- Credit score (United States)

-

A credit score in the United States is a number representing the creditworthiness of a person, the likelihood that person will pay his or her debts.

Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers. Widespread use of credit scores has made credit more widely available and cheaper for consumers.[1][2]

Contents

Credit scoring models

FICO score

The best-known and most widely used credit score model in the United States, the FICO score is calculated statistically, with information from a consumer's credit files. The letters stand for Fair Isaac Corporation. [3].

It provides a snapshot of risk that banks and other institutions use to help make lending decisions. Applicants with higher FICO scores may be offered better interest rates on mortgages or automobile loans.

Makeup of the FICO score

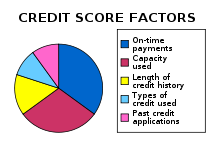

The approximate makeup of the FICO score used by U.S. lenders

The approximate makeup of the FICO score used by U.S. lenders

Credit scores are designed to measure the risk of default by taking into account various factors in a person's financial history. Although the exact formulas for calculating credit scores are secret, FICO has disclosed the following components:[4][5]

- 35%: Payment history—Late payments on bills, such as a mortgage, credit card or automobile loan, can cause a FICO score to drop. Bills paid on time will improve a FICO score.[6]

- 30%: Credit utilization—The ratio of current revolving debt (such as credit card balances) to the total available revolving credit or credit limit. FICO scores can be improved by paying off debt and lowering the credit utilization ratio.[7] Alternatively, applications for and receiving the credit limit increase will also drive down the utilization ratio. The closing of existing revolving accounts will typically adversely affect this ratio and therefore have a negative impact on a FICO score.

- 15%: Length of credit history—As a credit history ages it can have a positive impact on its FICO score.[8]

- 10%: Types of credit used (installment, revolving, consumer finance, mortgage)—Consumers can benefit by having a history of managing different types of credit.[9]

- 10%: Recent searches for credit—Credit inquiries, which occur when consumers are seeking new credit, can hurt scores. Individuals shopping for a mortgage or auto loan over a short period will likely not experience a decrease in their scores as a result of these types of inquiries, however.[10] While all credit inquiries are recorded and displayed on credit reports for a period of time, credit inquiries that were made by the owner (self-check), by an employer (for employee verification) or by companies initiating pre-screened offers of credit or insurance do not have any impact on a credit score.

Getting a higher credit limit can help your credit score. The higher the credit limit on the credit card, the lower the utilization ratio average for all of your credit card accounts. The utilization ratio is the amount owed divided by the amount extended by the creditor and the higher it is the better your FICO rating, in general. So if you have one credit card with a used balance of $500 and a limit of $1,000 as well as another with a used balance of $700 and $2,000 limit the average ratio is 40 percent ($1,200 total used divided by $3,000 total limits). If the first credit card company raises the limit to $2,000 the ratio lowers to 30 percent, which could boost the FICO rating.

There are other special factors which can weigh on the FICO score.

- Any money owed because of a court judgment, tax lien, etc. carry an additional negative penalty, especially when recent.

- Having one or more newly opened consumer finance credit accounts may also be a negative.[11]

FICO score range

A FICO score is between 300 and 850, exhibiting a negative skewed distribution with 60% of between approximately 650 and 799.[12] According to FICO the median score is 723.[13]

Each individual actually has three credit scores for the FICO scoring model because the three national credit bureaus, Experian, Equifax and TransUnion, each has its own database. Data about an individual consumer can vary from bureau to bureau.

NextGen score

The NextGen Score is a scoring model designed by the FICO company for assessing consumer credit risk. In 2004, at the time of launch, FICO research showed a 4.4% increase in the number of accounts above cutoff while simultaneously showing a decrease in the number of bad, charge-off and Bankrupt accounts when compared to FICO traditional[14].

Each of the major credit agencies market this score generated with their data differently:

- Experian: FICO Advanced Risk Score

- Equifax: Pinnacle

- TransUnion: Precision

Prior to the introduction of NextGen, their FICO-based scores were also marketed under different names:

- Experian: FICO or FICO II

- Equifax: BEACON

- TransUnion: EMPIRICA

VantageScore

In 2006, to try to win business from FICO, the three major credit-reporting agencies introduced VantageScore. According to court documents filed in the FICO v. VantageScore federal lawsuit the VantageScore market share is less than 6%. The VantageScore score methodology produces a score range from 501–990.[15]

CE Score

CE Score is published by CE Analytics and licensed to sites like Community Empower and Quizzle. This score is sold to lenders and investment banks but is free to consumers. It has a range of 350 to 850.[16][17]

Free annual credit report

As a result of the FACT Act (Fair and Accurate Credit Transactions Act), each legal U.S. resident is entitled to a free copy of his or her credit report from each credit reporting agency once every twelve months.[18] The law requires all three agencies to provide reports: Equifax, Experian, and Transunion.

