate of penetration in West Africa, and the highest growth rate in Eastern and Southern Africa [21] ). Considering that most bank clients in the developed world need several active accounts to keep their affairs in order, these figures indicate that the task the microfinance movement has set for itself is still very far from finished.

By type of service "savings accounts in alternative finance institutions outnumber loans by about four to one. This is a worldwide pattern that does not vary much by region."[22]

An important source of detailed data on selected microfinance institutions is the MicroBanking Bulletin, which is published by Microfinance Information Exchange. At the end of 2009 it was tracking 1,084 MFIs that were serving 74 million borrowers ($38 billion in outstanding loans) and 67 million savers ($23 billion in deposits).[23]

As yet there are no studies that indicate the scale or distribution of 'informal' microfinance organizations like ROSCA's and informal associations that help people manage costs like weddings, funerals and sickness. Numerous case studies have been published however, indicating that these organizations, which are generally designed and managed by poor people themselves with little outside help, operate in most countries in the developing world.[24]

Help can come in the form of more and better qualified staff, thus higher education is needed for microfinance institutions. This has begun in some universities, as Oliver Schmidt describes. Mind the management gap

"Inclusive financial systems"

The microcredit era that began in the 1970s has lost its momentum, to be replaced by a 'financial systems' approach. While microcredit achieved a great deal, especially in urban and near-urban areas and with entrepreneurial families, its progress in delivering financial services in less densely populated rural areas has been slow.

The new financial systems approach pragmatically acknowledges the richness of centuries of microfinance history and the immense diversity of institutions serving poor people in developing world today. It is also rooted in an increasing awareness of diversity of the financial service needs of the world’s poorest people, and the diverse settings in which they live and work.

Brigit Helms in her book 'Access for All: Building Inclusive Financial Systems', distinguishes between four general categories of microfinance providers, and argues for a pro-active strategy of engagement with all of them to help them achieve the goals of the microfinance movement.[25]

- Informal financial service providers

- These include moneylenders, pawnbrokers, savings collectors, money-guards, ROSCAs, ASCAs and input supply shops. Because they know each other well and live in the same community, they understand each other’s financial circumstances and can offer very flexible, convenient and fast services. These services can also be costly and the choice of financial products limited and very short-term. Informal services that involve savings are also risky; many people lose their money.

- Member-owned organizations

- These include self-help groups, credit unions, and a variety of hybrid organizations like 'financial service associations' and CVECAs. Like their informal cousins, they are generally small and local, which means they have access to good knowledge about each others' financial circumstances and can offer convenience and flexibility. Since they are managed by poor people, their costs of operation are low. However, these providers may have little financial skill and can run into trouble when the economy turns down or their operations become too complex. Unless they are effectively regulated and supervised, they can be 'captured' by one or two influential leaders, and the members can lose their money.

- NGOs

- The Microcredit Summit Campaign counted 3,316 of these MFIs and NGOs lending to about 133 million clients by the end of 2006.[26] Led by Grameen Bank and BRAC in Bangladesh, Prodem in Bolivia, and FINCA International, headquartered in Washington, DC, these NGOs have spread around the developing world in the past three decades; others, like the Gamelan Council, address larger regions. They have proven very innovative, pioneering banking techniques like solidarity lending, village banking and mobile banking that have overcome barriers to serving poor populations. However, with boards that don’t necessarily represent either their capital or their customers, their governance structures can be fragile, and they can become overly dependent on external donors.

- Formal financial institutions

- In addition to commercial banks, these include state banks, agricultural development banks, savings banks, rural banks and non-bank financial institutions. They are regulated and supervised, offer a wider range of financial services, and control a branch network that can extend across the country and internationally. However, they have proved reluctant to adopt social missions, and due to their high costs of operation, often can't deliver services to poor or remote populations. The increasing use of alternative data in credit scoring, such as trade credit is increasing commercial banks' interest in microfinance.[27]

With appropriate regulation and supervision, each of these institutional types can bring leverage to solving the microfinance problem. For example, efforts are being made to link self-help groups to commercial banks, to network member-owned organizations together to achieve economies of scale and scope, and to support efforts by commercial banks to 'down-scale' by integrating mobile banking and e-payment technologies into their extensive branch networks.

