- Management control system

-

A management control systems (MCS) is a system which gathers and uses information to evaluate the performance of different organizational resources like human, physical, financial and also the organization as a whole considering the organizational strategies. Finally, MCS influences the behavior of organizational resources to implement organizational strategies. MCS might be formal or informal. The term ‘management control’ was given of its current connotations by Robert N. Anthony (Otley, 1994). [1]

Robert N. Anthony (2007) defined Management Control is the process by which managers influence other members of the organization to implement the organization’s strategies. Management control systems are tools to aid management for steering an organization toward its strategic objectives and competitive advantage. Management controls are only one of the tools which managers use in implementing desired strategies. However strategies get implemented through management controls, organizational structure, human resources management and culture.[2] Anthony & Young (1999) showed management control system as a black box. The term black box is used to describe an operation whose exact nature cannot be observed. MCS involves the behavior of managers and these behaviors cannot be expressed by equations. Anthony & Young (1999) showed that management accounting has three major subdivisions: full cost accounting, differential accounting and management control or responsibility accounting. [3]

According to Horngren et al. (2005), management control system is an integrated technique for collecting and using information to motivate employee behavior and to evaluate performance. [4]. According to Simons (1995), Management Control Systems are the formal, information-based routines and procedures managers use to maintain or alter patterns in organizational activities [5]

Chenhall (2003) mentioned that the terms management accounting (MA), management accounting systems (MAS), management control systems (MCS), and organizational controls (OC) are sometimes used interchangeably. In this case, MA refers to a collection of practices such as budgeting or product costing. But MAS refers to the systematic use of MA to achieve some goal and MCS is a broader term that encompasses MAS and also includes other controls such as personal or clan controls. Finally OC is sometimes used to refer to controls built into activities and processes such as statistical quality control, just-in-time management.[6]

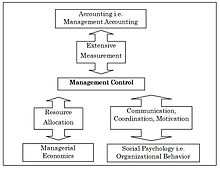

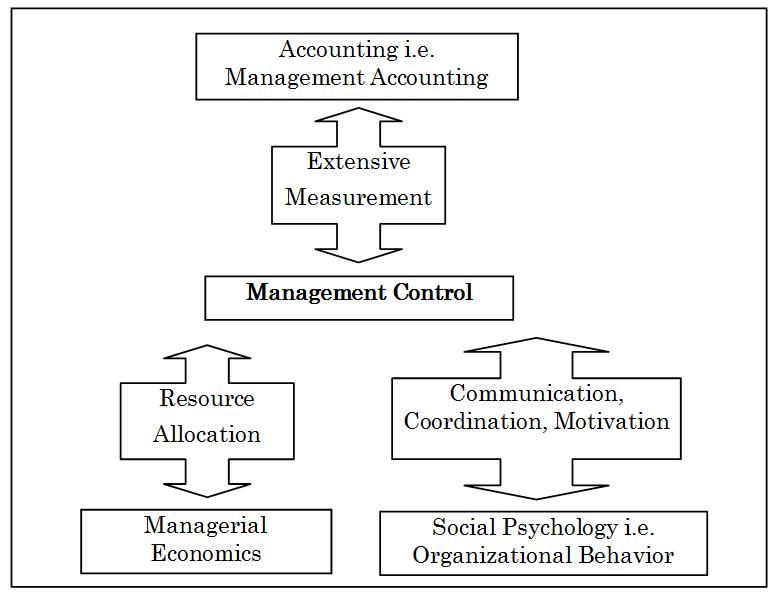

According to Maciariello et al. (1994), management control is concerned with coordination, resource allocation, motivation, and performance measurement. The practice of management control and the design of management control systems draws upon a number of academic disciplines. Management control involves extensive measurement and it is therefore related to and requires contributions from accounting especially management accounting. Second, it involves resource allocation decisions and is therefore related to and requires contribution from economics especially managerial economics. Third, it involves communication, and motivation which means it is related to and must draw contributions from social psychology especially organizational behavior (see Exhibit#1).[7] Exhibit#1: Management control as an interdisciplinary subject

Exhibit#1: Management control as an interdisciplinary subject

Management control systems use many techniques such as- Balanced scorecard

- Total quality management (TQM)

- Kaizen (Continuous Improvement)

- Activity-based costing

- Target costing

- Benchmarking and Benchtrending

- JIT

- Budgeting

- Capital budgeting

- Program management techniques, etc.

See also

- Management

- Control (management)

- Health management system

References

- ^ Otley, D., 1994. Management control in contemporary organizations: towards a wider framework, Management Accounting Research, 5, 289-299.

- ^ Anthony, R. and Govindarajan, V., 2007. Management Control Systems, Chicago, Mc-Graw-Hill IRWIN.

- ^ Anthony, R. and Young, D., 1999. Management control in nonprofit organizations, Boston, Irwin McGraw-Hill.

- ^ Horngren, C., Sundem, G. and Stratton, W., 2005. Introduction to Management Accounting, New Jersey, Pearson.

- ^ Simons, 1995, Levers of Control, Boston: Harvard Business School Press, p. 5

- ^ Chenhall, R., 2003. Management control system design within its organizational context: Findings from contingency-based research and directions for the future, Accounting, Organizations and Society, 28(2-3), 127-168.

- ^ Maciariello, J. and Kirby, C., 1994. Management Control Systems - Using Adaptive Systems to Attain Control, New Jersey, Prentice Hall.

Categories:

Wikimedia Foundation. 2010.