Non-traditional uses of credit scores

Credit scores are often used in determining prices for auto and homeowner's insurance. Starting in the 1990s, the national credit reporting agencies that generate credit scores have also been generating more specialized insurance scores, which insurance companies then use to rate the insurance risk of potential customers.[19][20] Studies indicate that the majority of insureds pay less in insurance through the use of scores.[21][22] These studies point out that people with higher scores have fewer claims.

Criticism

Credit scores are widely used because they are inexpensive and largely reliable, but do have their failings.

Easily gamed

Because a significant portion of the FICO score is determined by the ratio of credit used to credit available on credit card accounts, one way to increase the score is to increase the credit limits on one's credit card accounts.[23]

Not a good predictor of risk

Some have blamed lenders for inappropriately approving loans for subprime applicants, despite signs that people with poor scores were at high risk for not repaying the loan. By not considering whether the person could afford the payments if they were to increase in the future, many of these loans may have put the borrowers at risk for default.[24]

According to a Fitch study, the accuracy of FICO in predicting delinquency has reduced in recent years. In 2001 there was an average 31-point difference in the FICO score between borrowers who had defaulted and those who paid on time. By 2006 the difference was only 10 points.

Some banks have reduced their reliance on FICO scoring. For example, Golden West Financial (which merged with Wachovia Bank in 2006) abandoned FICO scores for a more costly analysis of a potential borrower's assets and employment before giving a loan.[23]

See also

References

- ^ Report to the Congress on credit scoring and its effects on the availability and affordability of credit

- ^ An overview of consumer data and credit reporting

- ^ [1]

- ^ "How Are Credit Scores Calculated? Learn What Affects Your Credit Score". myFICO.com. http://www.myfico.com/CreditEducation/WhatsInYourScore.aspx. Retrieved 2010-01-19.

- ^ Dayana Yochim. "How Lenders Keep Score". TheMotleyFool. http://www.fool.com/ccc/check/check02.htm. Retrieved 2008-02-29.

- ^ 3. Pay on time - How to be a savvy credit cardholder(Aug. 27, 2008)Bankrate, Inc

- ^ Here's how you can shape up your credit score Sandra Block (1/29/2008)Your Money columns, USA TODAY

- ^ The Real Estate Wonk: How-to Monday: Credit scores - reporter Jamie Smith Hopkins - Baltimore Sun

- ^ Is Paying Off the Mortgage Good for Our Credit? CREDIT CARDS Q&A By Joan Goldwasser, Kiplinger Personal Finance magazine, October 2008

- ^ "Plot a course to buying a home", The Dallas Morning News, Dec. 3, 2007

- ^ "Hold Off on Opening New Credit Cards" 12-09-07

- ^ Credit Score Information: About FICO Scores - myFICO.com

- ^ "New Mortgages Worry Regulators" The Washington Post, June 10, 2006

- ^ "FICO NextGen Score". FICO. http://www.fico.com/account/resourcelookup.aspx?theID=37.

- ^ "VantageScore". VantageScore.com. http://www.vantagescore.com/about/vantagescore_methodology. Retrieved 2010-01-19.

- ^ "How to get a free credit score". Bankrate.com. http://www.bankrate.com/finance/credit-cards/how-to-get-a-free-credit-score-6.aspx. Retrieved 2011-06-26.

- ^ "What kind of credit score does Quizzle offer?". Quizzle. https://www.quizzle.com/frequently-asked-questions#credit_score_type. Retrieved 2011-06-26.

- ^ https://www.annualcreditreport.com/cra/helpfaq#creditfile

- ^ Credit-based insurance scores: Impacts on consumers of automobile insurance A Report to Congress by the Federal Trade Commission July 2007

- ^ No evidence of disparate impact in Texas due to use of credit information by personal lines insurers Dr. Robert P. Hartwig in January, 2005. Insurance Information Institute

- ^ Allstate Insurance Company’s additional written testimony July 23, 2002

- ^ Use and impact of credit in personal lines insurance premiums pursuant to Ark. code Ann. §23-67-415 (September 1, 2006) - A report to the legislative council and the Senate and House committees on insurance and commerce of the Arkansas General Assembly (as required by Act 1452 of 2003)

- ^ a b "Credit Scores: Not-So-Magic Numbers" Business Week, Feb. 7, 2008.

- ^ Credit scores didn't fail in screening applicants for subprime loans(April 7, 2008)By PAMELA YIP / The Dallas Morning News

External links

- "Credit Scores: What You Should Know About Your Own," by Malgorzata Wozniacka and Snigdha Sen (November 2004) - PBS FRONTLINE

Categories:

Wikimedia Foundation. 2010.