Microcredit and the web

Due to the unbalanced emphasis on credit at the expense of microsavings, as well as a desire to link Western investors to the sector, peer-to-peer platforms have developed to expand the availability of microcredit through individual lenders in the developed world. The volume channeled through Kiva's peer-to-peer platform is about $100 million as of November 2009 (Kiva facilitates approximately $5M in loans each month). In comparison, the needs for microcredit are estimated about 250 bn USD as of end 2006.[28] Most experts agree that these funds must be sourced locally in countries that are originating microcredit, to reduce transaction costs and exchange rate risks.

There have been problems with disclosure on peer-to-peer sites, with some reporting interest rates of borrowers using the flat rate methodology instead of the familiar banking Annual Percentage Rate.[29] The use of flat rates, which has been outlawed among regulated financial institutions in developed countries, can confuse individual lenders into believing their borrower is paying a lower interest rate than, in fact, they are.[citation needed]

Evidence for reducing poverty

Research on the effectiveness of microfinance as a tool for economic development remains mixed, in part owing to the difficulty in monitoring and measuring this impact.[30] At the 2008 Innovations for Poverty Action/Financial Access Initiative Microfinance Research conference, economist Jonathan Morduch of New York University noted there are only one or two methodologically sound studies of microfinance's impact.[31]. Grameen Foundation has released two papers summarizing the state of research on the impact of microfinance on poverty: "Measuring the Impact of Microfinance, Taking Stock of What We Know" by Nathanael Goldberg[32] (now with Innovations for Poverty Action) and an update, "Measuring the Impact of Microfinance: Taking Another Look" by Professor Kathleen Odell. These two papers identify scores of findings indicating positive impact in research conducted over the last twenty years, as well as some findings that suggest limited or negative impact in some cases.

The BBC Business Weekly program reported that much of the supposed benefits associated with microfinance, are perhaps not as compelling as once thought. In a radio interview with Professor Dean Karlan of Yale University, a point was raised concerning a comparison between two groups: one African, financed through microcredit and one control group in the Philippines. The results of this study suggest that many of the benefits from microcredit are in fact loaned to people with existing business, and not to those seeking to establish new businesses. Many of those receiving microcredit also used the loans to supplement the family income. The income that went up in business was true only for men, and not for women. This is striking because one of the supposed major beneficiaries of microfinance is supposed to be targeted at women. Professor Karlan's conclusion was that whilst microcredit is not necessarily bad and can generate some positive benefits, despite some lenders charging interest rates between 40-60%, it isn't the panacea that it is purported to be. He advocates rather than focusing strictly on microcredit, also giving citizens in poor countries access to rudimentary and cheap savings accounts.[33]

To further the point stated by Prof Karlan, microfinancing begets the general tendency of a small business initially supported on credit to gain profits with time and generate micro savings. In his latest study, the famous two time pulitzer prize winner, Nicholas Donabet Kristof states that there is no evidence of any negative influence of micro financing but countless examples of people now looking at the bigger picture and saving for better things have surfaced. The example of BancoSol(Bolivia), where the number of savers has grown to twice as much as the number of borrowers, further strengthens his theory.[34][35]

Sociologist Jonathan H. Westover, Ph.D. found that much of the evidence on the effectiveness of microfinance for alleviating poverty is based in anecdotal reports or case studies. He initially found over 100 articles on the subject, but included only the 6 which used enough quantitative data to be representative, and none of which employed rigorous methods such as randomized control trials similar to those reported by Innovations for Poverty Action and the M.I.T. Jameel Poverty Action Lab. One of these studies found that microfinance reduced poverty. Two others were unable to conclude that microfinance reduced poverty, although they attributed some positive effects to the program. Other studies concluded similarly, with surveys finding that a majority of participants feel better about finances with some feeling worse.[36]

Microfinance and social interventions

There are currently a few social interventions that have been combined with micro financing to increase awareness of HIV/AIDS. Such interventions like the "Intervention with Microfinance for AIDS and Gender Equity" (IMAGE) which incorporates microfinancing with "The Sisters-for-Life" program a participatory program that educates on different gender roles, gender-based violence, and HIV/AIDS infections to strengthen the communication skills and leadership of women [37] "The Sisters-for-Life" program has two phases where phase one consists of ten one-hour training programs with a facilitator with phase two consisting of identifying a leader amongst the group, train them further, and allow them to implement an Action Plan to their respective centres.

Microfinance has also been combined with business education and with other packages of health interventions.[38] A project undertaken in Peru by Innovations for Poverty Action found that those borrowers randomly selected to receive financial training as part of their borrowing group meetings had higher profits, although there was not a reduction in "the proportion who reported having problems in their business".[39]

Other criticisms

See also: Microcredit: CriticismMost criticisms of microfinance have actually been criticisms of microcredit, delivered in the absence of other microfinance services such as savings, remittances, payments and insurance.

For example, there has been much criticism of the high interest rates charged to borrowers. The real average portfolio yield cited by the sample of 704 microfinance institutions that voluntarily submitted reports to the MicroBanking Bulletin in 2006 was 22.3% annually. However, annual rates charged to clients are higher, as they also include local inflation and the bad debt expenses of the microfinance institution.[40] Muhammad Yunus has recently made much of this point, and in his latest book[41] argues that microfinance institutions that charge more than 15% above their long-term operating costs should face penalties.

Milford Bateman, the author of Why Doesn't Microfinance Work?, argues that microcredit offers only an "illusion of poverty reduction". "As in any lottery or game of chance, a few in poverty do manage to establish microenterprises that produce a decent living," he argues, but "these isolated and often temporary positives are swamped by the largely overlooked negatives." Bateman concludes that "The international development community is now faced with the reality that, overall, microfinance has been a development policy blunder of quite historic proportions."[42] Here Bateman, like many writers, confuses microfinance as a broad sector with microcredit, a single microfinance intervention (see delineation above).

The role of donors has also been questioned. The Consultative Group to Assist the Poor (CGAP) recently commented that "a large proportion of the money they spend is not effective, either because it gets hung up in unsuccessful and often complicated funding mechanisms (for example, a government apex facility), or it goes to partners that are not held accountable for performance. In some cases, poorly conceived programs have retarded the development of inclusive financial systems by distorting markets and displacing domestic commercial initiatives with cheap or free money."[43]

There has also been criticism of microlenders for not taking more responsibility for the working conditions of poor households, particularly when borrowers become quasi-wage labourers, selling crafts or agricultural produce through an organization controlled by the MFI. The desire of MFIs to help their borrower diversify and increase their incomes has sparked this type of relationship in several countries, most notably Bangladesh, where hundreds of thousands of borrowers effectively work as wage labourers for the marketing subsidiaries of Grameen Bank or BRAC. Critics maintain that there are few if any rules or standards in these cases governing working hours, holidays, working conditions, safety or child labour, and few inspection regimes to correct abuses.[44] Some of these concerns have been taken up by unions and socially responsible investment advocates.

For example, BusinessWeek reported that some Mexicans are stumbling with terms of newly available funding.[45][46]

Other criticism was raised by the IPO (Initial Public Offering) of a Mexican MFI Banco Compartamos in 2007. As the company put its shares on Mexican Stock Exchange it was able to generate very high profits that were achieved by rising interest rates on their micro-loans that at some point reached 86% per year.[47] In July 2010 India's biggest MFI, SKS Microfinance also went public. In both instances Muhammad Yunus publicly stated his disagreement, saying that the poor should be the only beneficiaries of microfinance.[48][49]

Microcredit has been blamed for many suicides in India: aggressive lending by microcredit companies in Andra Pradesh is said to have resulted in over 80 deaths in 2010.[50]

Some problems with microcredit are mistakenly alleged in The Micro Debt, a film by the Danish journalist Tom Heinemann.[51] After a thorough investigation in December 2010 by the Norwegian Foreign Ministry, the alleged problems have been proven to be false and no further actions against the Grameen Bank and its founder, Muhammad Yunnis, have been taken.[52]

The documentary by Heinemann also looks at the effectiveness of Grameen Bank and alleges that it has little impact on poverty by highlighting the purported continued poverty of Sufiya Begum, the original loan recipient of Grameen, in Jobra Village. This allegation is disputed, since documentary maker Gayle Ferraro found the woman alive and well, confirming the original Grameen story.[53]

Bibliography

- Adams, Dale W., Douglas H. Graham & J. D. Von Pischke (eds.). Undermining Rural Development with Cheap Credit. Westview Press, Boulder & London, 1984.

- de Aghion, Beatriz Armendáriz & Jonathan Morduch. The Economics of Microfinance, The MIT Press, Cambridge, Massachusetts, 2005.

- Branch, Brian & Janette Klaehn. Striking the Balance in Microfinance: A Practical Guide to Mobilizing Savings. PACT Publications, Washington, 2002.

- Christen, Robert Peck, Jayadeva, Veena & Richard Rosenberg. Financial Institutions with a Double Bottom Line. Consultative Group to Assist the Poor, Washington 2004.

- Dichter, Thomas and Malcolm Harper (eds). What’s Wrong with Microfinance? Practical Action, 2007.

- Dowla, Asif & Dipal Barua. The Poor Always Pay Back: The Grameen II Story. Kumarian Press Inc., Bloomfield, Connecticut, 2006.

- Gibbons, David. The Grameen Reader. Grameen Bank, Dhaka, 1992.

- Helms, Brigit. Access for All: Building Inclusive Financial Systems. Consultative Group to Assist the Poor, Washington, 2006.

- Hirschland, Madeline (ed.) Savings Services for the Poor: An Operational Guide. Kumarian Press Inc., Bloomfield CT, 2005.

- Khandker, Shahidur R. Fighting Poverty with Microcredit, Bangladesh edition, The University Press Ltd, Dhaka, 1999.

- Ledgerwood, Joanna and Victoria White. Transforming Microfinance Institutions: Providing Full Financial Services to the Poor. World Bank, 2006.

- Mas, Ignacio and Kabir Kumar. Banking on mobiles: why, how and for whom? CGAP Focus Note #48, July, 2008.

- Raiffeisen, FW (translated from the German by Konrad Engelmann). The Credit Unions. The Raiffeisen Printing & Publishing Company, Neuwied on the Rhine, Germany, 1970.

- Rutherford, Stuart. The Poor and Their Money. Oxford University Press, Delhi, 2000.

- Wolff, Henry W. People’s Banks: A Record of Social and Economic Success. P.S. King & Son, London, 1910.

- Sapovadia, Vrajlal K., Micro Finance: The Pillars of a Tool to Socio-Economic Development. Development Gateway, 2006.

- Maimbo, Samuel Munzele & Dilip Ratha (eds.) Remittances: Development Impact and Future Prospects. The World Bank, 2005.

- Wright, Graham A.N. Microfinance Systems: Designing Quality Financial Services for the Poor. The University Press, Dhaka, 2000.

- United Nations Department of Economic Affairs and United Nations Capital Development Fund. Building Inclusive Financial Sectors for Development. United Nations, New York, 2006.

- Yunus, Muhammad. Creating a World Without Poverty: Social Business and the Future of Capitalism. PublicAffairs, New York, 2008.

See also

- Alternative data

- Bank

- Credit union

- Crowd funding

- Microcredit

- Microfinance in Tanzania

- Microinsurance

- Microfinance organizations

- Opportunity finance

- Pawnbroker

- ROSCA

- Savings bank

- Microfinance Focus

Notes

- ^ Robert Peck Christen, Richard Rosenberg & Veena Jayadeva. Financial institutions with a double-bottom line: implications for the future of microfinance. CGAP Occasional Paper, July 2004, pp. 2-3.

- ^ Feigenberg, Benjamin; Erica M. Field, Rohini Pande. Building Social Capital Through MicroFinance. NBER Working Paper No. 16018. http://www.nber.org/papers/w16018. Retrieved 10 March 2011.

- ^ Hernando de Soto. The Other Path: The Invisible Revolution in the Third World. Harper & Row Publishers, New York, 1989, p. 162.

- ^ a b Adams, Dale W., Douglas H. Graham & J. D. Von Pischke (eds.). Undermining Rural Development with Cheap Credit. Westview Press, Boulder & London, 1984.

- ^ Marguerite Robinson. The Microfinance Revolution: Sustainable Finance for the Poor World Bank, Washington, 2001, pp. 199-215.

- ^ a b Helms, Brigit (2006). Access for All: Building Inclusive Financial Systems. Washington, D.C.: The World Bank. ISBN 0821363603.

- ^ a b Microfinance: An emerging investment opportunity. Deutsche Bank Dec 2007

- ^ "Microfinance: Building Domestic Markets in Developing Countries". Citigroup.com. http://www.citigroup.com/citi/microfinance/data/initiatives.pdf. Retrieved 2011-03-25.

- ^ http://www.inwent.org/ez/articles/184683/index.en.shtml

- ^ Helms (2006), p. xi

- ^ a b c Helms (2006), p. xii

- ^ Robert Peck Christen. What microenterprise credit programs can learn the moneylenders, Accion International, 1989

- ^ See for example Adrian Gonzalez & Richard Rosenberg. The state of microfinance: outreach, profitability and poverty, Consultative Group to Assist the Poor, 2006.

- ^ Microfinance Information Exchange, Inc. (2007-08-01). "MicroBanking Bulletin Issue #15, Autumn, 2007, pp. 46,49". Microfinance Information Exchange, Inc.. http://www.themix.org/microbanking-bulletin/mbb-issue-no-15-autumn-2007. Retrieved 2010-01-15.

- ^ McKenzie, David (2008-10-17). "Comments Made at IPA/FAI Microfinance Conference Oct. 17 2008". Philanthropy Action. http://www.philanthropyaction.com/nc/what_is_it_about_women/. Retrieved 2008-10-17.

- ^ See for example Cheryl Frankiewicz Calmeadow Metrofund: a Canadian experiment in sustainable microfinance, Calmeadow Foundation, 2001.

- ^ Stuart Rutherford. The Poor and Their Money. Oxford University Press, New Delhi, 2000, p. 4. isbn =019565790X

- ^ Khandker, Shahidur R. Fighting Poverty with Microcredit, Bangladesh edition, The University Press Ltd, Dhaka, 1999, p. 78.

- ^ Graham A.N. Wright and Leonard Mutesasira. The relative risks to the savings of poor people, Micro-Save Africa, January, 2001.

- ^ Robert Peck Christen, Richard Rosenberg & Veena Jayadeva. Financial institutions with a double-bottom line: implications for the future of microfinance. CGAP Occasional Paper, July 2004.

- ^ MFW4A - Microfinance (2010-11-05). "MFW4A - Microfinance". http://www.mfw4a.org/access-to-finance/microfinance.html.

- ^ Christen, Rosenberg & Jayadeva. Financial institutions with a double-bottom line, pp. 5-6

- ^ Microfinance Information Exchange, Inc. (2009-12-01). "MicroBanking Bulletin Issue #19, December, 2009, pp. 49". Microfinance Information Exchange, Inc.. http://www.themix.org/microbanking-bulletin/mbb-issue-no-19-december-2009.

- ^ See for example Joachim de Weerdt, Stefan Dercon, Tessa Bold and Alula Pankhurst, Membership-based indigenous insurance associations in Ethiopia and Tanzania For other cases see ROSCA.

- ^ Brigit Helms. Access for All: Building Inclusive Financial Systems. CGAP/World Bank, Washington, 2006, pp. 35-57.

- ^ "''State of the Microcredit Summit Campaign Report 2007'', Microcredit Summit Campaign, Washington, 2007.". Microcreditsummit.org. 2006-12-31. http://www.microcreditsummit.org/pubs/reports/socr/2007.html. Retrieved 2011-03-25.

- ^ Turner, Michael, Robin Varghese, et al. Information Sharing and SMME Financing in South Africa, Political and Economic Research Council (PERC), p58.

- ^ Microfinance: An emerging investment opportunity. Deutsche Bank Research. December 19, 2007.

- ^ Waterfield, Chuck. Why We Need Transparent Pricing in Microfinance. MicroFinance Transparency. 11 November 2008.

- ^ Littlefield, Elizabeth; Morduch, Jonathan and Hashemi, Syed (2003-01-01). "Is Microfinance an Effective Strategy to Reach the Millennium Development Goals?" (PDF). FocusNote (Consultative Group to Assist the Poor) (24). Archived from the original on 2007-02-03. http://web.archive.org/web/20070203045104/http://www.cgap.org/docs/FocusNote_24.pdf. Retrieved 2007-03-27.

- ^ Morduch, Jonathan (2008-10-17). "Comments Made at IPA/FAI Microfinance Conference Oct. 17 2008". Philanthropy Action. http://www.philanthropyaction.com/nc/cutting_edge_research_on_microfinance/. Retrieved 2008-10-17.

- ^ "Measuring the Impact of Microfinance, Taking Stock of What We Know". Grameen Bank. 2005. http://www.givewell.org/files/Cause1-2/Independent%20research%20on%20microfinance/GFUSA-MicrofinanceImpactWhitepaper-1.pdf. Retrieved 2011-10-25.

- ^ "BBC.co.uk". BBC.co.uk. http://www.bbc.co.uk/programmes/p003s71s. Retrieved 2011-03-25.

- ^ Kristof, Nicholas (2009-12-28). "The Role of Microfinance". The New York Times. http://kristof.blogs.nytimes.com/2009/12/28/the-role-of-microfinance/.

- ^ "Reply to Nicholas Kristof: Microcredit, microsavings? Microfinance. «". Centerforfinancialinclusionblog.wordpress.com. 2010-01-20. http://centerforfinancialinclusionblog.wordpress.com/2010/01/05/reply-to-nicholas-kristof-microcredit-microsavings-microfinance/. Retrieved 2011-03-25.

- ^ Westover J. (2008). The Record of Microfinance: The Effectiveness/Ineffectiveness of Microfinance Programs as a Means of Alleviating Poverty. Electronic Journal of Sociology.

- ^ Kim, J.C., Watts, C. H., Hargreaves, J. R., Ndhlovu, L. X., Phetla, G., Morison, L. A., et al. (2007). Understanding the impact of a microfinance-based intervention of women's empowerment and the reduction of intimate partner violence in South Africa. American Journal of Public Health.

- ^ Stephen C. Smith, "Village Banking and Maternal and Child Health: Evidence from Ecuador and Honduras," World Development, 30, 4, 707 723, April 2002

- ^ Karlan D, Valdivia M. (2009). Teaching Entrepreneurship: Impact of Business Training on Microfinance Clients and Institutions. Forthcoming March 2010, Review of Economics and Statistics.

- ^ Microfinance Information Exchange, Inc. (2007-08-01). "MicroBanking Bulletin Issue #15, Autumn, 2007, pp. 48". Microfinance Information Exchange, Inc.. http://www.themix.org/microbanking-bulletin/mbb-issue-no-15-autumn-2007.

- ^ Muhammad Yunus and Karl Weber. Creating a World Without Poverty: Social Business and the Future of Capitalism. PublicAffairs, New York, 2007

- ^ "The illusion of poverty reduction". Red Pepper magazine. 2010-09-01. http://www.redpepper.org.uk/the-illusion-of-poverty-reduction.

- ^ Brigit Helms. Access for All: Building Inclusive Financial Systems. CGAP/World Bank, Washington, 2006, p. 97.

- ^ Farooque Chowdhury. The metamorphosis of the micro-credit debtor New Age, June 24, 2007.

- ^ Epstein, Keith (2007-12-13). "''Businessweek'', The Ugly Side of Microlending". Businessweek.com. http://www.businessweek.com/magazine/content/07_52/b4064038915009.htm. Retrieved 2011-03-25.

- ^ "Mexican microlending bank surges in market debut". Reuters.com. http://www.reuters.com/article/newIssuesNews/idUSN2025193920070420. Retrieved 2011-03-25.

- ^ CGAP, "Banco Compartamos: Interest Rates, Profits, and an Initial Public Offering" http://www.cgap.org/p/site/c/template.rc/1.26.4905/

- ^ Businessweek, "Online Extra: Yunus Blasts Compartamos" http://www.businessweek.com/magazine/content/07_52/b4064045920958.htm

- ^ ABCNews, SKS Launches India's First Microfinance IPO http://abcnews.go.com/Business/wireStory?id=11270209

- ^ "India's micro-finance suicide epidemic". BBC News. 2010-12-16. http://www.bbc.co.uk/news/world-south-asia-11997571.

- ^ "Tom Heinemann: "Fanget i Mikrogæld"". Dr.dk. http://www.dr.dk/Nyheder/Udland/2010/12/01/170646.htm. Retrieved 2011-03-25.

- ^ "Grameen: Norway gives all-clear to Bangladesh bank". BBC News. BBC. http://www.bbc.co.uk/news/world-south-asia-11947902. Retrieved 17 September 2011.

- ^ "David Roodman's Microfinance Open Book Blog". Blogs.cgdev.org. http://blogs.cgdev.org/open_book/2011/02/being-crossfire.php. Retrieved 2011-03-25.

External links

Categories:

Wikimedia Foundation. 2010.